Technology Procurement and IT Solutions Consulting Sector M&A Transactions and Valuations

From Q1 2021 through Q4 2025, sustained enterprise digital transformation, increasing IT infrastructure complexity, and heightened demand for vendor-neutral advisory services drove robust M&A activity within the technology procurement and IT solutions consulting sector. As organizations navigated multi-cloud adoption, cybersecurity integration, telecom modernization, and SaaS proliferation, technology sourcing and vendor management functions evolved from transactional processes into strategic enterprise capabilities.

Enterprises, particularly within the mid-market, faced growing challenges in managing fragmented vendor ecosystems, negotiating service contracts, and optimizing long-term IT spend. As a result, advisory-led procurement platforms and IT solutions consultants embedded within enterprise purchasing workflows emerged as mission-critical intermediaries. These range from large-scale brokerage and advisor network platforms to smaller, consulting-led procurement firms that provide hands-on sourcing, implementation, and vendor management support. Strategic acquirers and financial sponsors have increasingly targeted scalable, asset-light brokerage and advisory models characterized by recurring commission and services-based revenue, strong advisor networks, and diversified vendor relationships.

This report analyzes M&A activity and valuation dynamics across the sector, including transaction trends, deal structure, capital deployment patterns, valuation benchmarks, and representative case studies that underscore continued consolidation and platform formation across the technology advisory ecosystem.

EXHIBIT 1

Structural Demand Drivers in Technology Procurement and IT Solutions Consulting

DIGITALIZATION AS A CORE ENTERPRISE PRIORITY

IT investment continues to be driven by enterprise digital transformation, operational efficiency initiatives, and competitive positioning. Mid-sized enterprises increasingly view technology infrastructure as essential to long- term scalability, operational resilience, and competitive differentiation.

RISING IT COMPLEXITY DRIVING OUTSOURCING

As cloud, IoT, big data, and AI adoption accelerates, internal IT teams face increasing capacity and expertise constraints. Organizations increasingly rely on external procurement advisors and IT solutions consultants to manage vendor ecosystems, coordinate infrastructure integration, and navigate architectural complexity.

HYBRID BUSINESS MODELS COMBINING PRODUCT PROCUREMENT AND SERVICES

Leading platforms combine technology procurement with advisory, implementation, and managed services, positioning themselves as integrated, end-to-end technology partners rather than transactional intermediaries.

SHIFT TOWARD RECURRING REVENUE MODELS

Firms incorporating managed services, lifecycle IT support, and ongoing optimization engagements enhance revenue visibility while deepening long-term client relationships.

CLOUD AND MANAGED SERVICES EXPANSION

The rapid migration toward cloud infrastructure and managed services is increasing demand for consultants capable of structuring sourcing strategies, negotiating vendor agreements, and optimizing long-term IT spending.

EXHIBIT 2

Market Structure, Consolidation and Competitive Positioning

- Highly Fragmented Competitive Landscape:

The IT procurement and technology solutions consulting market remains highly fragmented, with numerous regional advisory firms and specialized providers operating alongside a limited number of scaled platforms with meaningful market share. In addition to these platforms, the sector includes a broad base of smaller, advisory-led IT procurement and consulting firms that combine vendor sourcing, implementation support, and project-based services, particularly within mid-market and public sector environments. - Scale Advantages in Vendor Negotiation and Service Breadth:

Larger consulting platforms benefit from greater purchasing leverage, broader solution portfolios, deeper technical expertise, and expanded geographic reach, creating structural competitive advantages in vendor negotiations and enterprise client engagement. - Active Consolidation and Platform Formation:

Market leaders are pursuing acquisition-led expansion strategies to broaden service capabilities, deepen vertical specialization, and strengthen their positioning as full-service technology advisory partners. - Mid-Market-Centric Demand Base:

Mid-sized enterprises often lack the internal IT resources required to manage complex, multi-vendor technology environments, reinforcing sustained demand for outsourced procurement advisory and IT solutions consulting services. - Technology-Enabled Differentiation:

Platforms integrating analytics capabilities, automation tools, and vendor performance dashboards into advisory offerings improve scalability and operating leverage while enhancing client retention and long-term engagement.

Source: Gartner IT services market research; IDC cloud and managed services outlook; Bitkom industry fragmentation data; HSBC European IT services sector analysis; McKinsey technology services M&A commentary; professional services consolidation research.

