https://www.thetimes.co.uk/article/joe-biden-takes-blue-collar-blueprint-to-the-public-dz05vlbsw

The chart below identifies the type of products associated with each import and export category based on World Bank nomenclature.

MENA’s trade position is unique when compared to China and the USA. MENA’s dominance is driven by the presence of oil, a natural resource. The USA and China’s imports and exports are not driven by a natural resource and are therefore more easy to replicate. If the MENA countries successfully diversify their economies, the region can become an increasingly powerful player by building on this natural resource foundation and then competing with other regions on services, technology, and other high-growth sectors. Due to current reforms in major MENA countries, the region is actively accomplishing this.

The MENA region is a gateway between the growing economies of Africa and Southeast Asia and more stabilized regions such as North America and Europe. This gives the region a strong value-added position when participating in trade between these other parts of the world.

The UAE and KSA are the most dominant players in the MENA economy. They account for the majority of imports and exports as well as most of the region’s economic activity. The UAE has been removing barriers to trade that are not tariff-related, such as allowing expedited customs and the use of technology to create more efficient government organizations. KSA has recently started opening trade policies that reflect UAE standards.

KSA’s Vision 2030 is a framework to reduce Saudi Arabia’s dependence on oil and diversify its economy. This will be accomplished through investments in health, education, infrastructure, recreation, and tourism. The Vision 2030’s goals include reinforcing economic and investment activities, increasing non-oil international trade, increasing government spending on the military, and promoting a more secular image of the kingdom.

As shown in the previous J&A series, tech investments are on the rise in the MENA region. The UAE has recently made 10 major food-tech investments as part of its continued commitment to food independence and leadership. These food-tech investments include smart farms, food delivery, curated menus, and more. The image above shows three examples of these investments from different categories.

In the final part of our series, we will investigate the Gulf Cooperation Council’s role in global trade for the MENA region as well as steps the council is taking to increase its cooperation and cumulative strength.

The following chart shows the trade openness of the GCC. This index is calculated by adding imports and exports in goods and services and dividing by the total GDP. The larger the ratio, the more the country is open to international trade.

The region represents approximately half the volume of imports and exports compared to the USA and China, but produces nearly 40% of the world’s fuel supply. The general volatility of fuel has pushed leaders to diversify the economy.

Sources: IAGS | The World Bank | IMF GCC Banking | IMF GCC Markets | IMF Trade and Foreign Investment | Saudi Arabia Vision 2030 | UAE Ministry of Finance

[vc_row dfd_row_config=”full_width_content”][vc_column][vc_column_text el_class=”blog-glance”]

[/vc_column_text][/vc_column][/vc_row][vc_row dfd_row_config=”full_width_content” el_class=”blog-img-section”][vc_column][vc_single_image image=”9178″ img_size=”full”][/vc_column][/vc_row][vc_row dfd_row_config=”full_width_content”][vc_column][vc_column_text]The Gulf states and Israel provide an opportunity for the US to participate in a global economy that will be more centered on the Middle East than it was before the virus. This future must be a cornerstone of US policy, as well the legacy issues around security.

Covid has threatened the mature economies of the US and Europe, accelerated China’s inevitable rise, and given opportunity to the region’s often more agile and adaptable countries.

There are few countries in the world who have (almost) put the pandemic behind them and are on good terms with both the US and China. Those are the countries who are set to lead the world in the 21st century. They are almost exclusively in the Middle East.

The rise of the Middle East as a gateway between the US and China presents an opportunity for Biden to re-engage with Beijing through the neutral soil of Israel and the Gulf states. Biden should not be afraid of celebrating and building on the diplomatic progress achieved under the Trump administration through the end of the GCC rift and the Abraham accords.

Being the “new Europe” is something that Middle Eastern leaders are understandably motivated by, particularly in light of their relations with both DC and Beijing. Europe was the middle ground for the Soviet-US Cold War, and the Middle East is the same for the China-US relationship — geographically, politically and economically.

Rather than continue to fight yesterday’s conflicts and ignore today’s achievements (perhaps focused on distancing himself from Trump’s policies), Biden should craft policy based on the reality that the Middle East is transitioning from a 20th century defined by conflict and insecurity to a 21st century where the Silk Road is once again the social, economic, cultural, and political center of the world.

