Capital Investments in Beauty and Cosmetics: Market Overview

The global cosmetic and beauty market is anticipated to grow to $416 billion in 2028 with a CAGR of 7%. Although the COVID-19 pandemic had a significant negative impact during 2019 and 2020 on the market, the rise in CAGR is attributable to a strong rebound in consumer demand. The market exhibited lower growth of -11% and contracted in 2020, but grew to $254 billion in 2021. This shows that the market has constant demand and is returning to the pre-pandemic level as the effects of the pandemic decrease.

In this report, J&A will analyze the international capital market activity conducted within the beauty and cosmetics market between 2020 and 2022.

Market Overview

The beauty and cosmetics industry are segmented into three major categories: skin care, hair care, and makeup.

- Skin care forms the largest segment of the cosmetics market with 34%. According to research, the average spend on skin care per person per year is over $1,200 USD in the USA.

- Hair care maintained a market position of 23%, mostly due to younger consumers. The hair care segment is expected to grow with a CAGR of 6%.

- The other segments of beauty and cosmetics include hygiene, oral care, and fragrance products with a combined 34% market share.

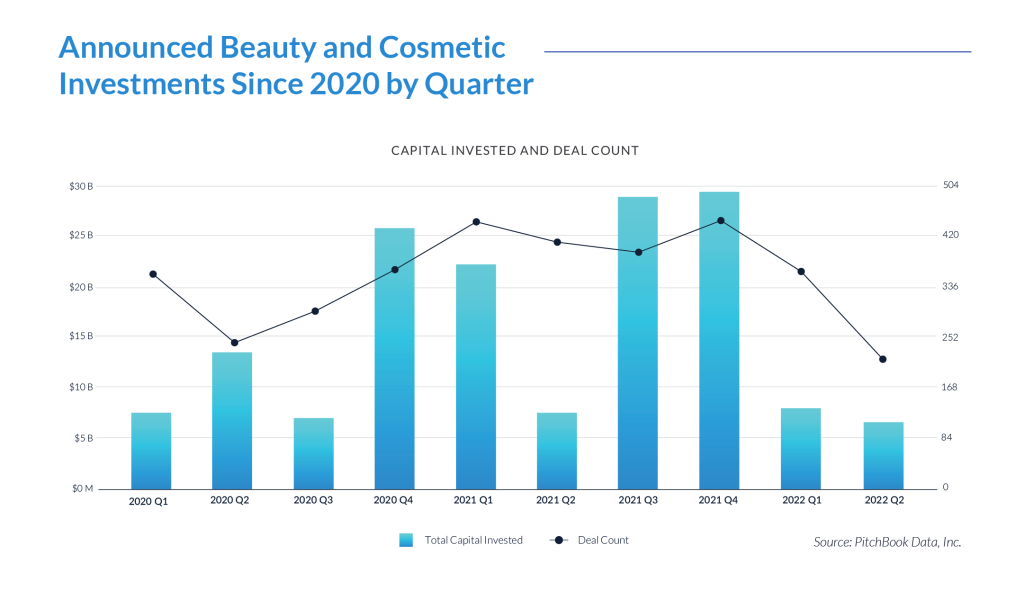

- In 2020, a focus on beauty and cosmetics (due to the global COVID-19 pandemic) led to a spike in deal flow in the sector, especially in the Q4 time period with $26 billion in capital investments and 390 deals. The total average deal size in 2020 was $174 million.

- In 2021 Q4 the largest deal was $29 billion, and a total of 430 deals were recorded.

- In 2021 the average deal size was recorded at $201 million, which shows that the average deal size has increased significantly compared to 2020 when it was recorded at $173 million.

- Between 2020 and 2022 Q2, 3,348 total deals deployed capital into the beauty and cosmetics market with $154 billion of capital deployed. The average deal size in the sector was $16 billion within that time frame.

- The periods with the largest amount of capital invested were 2021 Q4 and 2022 Q1, due to the significant market growth with the global COVID-19 pandemic.

- Jahani and Associates (J&A) anticipate that trend will continue to grow with notable increases in 2022 and forward.

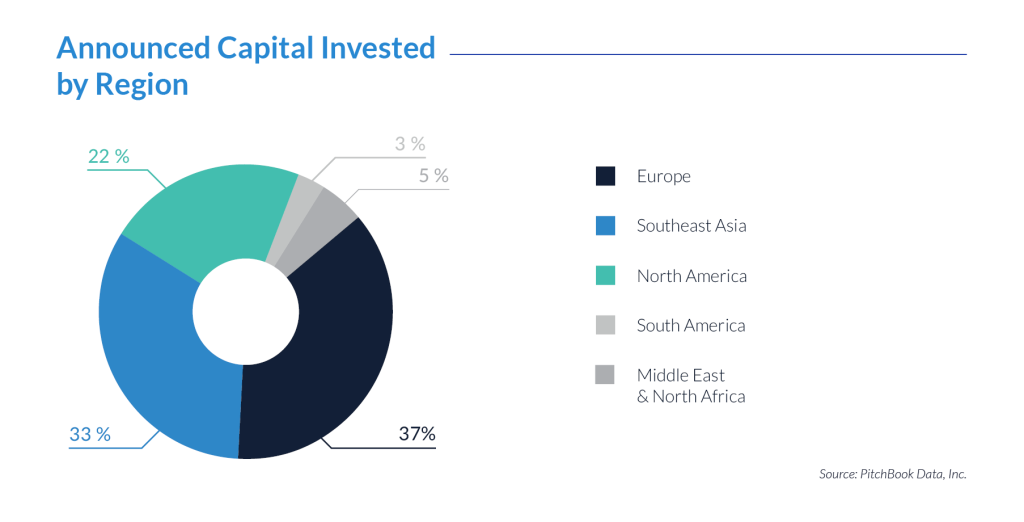

- Europe is leading the capital invested with 37% of the total raise. The beauty and cosmetics market is growing in the European market mostly. The scalability of the e-commerce market combined with the global pandemic effect on social media directly affected beauty and cosmetics products.

- Asia has the second-largest capital investment with 33%. Additionally, China and Japan have the largest market size with $52 billion and $38 billion respectively. The technological research and developments in the specific market have grown respectively in the Asian region.

- Due to their high-end quality of the products, the Korean market has an important place in the global market. In 2019, the market size was estimated at $10 billion. Korea is one of the top 10 beauty markets in the world and has 3% of the global market.

- The USA holds 22% of the capital investments. The USA currently is the world’s largest beauty market, with about 20% share, followed by China at 13% and Japan at 8%.

- South America has 3% of the capital investments and the market holds significant growth.

There is considerable growth in the beauty and cosmetics sector and also in the capital market between 2020 Q4 and 2021 Q4. The development of new technologies in the beauty and cosmetics industry has disrupted the existing ecosystem, and technological innovations are projected to significantly impact market growth in the USA and Korean regions in the beauty and cosmetic sectors. The 14% growth in the global e-commerce market makes beauty and cosmetics products more attractive, and the market more scalable for investments. J&A predicts a continued increase in capital market activity within the beauty and cosmetics sector in Southeast Asia and North America as economies become more interconnected and companies expand into new international markets.

Sources: Pitchbook Data, Inc.