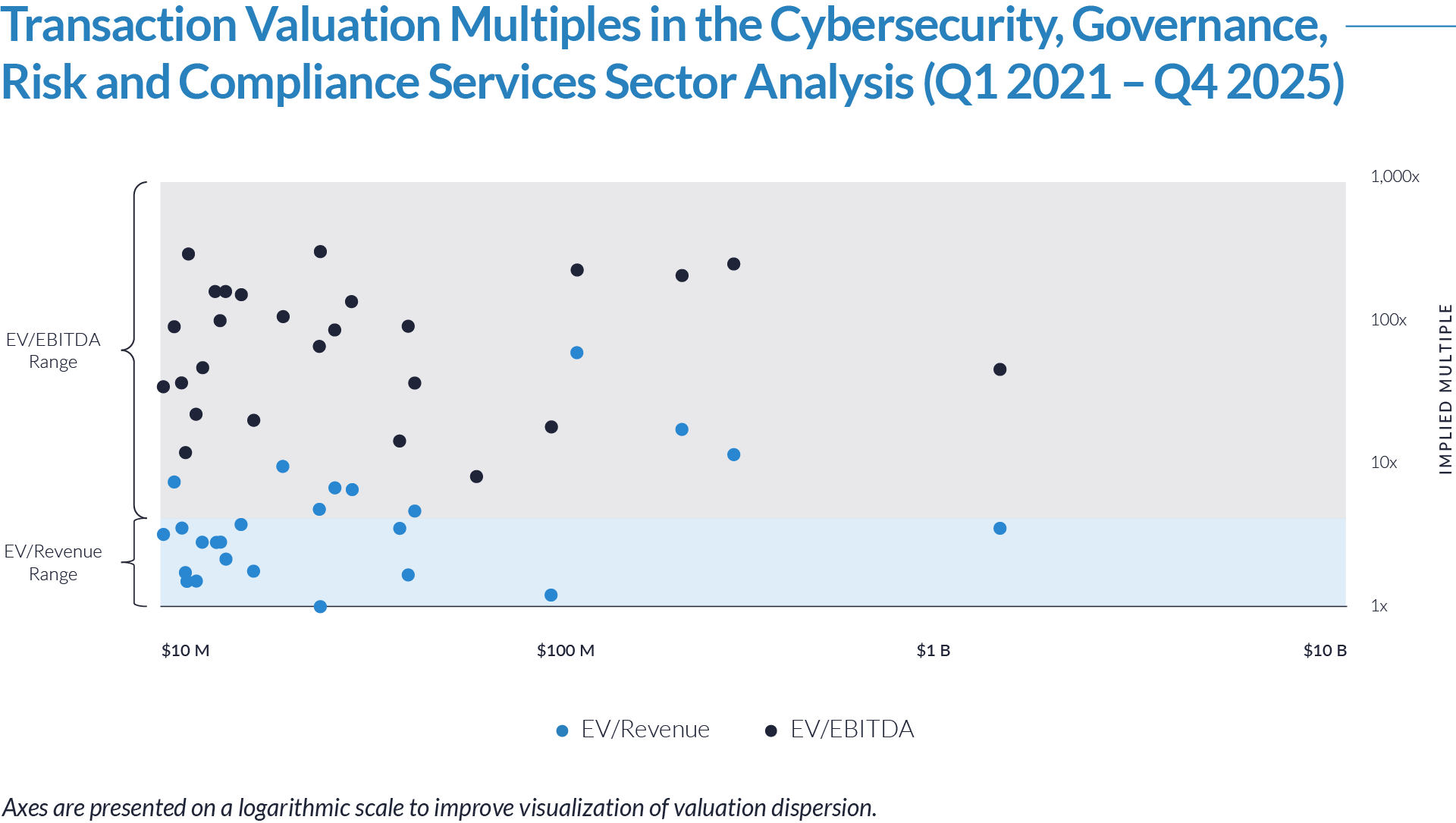

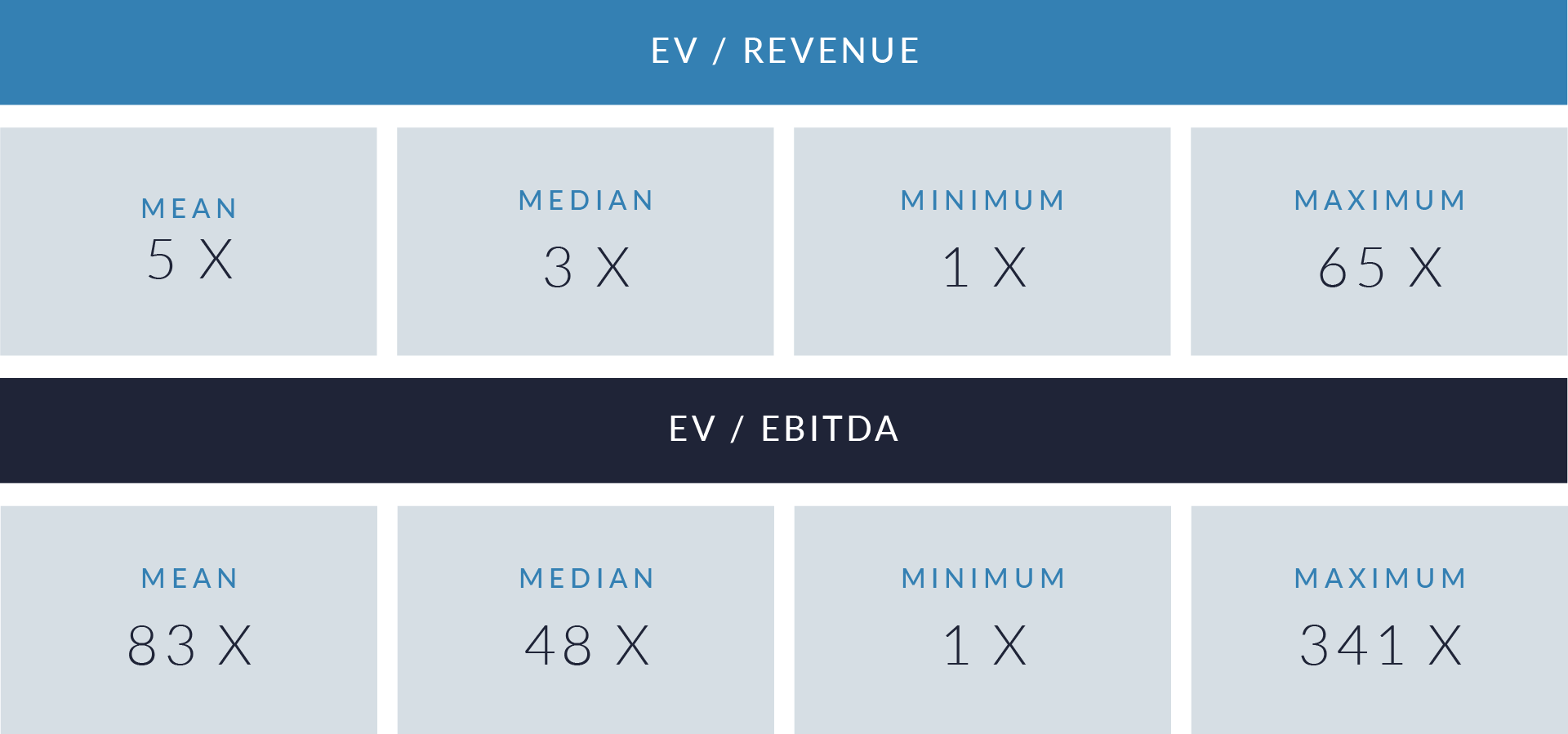

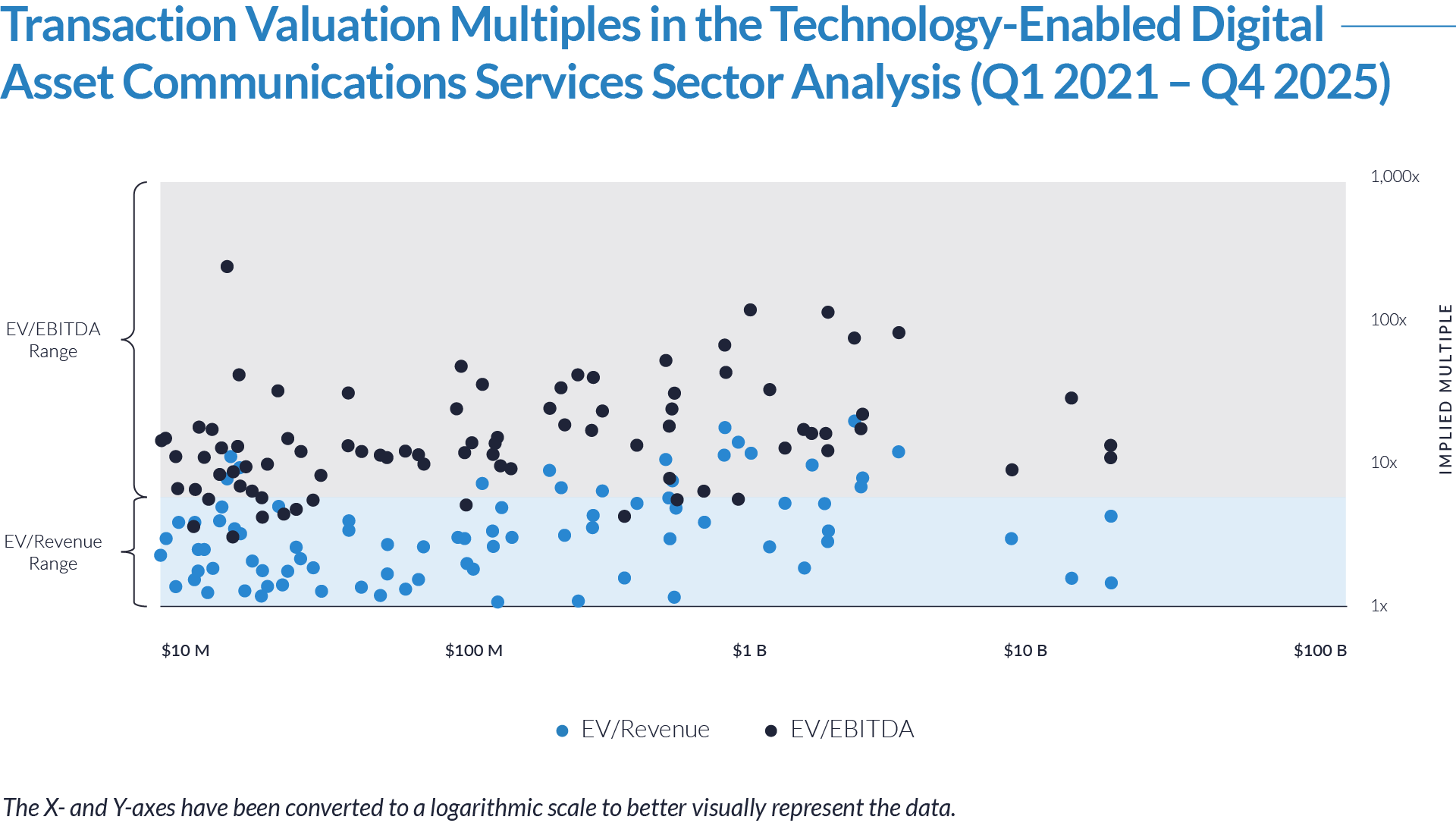