This is a future into which the Middle East is rapidly progressing. Three of the top five countries with the most Covid vaccinations (excluding the Seychelles and Maldives) are in the Middle East — namely the UAE, Israel, and Bahrain. In addition to a successful vaccination campaign, total death rates in these countries and others in the region have remained low. All this while key industries, including tourism, have often remained open.

Saudi Arabia has been working to almost triple its non-oil revenues, and is investing billions into futuristic cities like NEOM and “The Line.” The UAE successfully completed a mission to Mars during the pandemic and recently announced plans to double Dubai’s population, all while commentators in London and New York discuss the “death of cities.”

Gulf economies also benefit from a low debt to GDP ratio, which will allow them to maintain growth while more developed and leveraged economies struggle in the wake of the pandemic. The US currently has a debt to GDP ratio of over 100 percent; in Saudi Arabia and the UAE, the debt to GDP ratio is only 20 percent, meaning those governments will have spending power well into the future for public and private projects.

China is busy building deeper links in the region, where doing business is more important than talking politics. It is important to Biden’s legacy that US policymakers and investors do the same, and foster both cultural and economic connections to the new Middle East rather than allowing themselves to be crowded out.

To this day, too many American political and business leaders are driven by the impulses that impacted actions between them and the Middle East at the start of the millennium. Twenty years on, the White House should look to the future. It must adapt to the rise of China by utilizing the Middle East’s neutral ground to increase cooperation with Beijing.

It’s high time an American president looked to the Middle East for its entrepreneurship, adaptability and its e-governance, rather than simply for its oil.

Joshua Jahani is a Cornell alum, public speaker and investment banker with a focus on the Middle East and Africa

https://www.independent.co.uk/voices/biden-china-meeting-middle-east-b1819729.html[/vc_column_text][/vc_column][/vc_row][vc_row el_class=”more-from-report”][vc_column][vc_column_text]

[/vc_column_text][vc_row_inner][vc_column_inner width=”1/2″][vc_column_text]https://www.bbc.com/news/world-middle-east-35221569[/vc_column_text][vc_column_text]https://www.politico.com/news/2021/03/29/us-biden-iran-nuclear-deal-478354[/vc_column_text][vc_column_text]https://www.reuters.com/article/us-iran-nuclear-usa/bidens-iran-approach-praised-as-deft-despite-lack-of-progress-idUSKCN2AW2SB[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/2″][vc_column_text]https://www.bbc.com/news/world-middle-east-42008809[/vc_column_text][vc_column_text]https://www.washingtonpost.com/world/2021/03/19/biden-iran-deal-stalemate/[/vc_column_text][vc_column_text]https://www.nbcnews.com/politics/national-security/biden-administration-says-it-s-ready-nuclear-talks-iran-n1258299 [/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row el_class=”more-from-report” disable_element=”yes”][vc_column][vc_column_text]

[/vc_column_text][vc_row_inner][vc_column_inner width=”1/2″][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/2″][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row dfd_overlay_color=”#e9ecf2″ el_class=”access-article”][vc_column width=”1/2″][vc_column_text]

[/vc_column_text][/vc_column][vc_column width=”1/2″][dfd_button button_text=”Explore the full article” buttom_link_src=”url:%23|||” style=”style_1″ box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” hover_box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” el_class=”blue-btn”][dfd_button button_text=”Download the PDF” buttom_link_src=”url:%23|||” style=”style_1″ box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” hover_box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” el_class=”blue-btn”][/vc_column][/vc_row]

Taiwan’s rail company says 36 people are known to have died, and dozens injured. Myanmar’s deposed leader Aung San Suu Kyi had already been accused of breaking COVID-19 rules and illegally possessing walkie-talkies—now she’s been charged with violating the country’s official secrets act. And the story of the Italian businessman who tried to fake his own kidnapping for financial gain, but ended up as a prisoner of a jihadist group for three years.

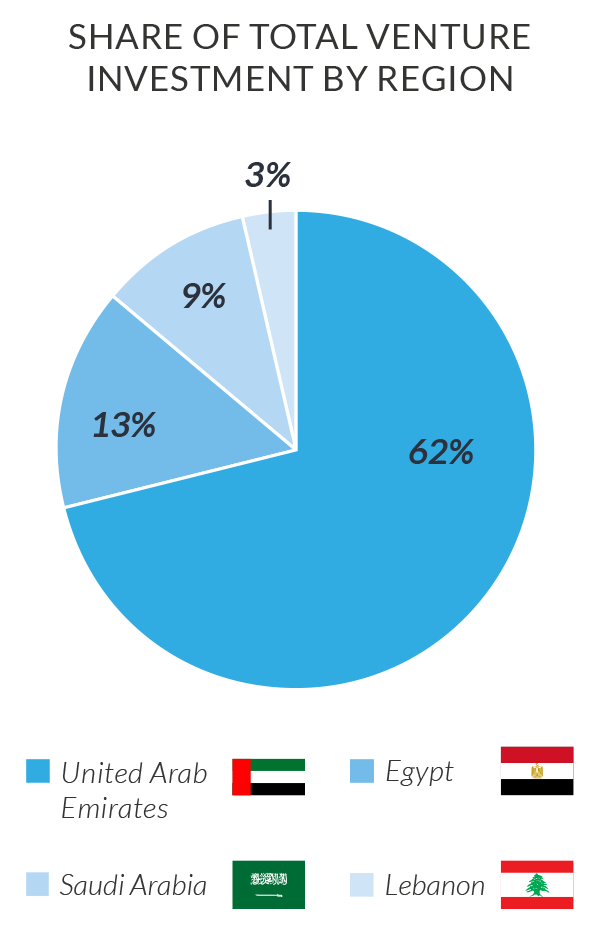

The United Arab Emirates (UAE): The majority of venture capital Middle East and Northern African (MENA) investments in 2019 were made by United Arab Emirates (UAE) investors, accounting for 62% of total MENA investment.

We expect this trend to continue due to the more robust investment infrastructure in the UAE. Although the percentage of deals completed did not change from 2018 to 2019, the UAE’s percentage of total MENA investment increased 21%. This signifies the continuing growth in UAE investment size.

Egypt: A distant second in terms of total MENA investment (13%), Egypt completed seven more deals in 2019 compared to the UAE, confirming the assumption that due to its size the country is investing less money in more deals.

Saudi Arabia: Rounding out the top three in terms of deal value closed is Saudi Arabia. Saudi Arabia’s position is expected to increase in the upcoming years due to the government’s efforts to diversify the economy.

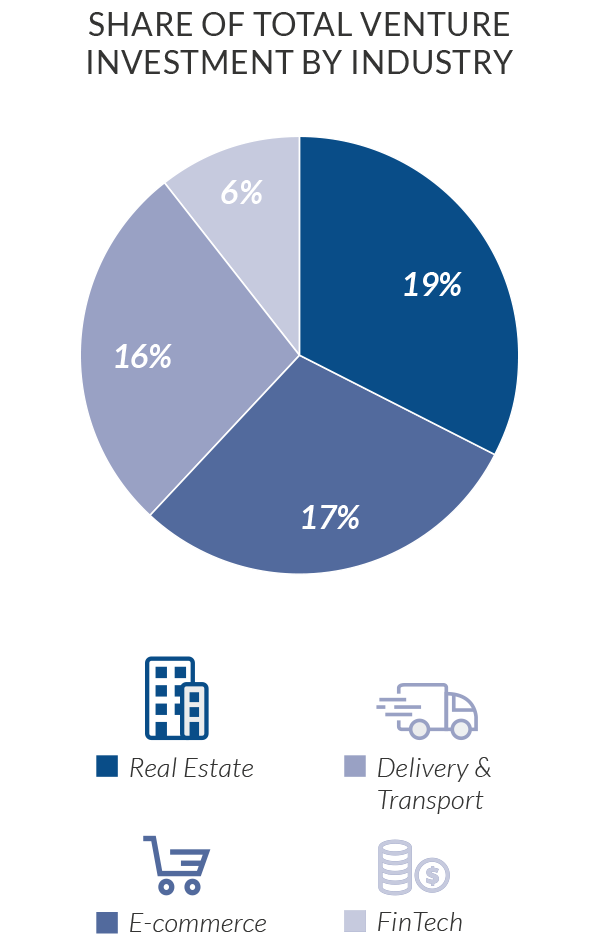

Real estate held the top spot in terms of investment dollars in 2019 but did not rank in the top five for deal count. This is a result of the capital-intensive nature of the investments. Fintech remained the leader in number of deals despite the moderate industry slowdown near the end of 2019. These investments include those in blockchain and crypto-related businesses.