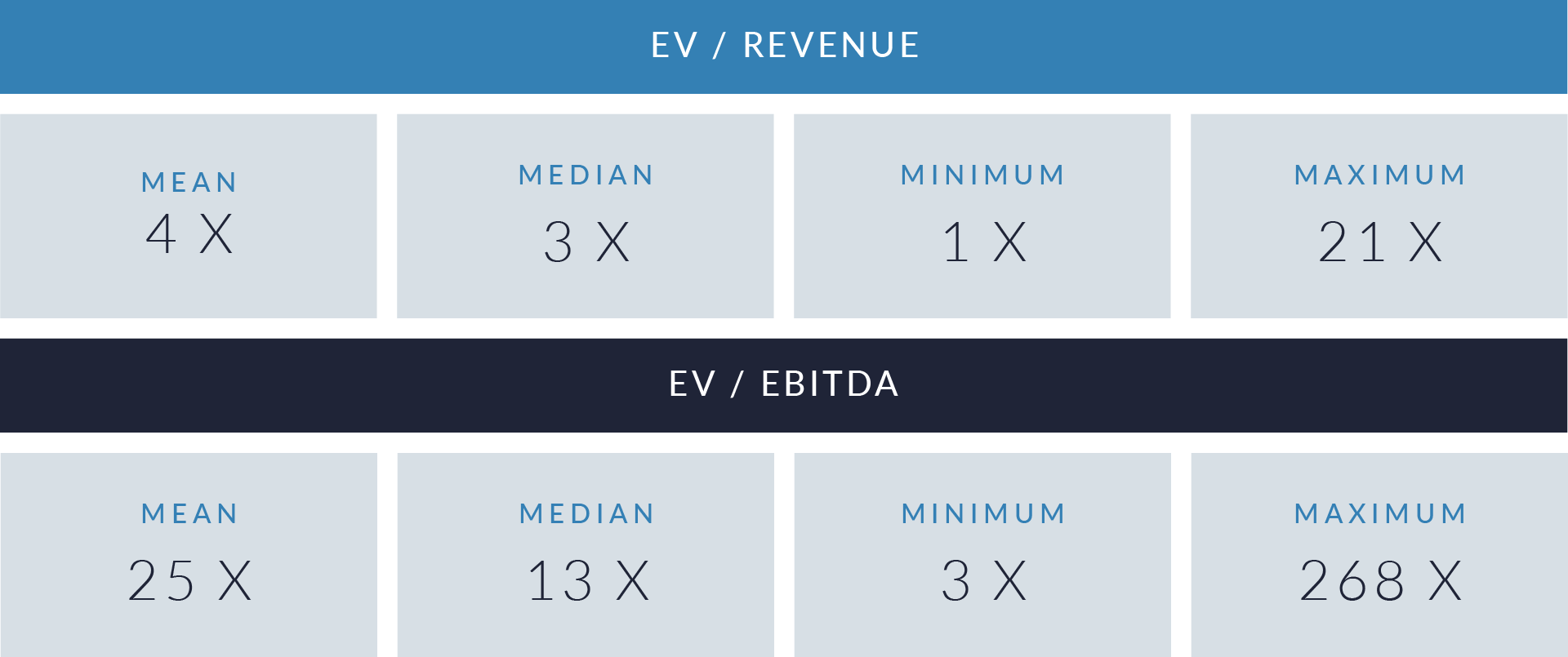

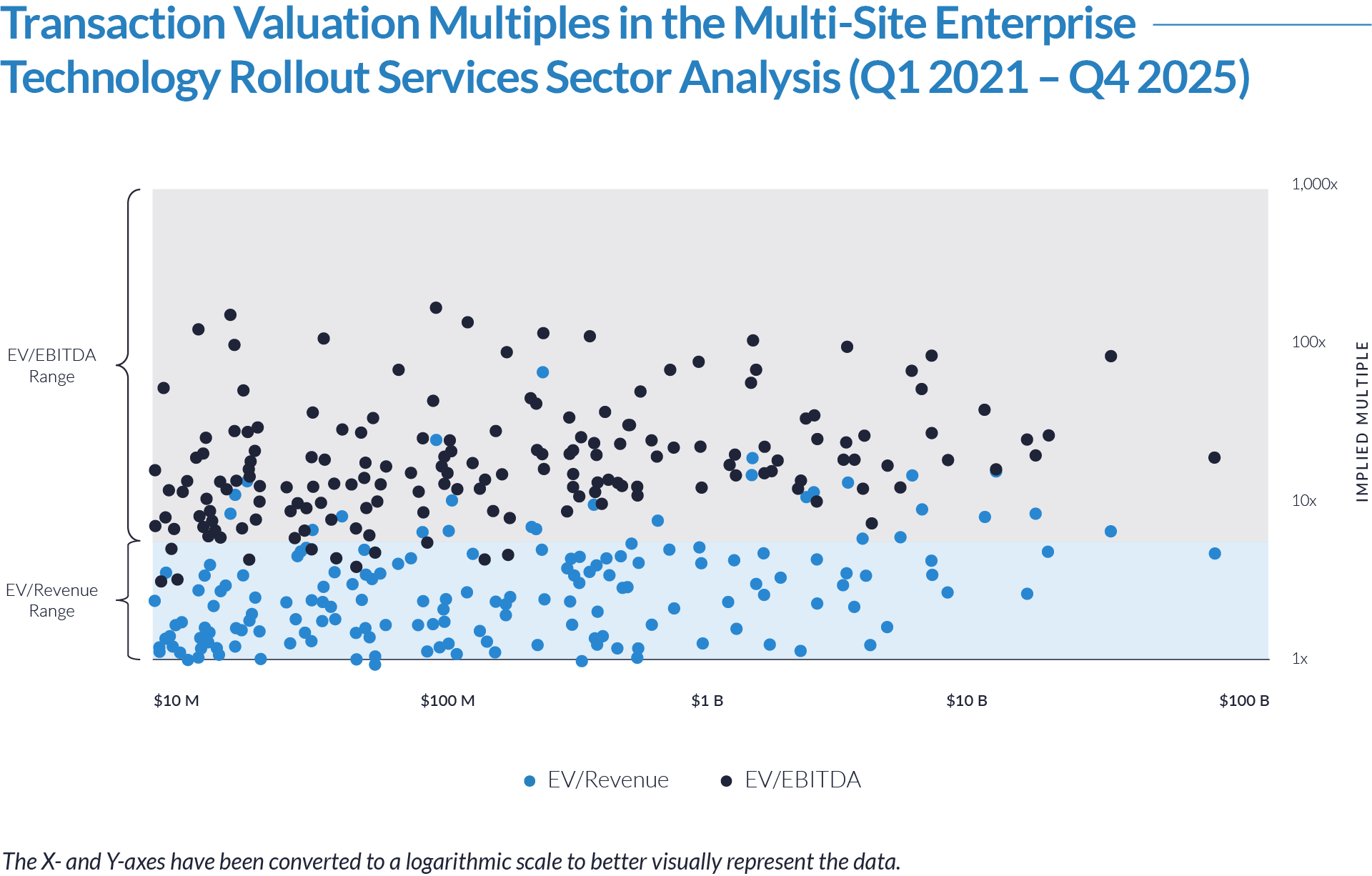

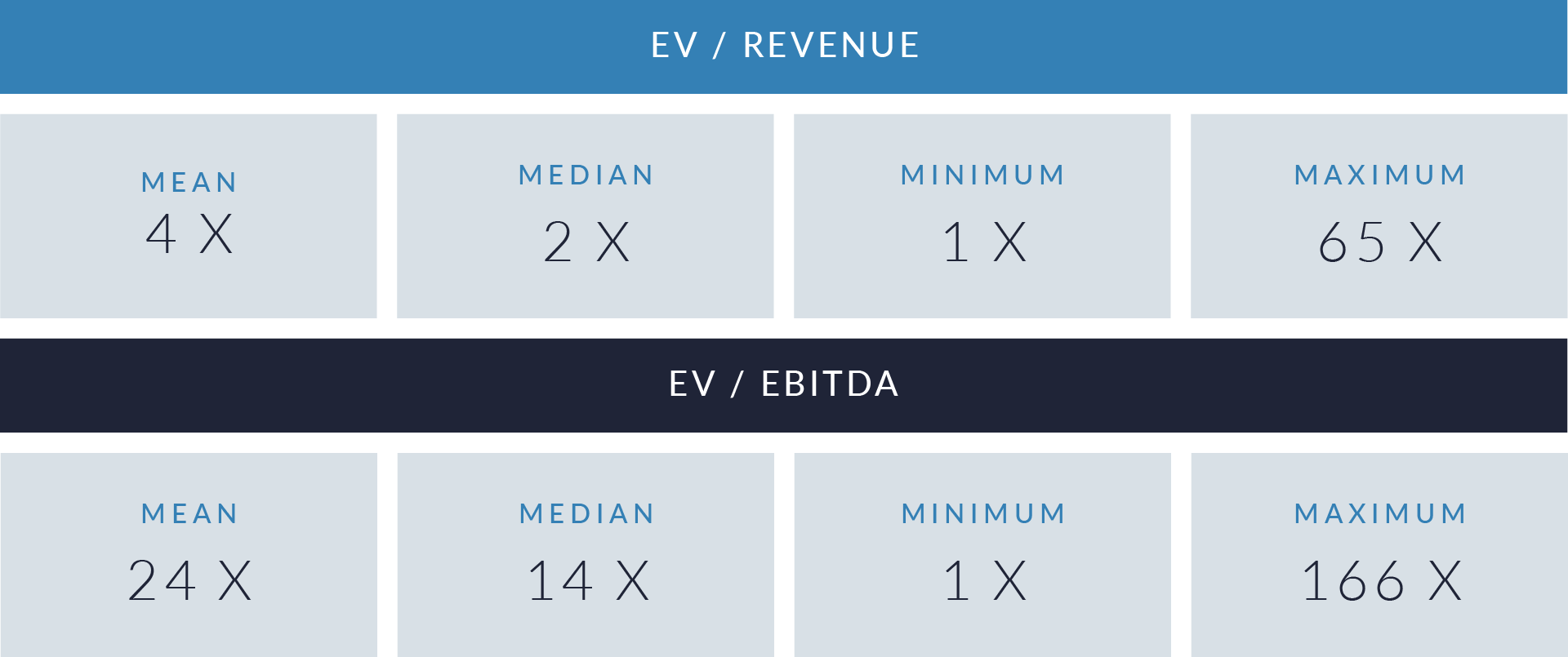

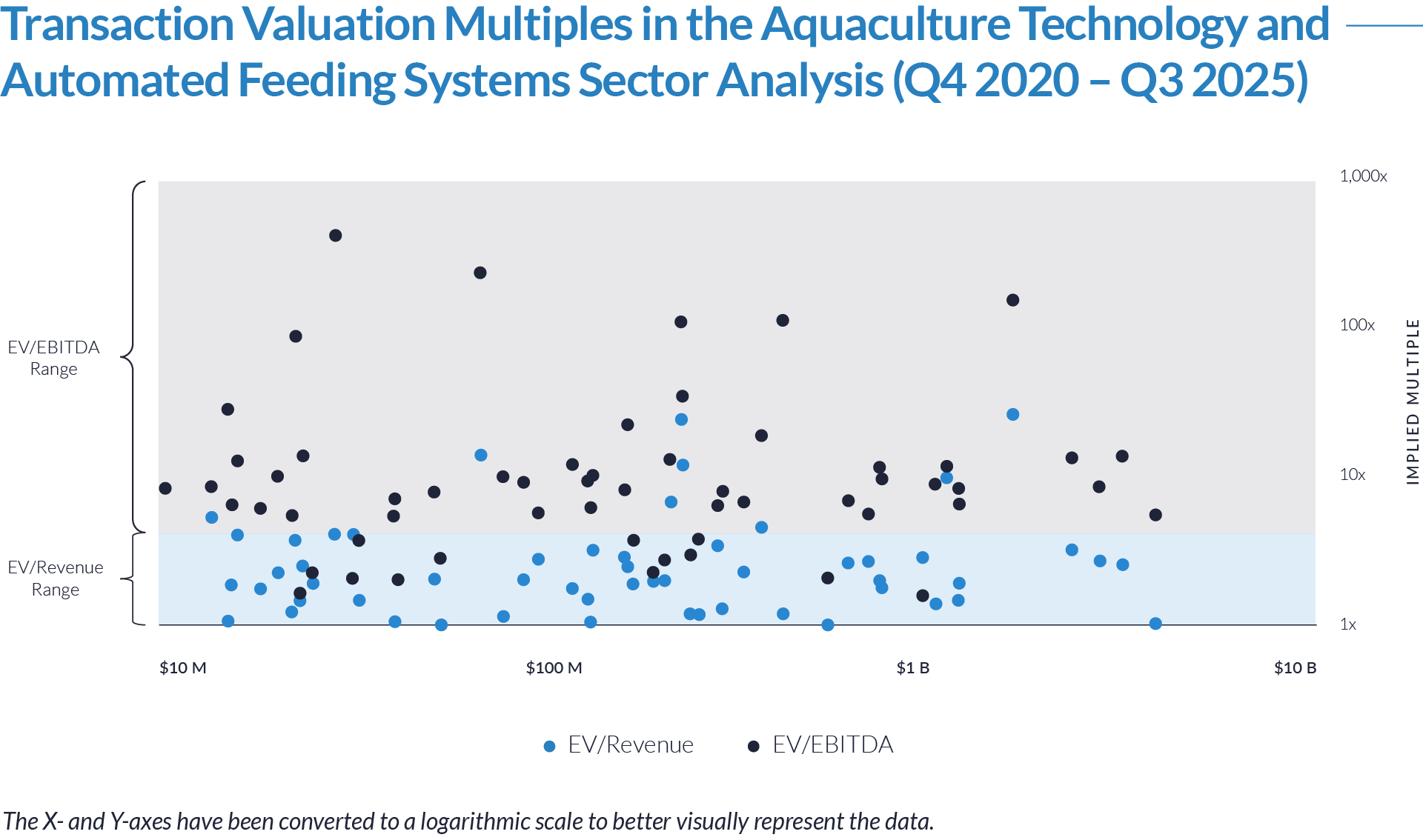