Although funding for fintech was number five in terms of investment dollars, these numbers signify an interest that investors like to enter the market early.

E-commerce took second place in terms of funding value (17%) and deals (10%). As the industry continues to grow globally and key players continue to make acquisitions, this is an interesting market to watch. These numbers are bolstered by a $6.2 million seed round investment in the e-commerce wholesale food and grocery marketplace MaxAB.

Delivery and transport realized large growth in investment dollars with 10% growth from 2018. This mimics trends from USA investments as delivery startups continue to compete for the expanding market.

Previously, we detailed the recent venture funding the region by industry and country. Now that the Middle East investment landscape has been outlined, we will walk through how to use a joint venture (JV) strategy for bringing innovation to the MENA region.

PwC recently conducted a survey of business executives in the Middle East asking them which activities, if any, they were planning in the next 12 months to drive revenue growth.

Entering a new market or forming a joint venture was identified as a top priority for 83% of business executives in the Middle East.

Additionally, 17% of business executives identified collaborating with a startup or innovative company as a top priority.

These three objectives (entering a new market, forming a JV, or collaborating with startups) presents powerful opportunities for companies seeking capital and financial partners in the region.

Note: J&A utilizes a broad definition of joint ventures that includes distribution agreements, franchising agreements, reseller agreements, and traditional joint venture agreements in which multiple entities own equity positions in a new entity.

Joint ventures can be an ideal investment structure in certain situations, especially in fast-growing markets like MENA. Below are some common advantages associated with JVs.

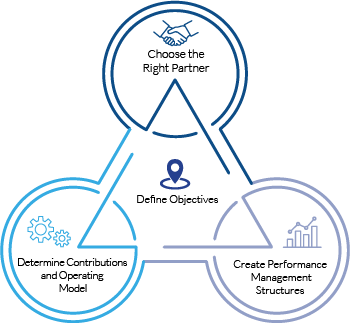

We have seen great success with North American and MENA JVs in recent years when a clear strategy, detailed planning, and strong execution is at the center of the deal. Below are components of success for long-term value creation.

Define objectives: Starting with the end in mind, defining the objectives and aligning to them will ensure the feasibility and strategic fit of the JV.

Choose the right partner: Due to the collaborative nature of JVs, selecting the right partner is critical to its success. Defined objectives inform selection criteria based on the needs of the partners (i.e. ownership of a critical asset such as presence in a market or intellectual capital). Other selection criteria to support the JV may include company culture, decision making, communication, trust, and financial drivers.

Determine contributions and operating model: Clearly articulating the link between asset contributions and ownership will drive success. Selecting a valuation methodology and layering in industry and region nuances will help guide the contribution discussion. Understanding the level of support, involvement, and key target dates for each company will act as a guide to ensure objectives are met.

For more information on MENA investments, please contact us at [email protected] or visit our website jahaniandassociates.com.

Originally published February 18, 2020. Updated March 20, 2020.

Sources: PWC Middle East CEO survey | McKinsey and Company | Magnitt | The World Economic Forum[/vc_column_text][/vc_column][/vc_row]

J&A has collected investor data to generate a summary of Middle Eastern and Northern African (MENA) investor location, investment size, investment volume, and investment location. This article provides data and insights on these topics. It is important to know that many transactions in the MENA region are not announced, therefore the metrics here report less activity than what is truly taking place. The date herein is collected from 2000 to 2018.

The insights and data herein signify strong growth in a maturing investment region. Next, we will review the amount of invested capital per deal, the number of deals invested in by MENA entities, and investment locations.

In this section, we will analyze the average money raised from MENA investors by round, the number of companies invested in by round, and briefly review where MENA portfolio companies are headquartered. All data is from the years 2000 to 2018.

The following section will highlight where investments are located, as MENA investments are more diverse than North American investments. J&A will also highlight regions where growth and opportunity are expected.