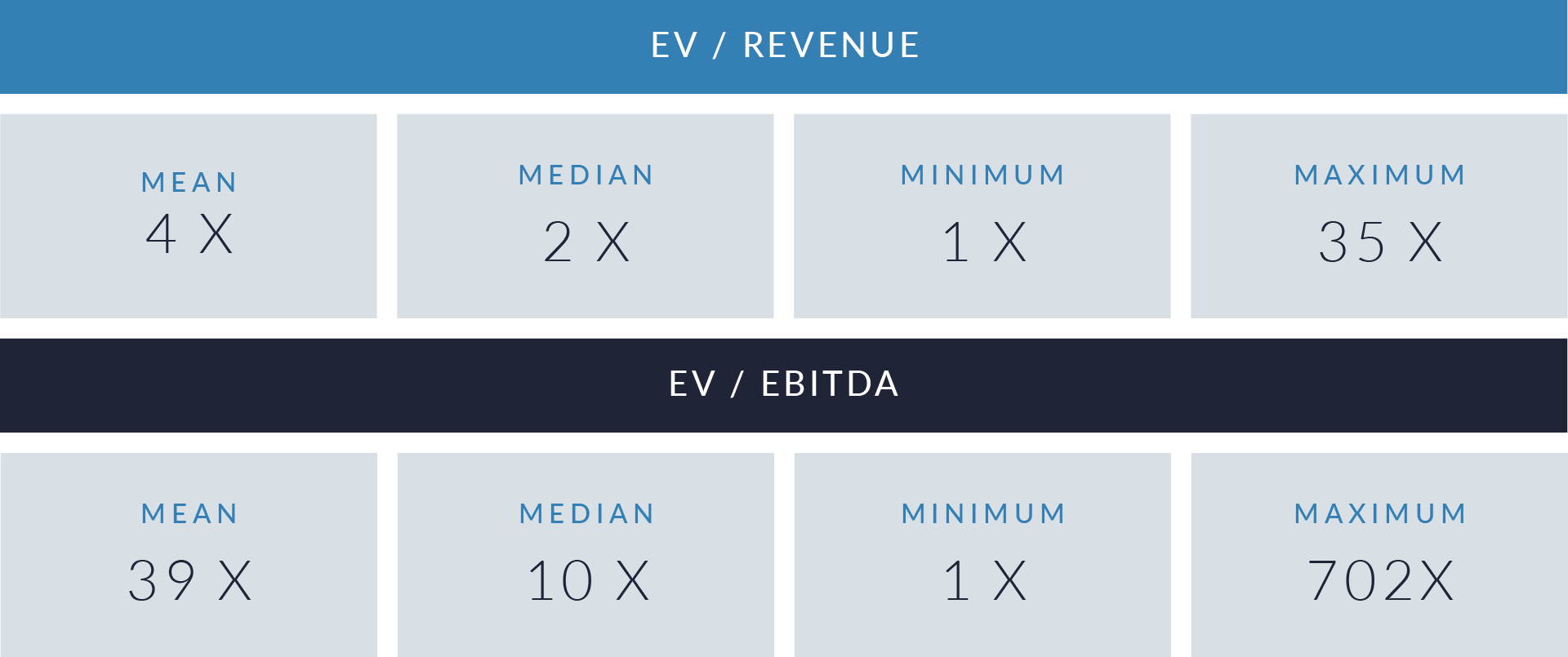

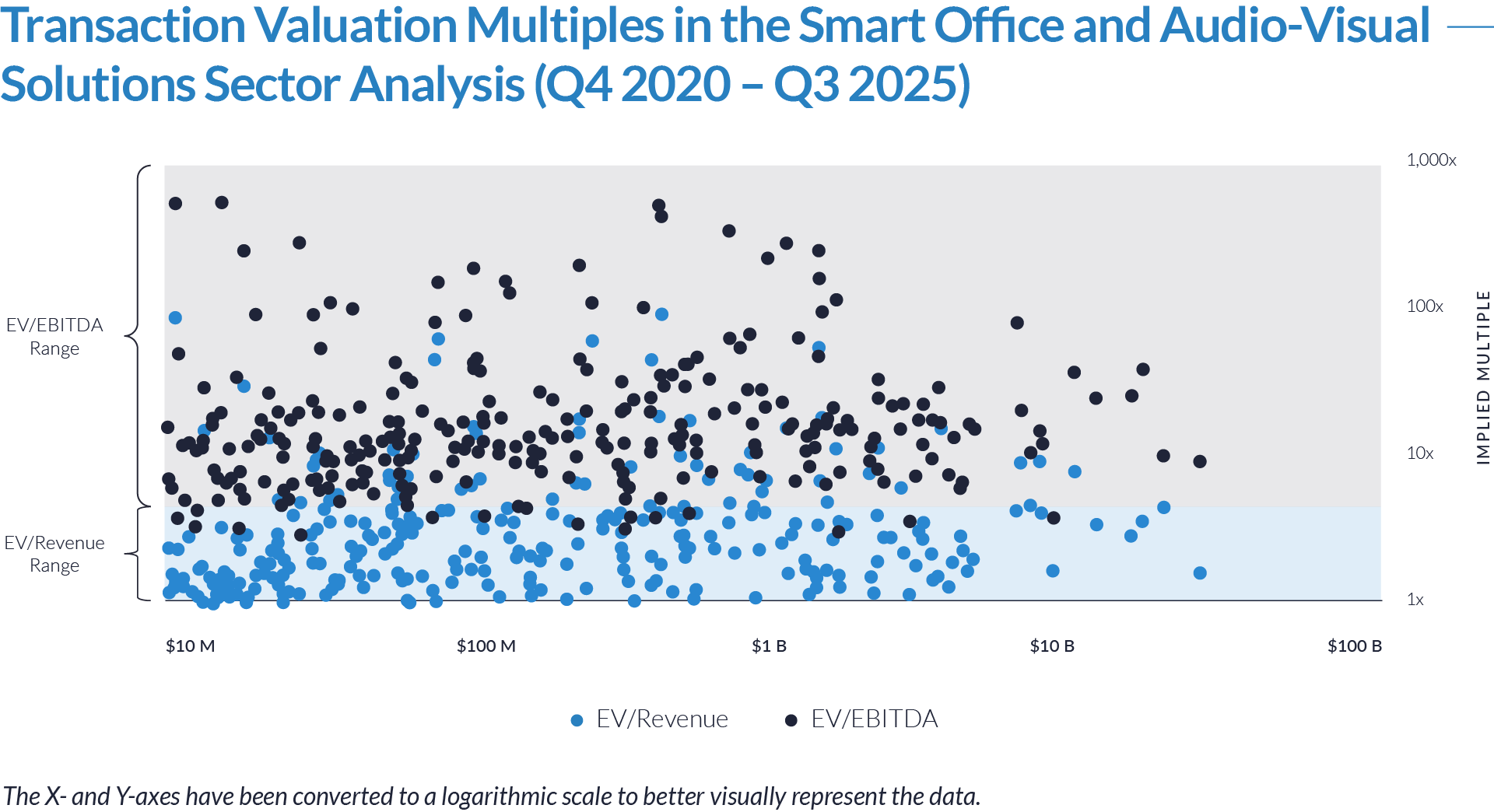

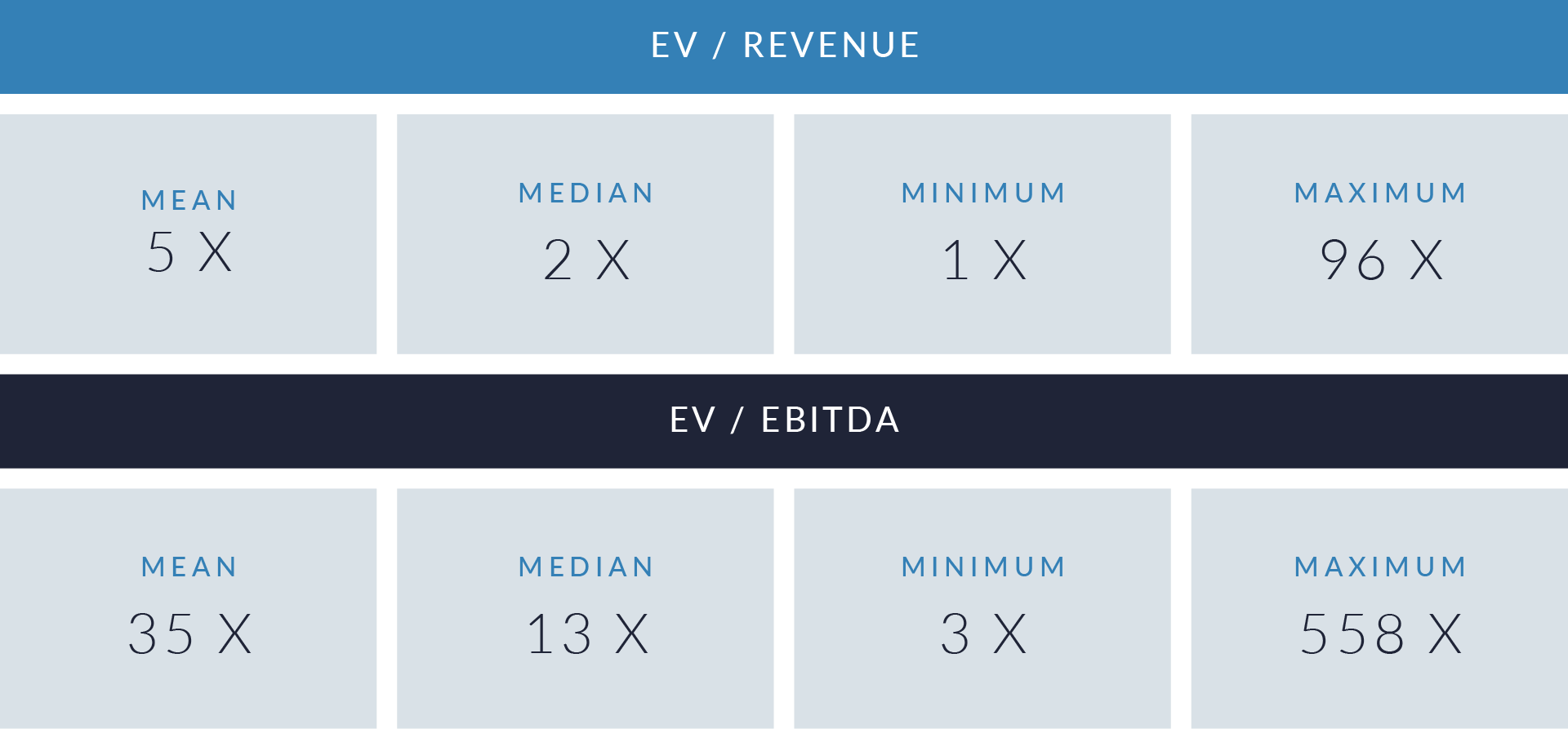

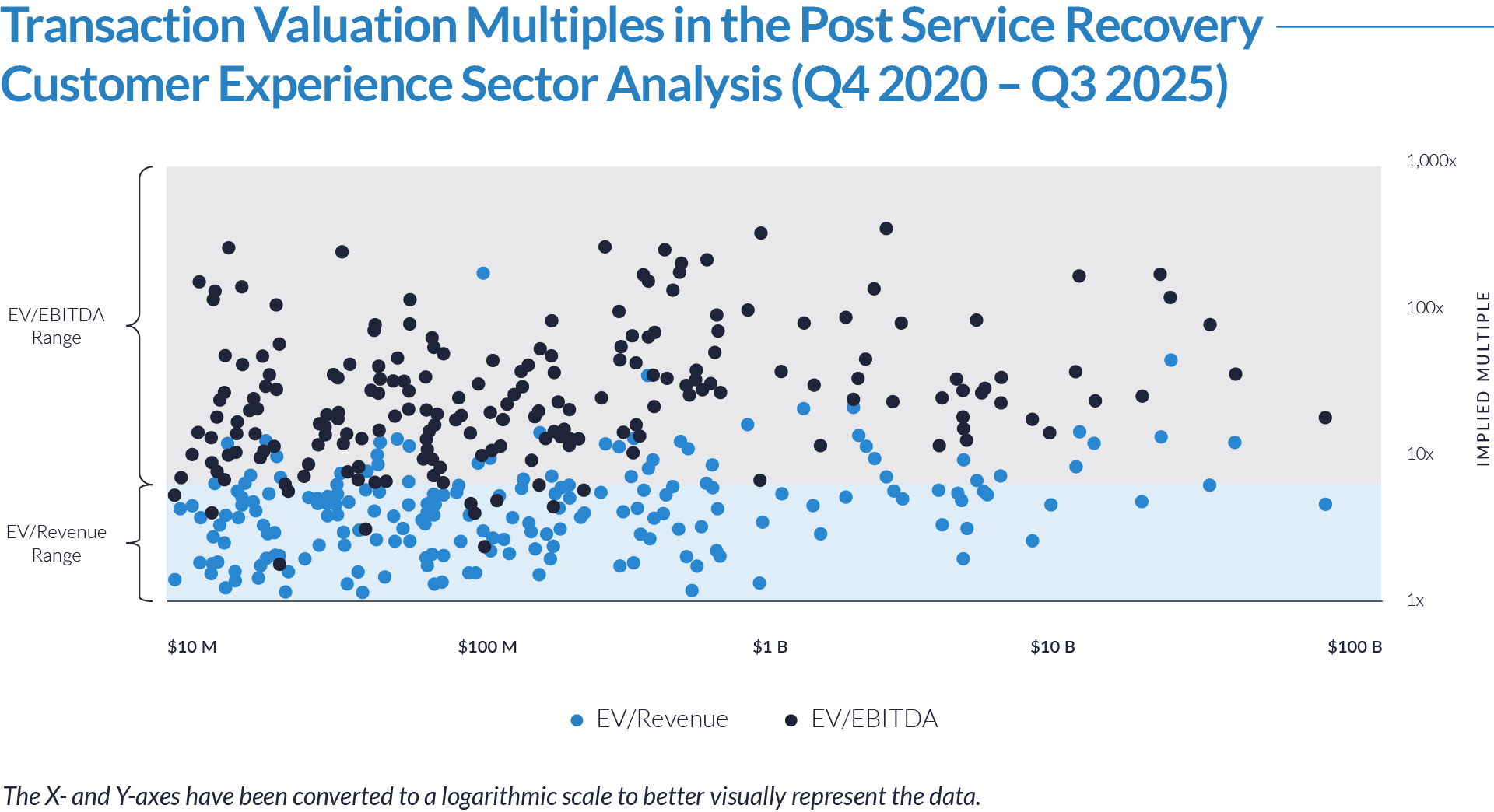

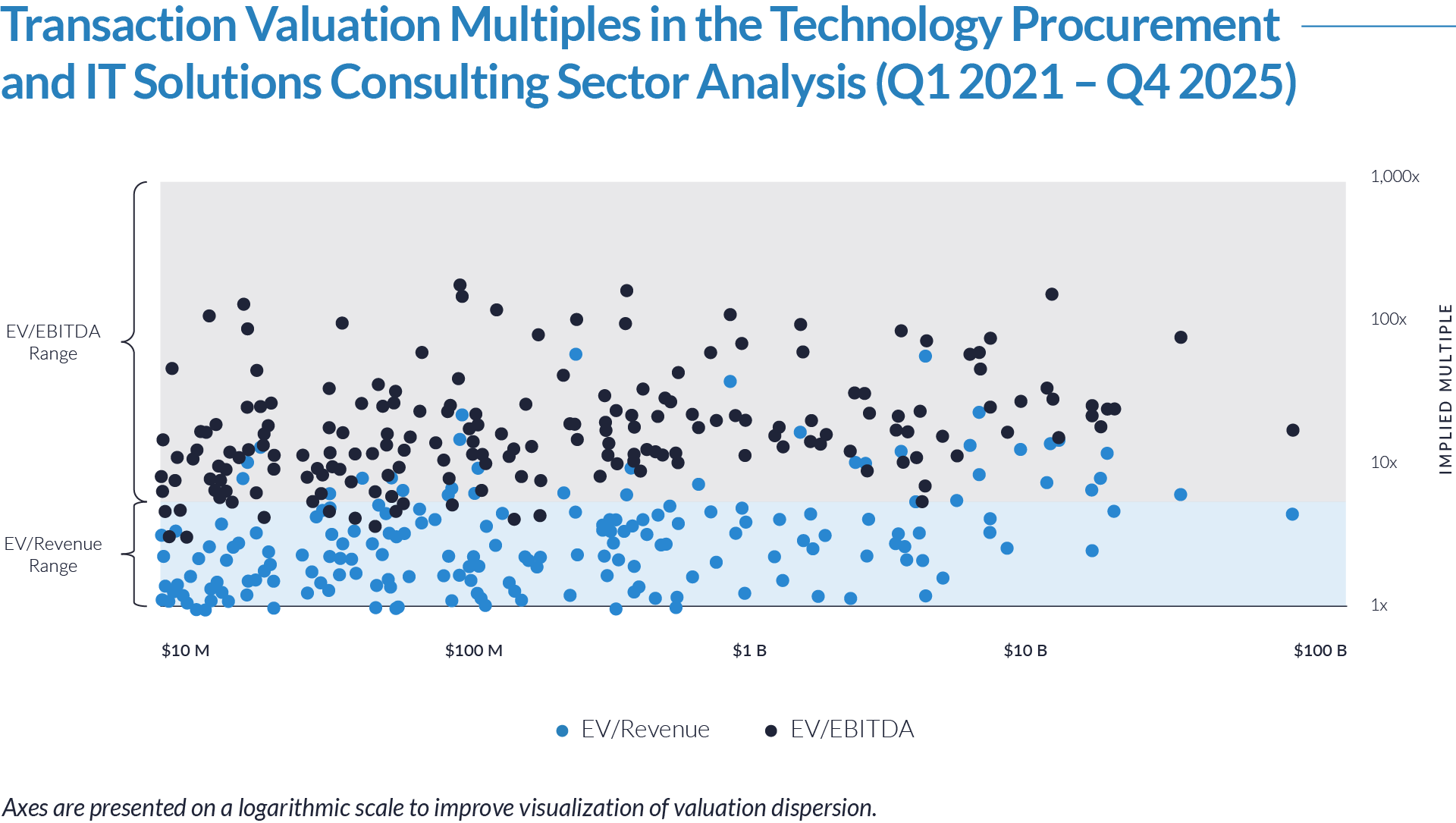

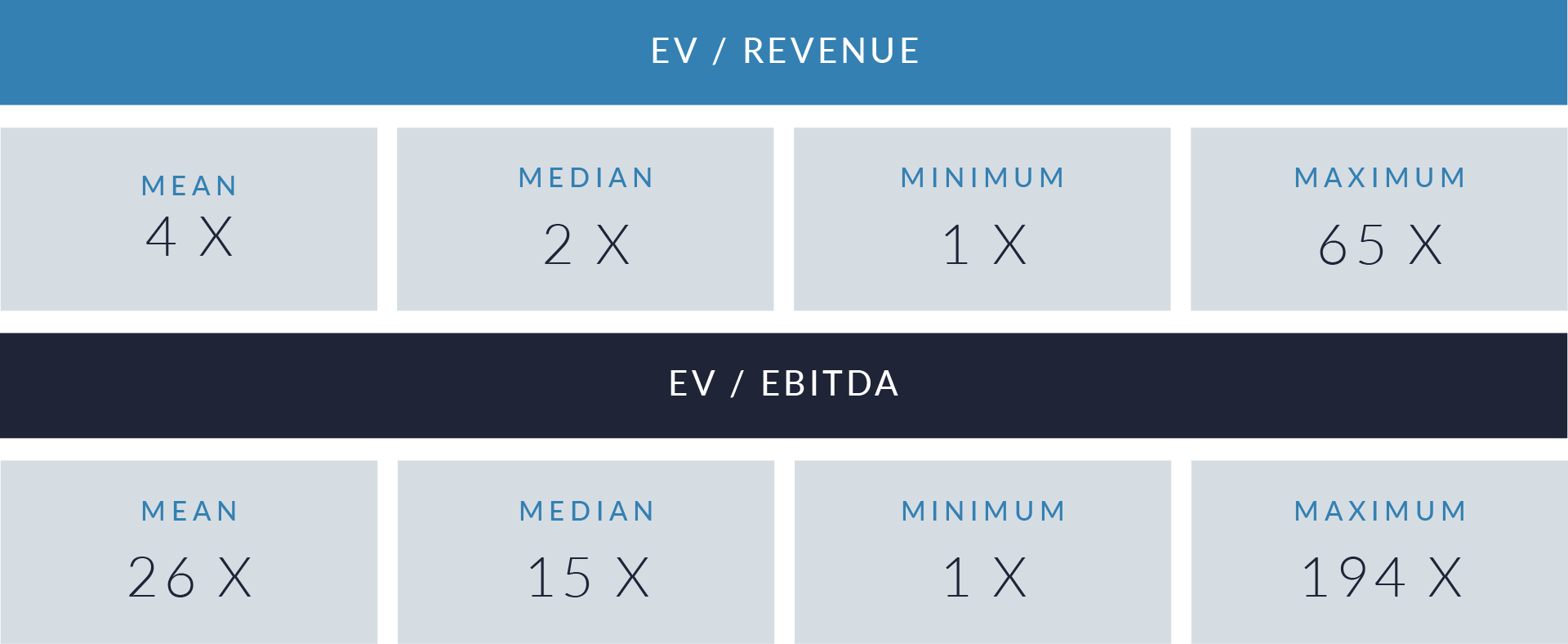

- Valuation multiples are based on a sample set of M&A transactions in the technology procurement and IT solutions consulting sector using data collected as of February 12, 2026.