As shown in the previous section, investments are globally diverse for MENA investors. The data herein showcases which investments have taken place over the last 15 years. J&A expects strong South American and MENA investment growth due to government initiatives. We also expect Eastern African and Southern African investments to grow disproportionately in deal count five to 10 years from now.

The chart below shows the average investment dollar amount made by MENA investors in each region.

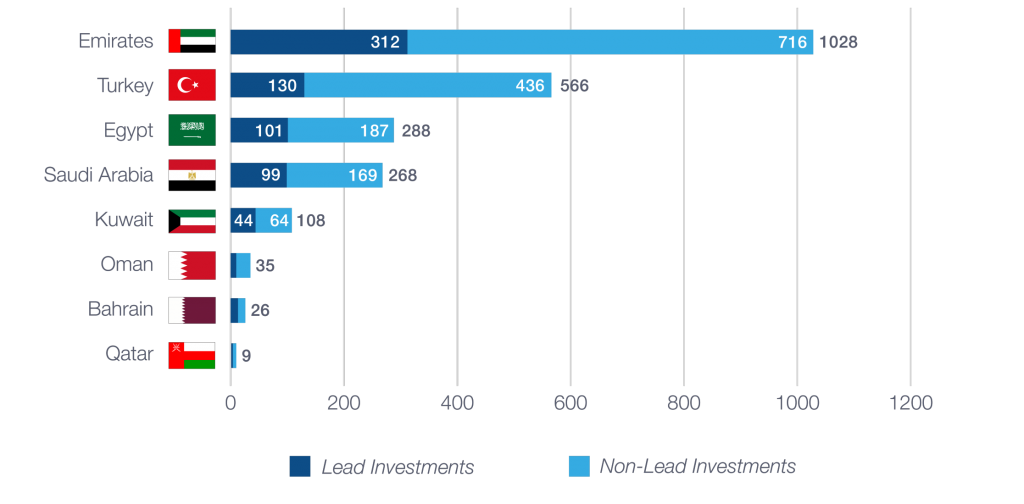

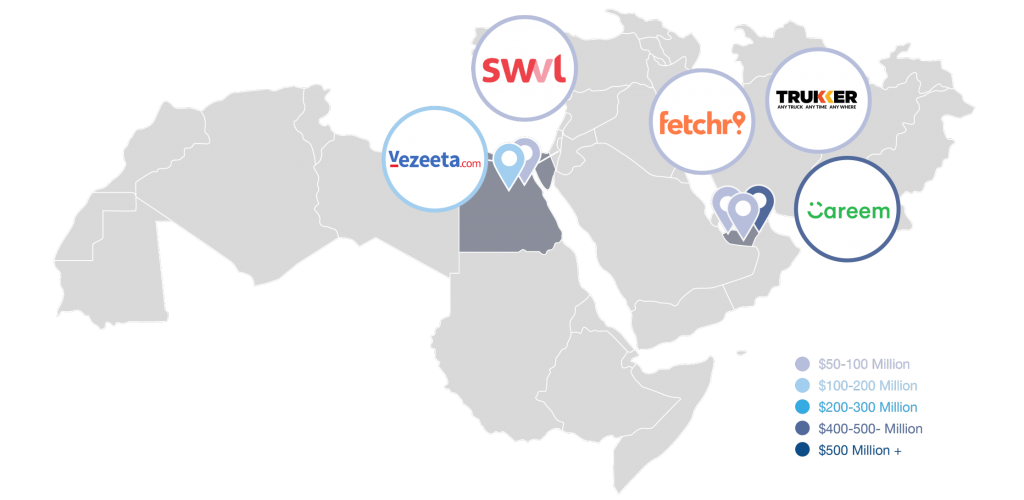

The map below shows the brands that raised over $50 million and their respective locations.

It is important to note the anticipated growth of Saudi Arabia in the MENA region. Based on the kingdom’s initiatives and relative wealth, J&A and other authorities expect the Kingdom of Saudi Arabia (KSA) to experience tremendous growth over the next 10 years. Investments in technology and innovation will be a major part of this growth. KSA is relatively small within MENA, but the country’s power in fuel and geopolitical posturing will likely lead to meaningful activity in the near term.

Sources: Crunchbase | McKinsey | International Monetary Fund | World Bank | PwC MENA

641 Lexington Ave. 15th Floor

New York, NY, USA 10018