- Valuation dispersion across the sector remains significant, with EV/revenue multiples ranging from approximately 1x to over 60x and EV/EBITDA multiples spanning from low single digits to well above 100x. Premium valuations are concentrated among scaled, technology-enabled platforms with strong client integration and recurring revenue visibility, while smaller or slower-growth advisory businesses transact at materially lower multiples.

- Despite headline outliers, the dataset shows a clear concentration of transactions between approximately 2x and 6x EV/revenue, indicating a normalized valuation band for established technology procurement and IT advisory platforms. This range reflects balanced underwriting assumptions around revenue durability, margin expansion potential, and client retention within a more disciplined post-2021 capital environment.

- The elevated and highly variable EV/EBITDA multiples indicate that many transactions price in forward growth expectations and operating leverage rather than current profitability. In several cases, high EBITDA multiples reflect reinvestment-heavy operating models or temporarily depressed earnings, reinforcing that revenue quality, recurring commission or services revenue streams, and strategic positioning remain primary valuation drivers.

Capital Markets Activities

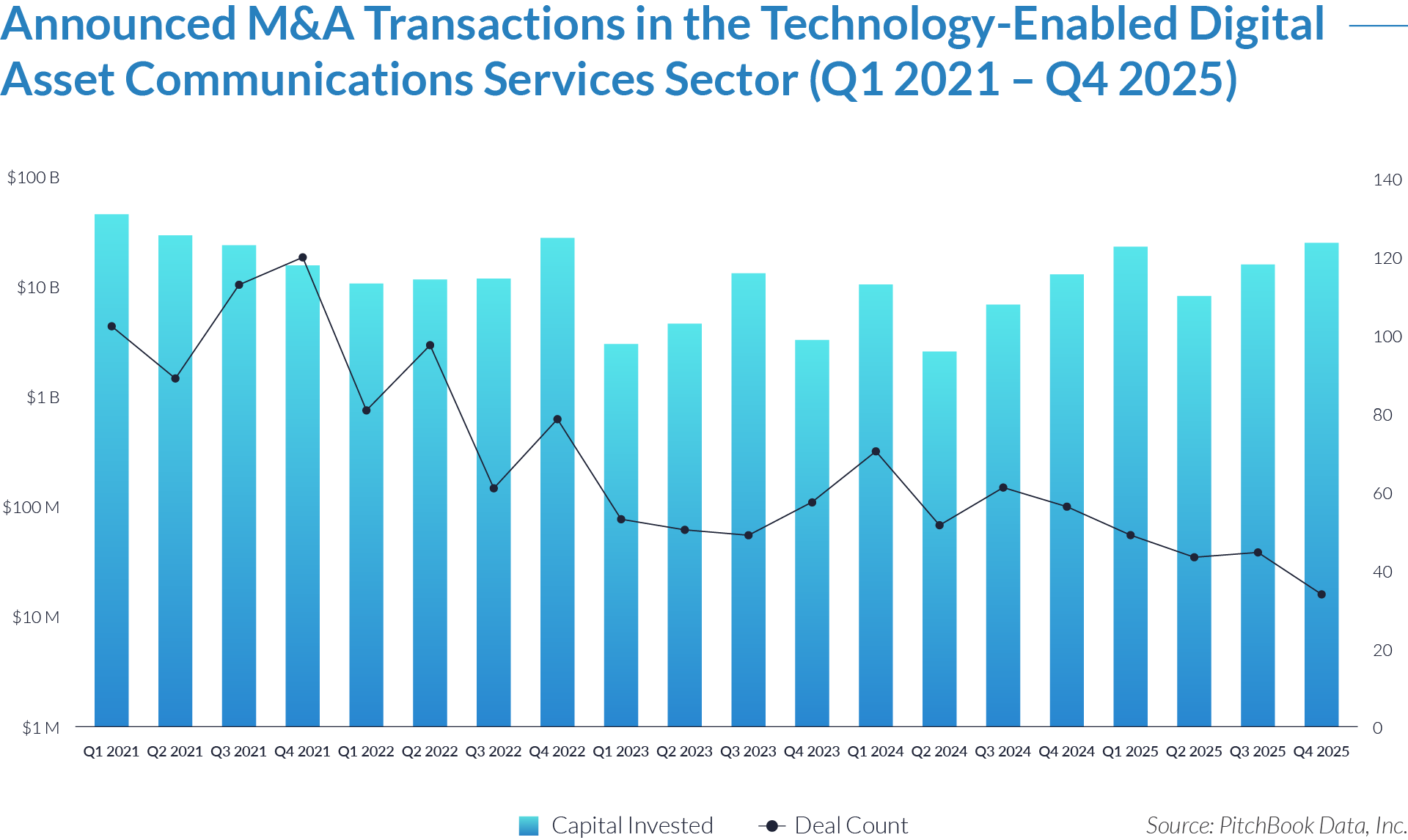

The data highlights transaction volume, capital deployment, deal structure, and geographic investment patterns across the technology procurement and IT solutions consulting sector. Accelerating enterprise digital transformation, increasing IT infrastructure complexity, and the expansion of multi-vendor technology ecosystems continue to drive consolidation among procurement intermediaries and IT advisory platforms. Strategic acquirers and financial sponsors are prioritizing scalable, asset-light consulting and brokerage models embedded within enterprise technology purchasing workflows, favoring platforms with recurring commission and services-based revenue, diversified vendor relationships, and capabilities spanning cloud infrastructure, cybersecurity, telecom, and enterprise software solutions.

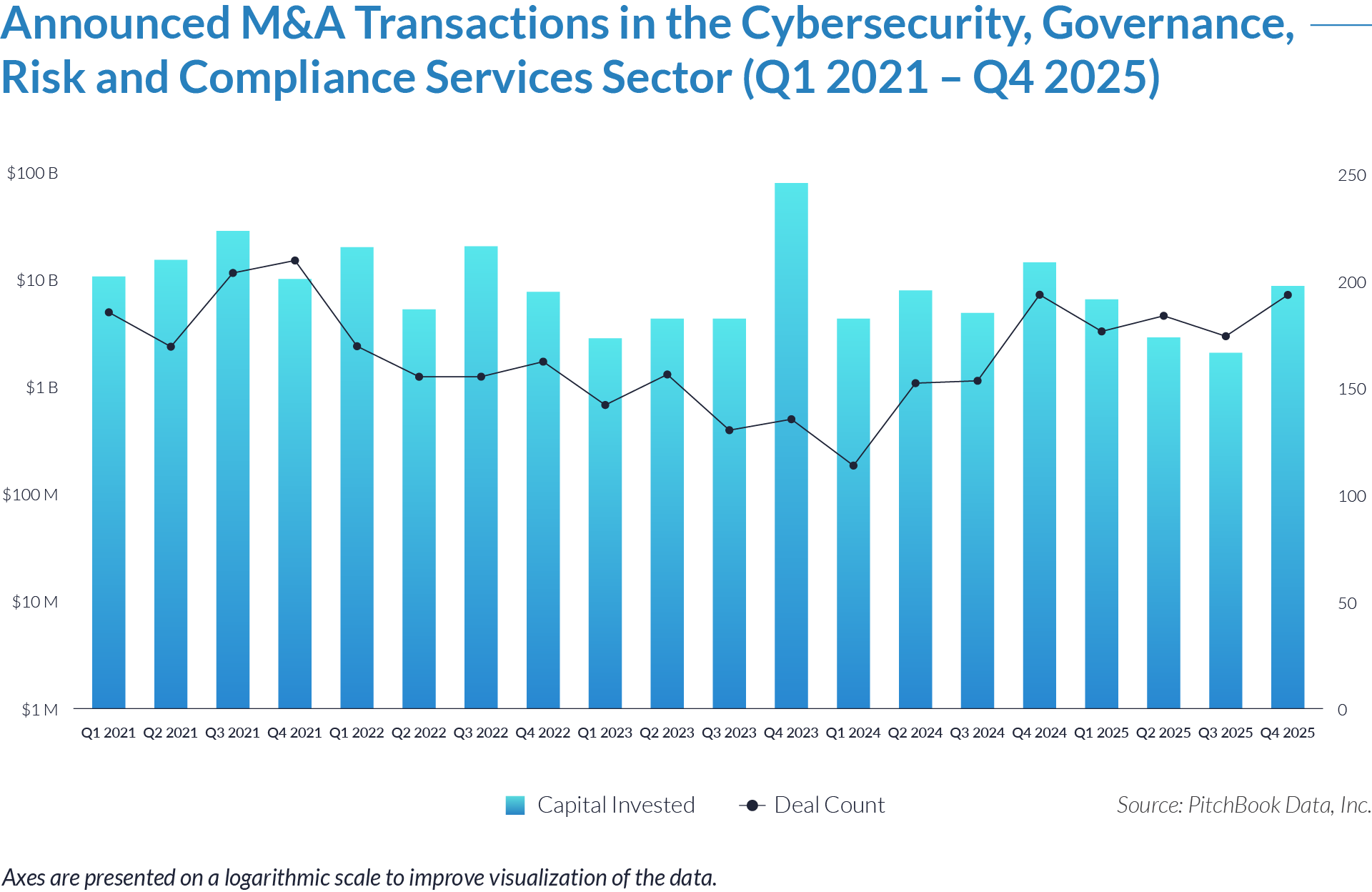

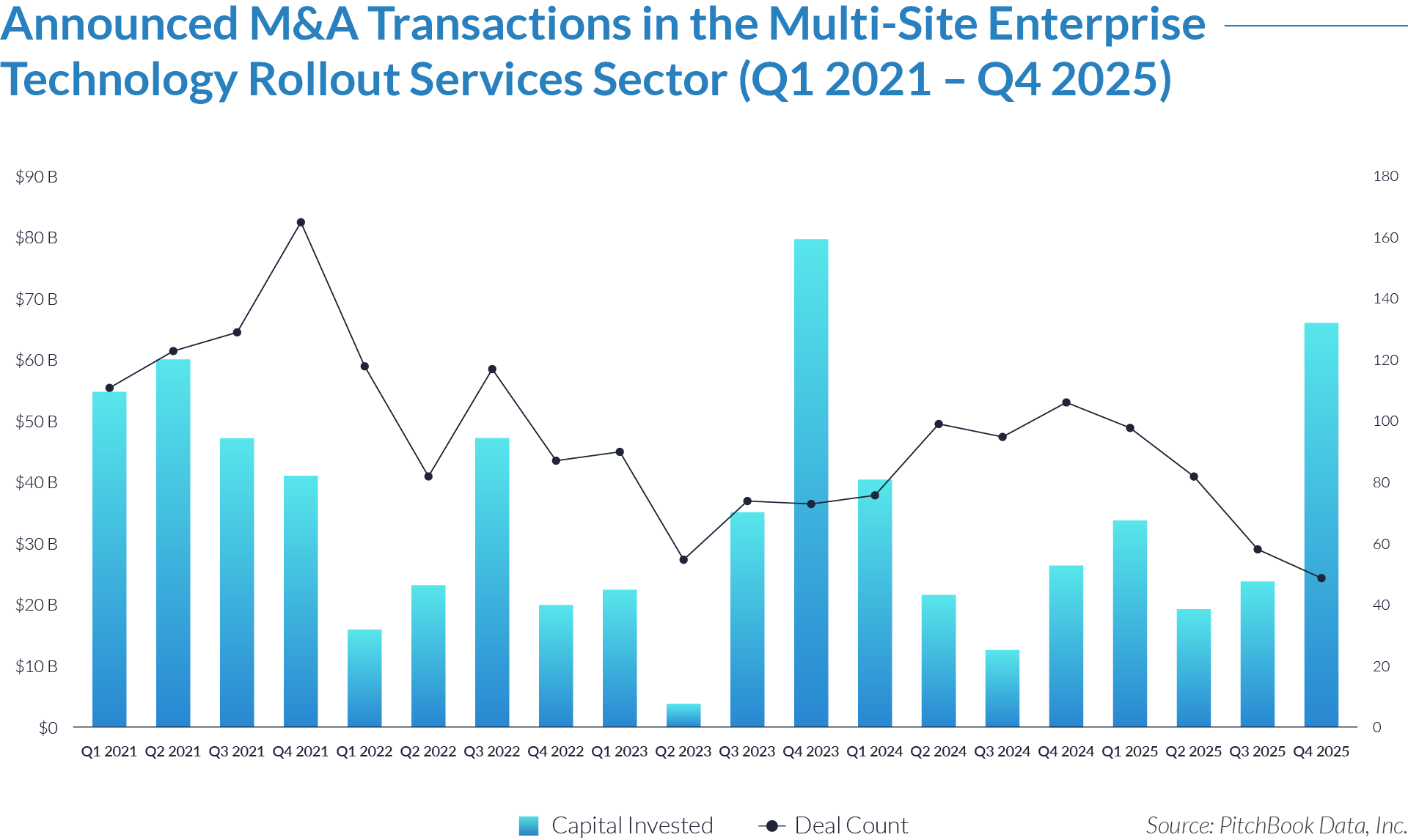

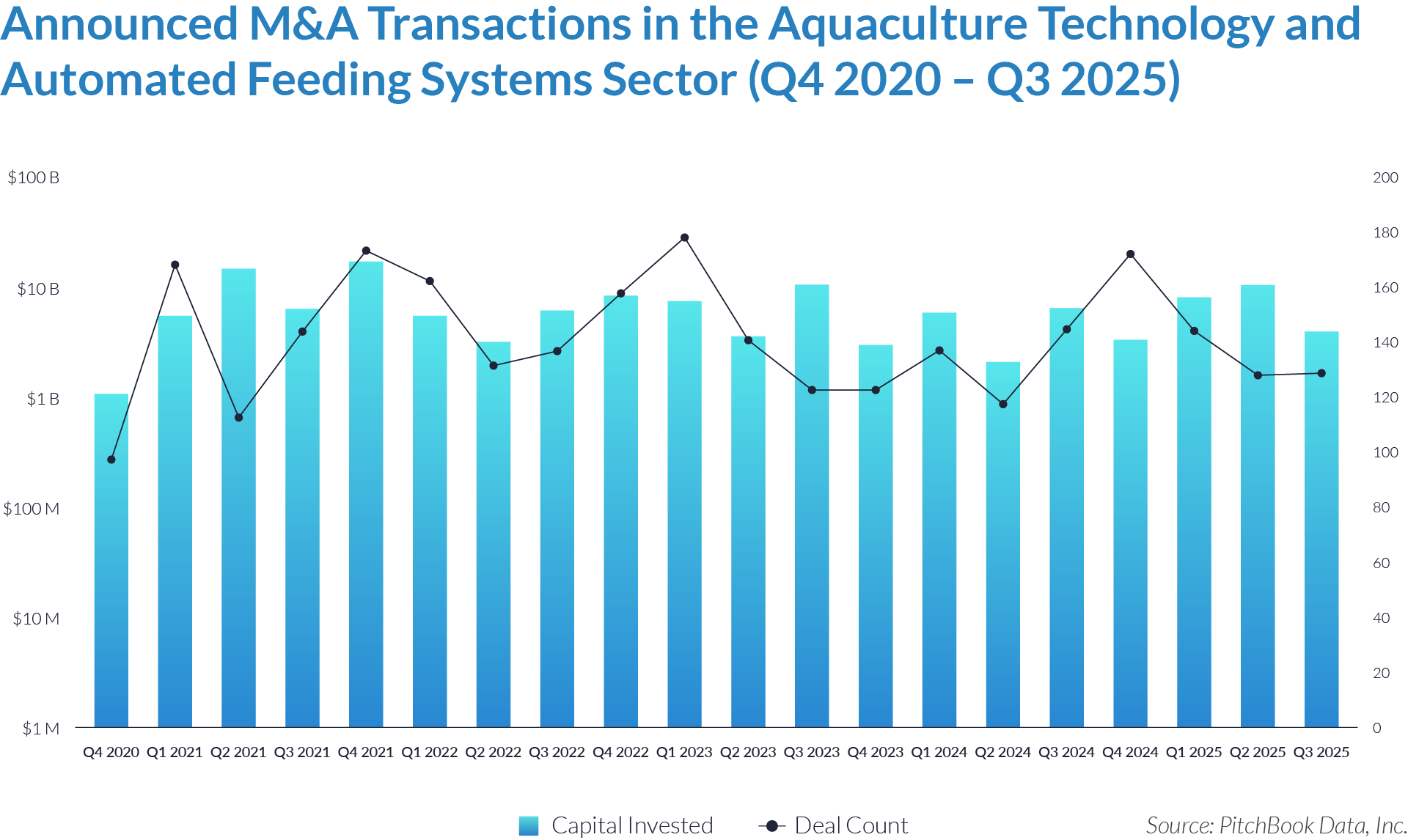

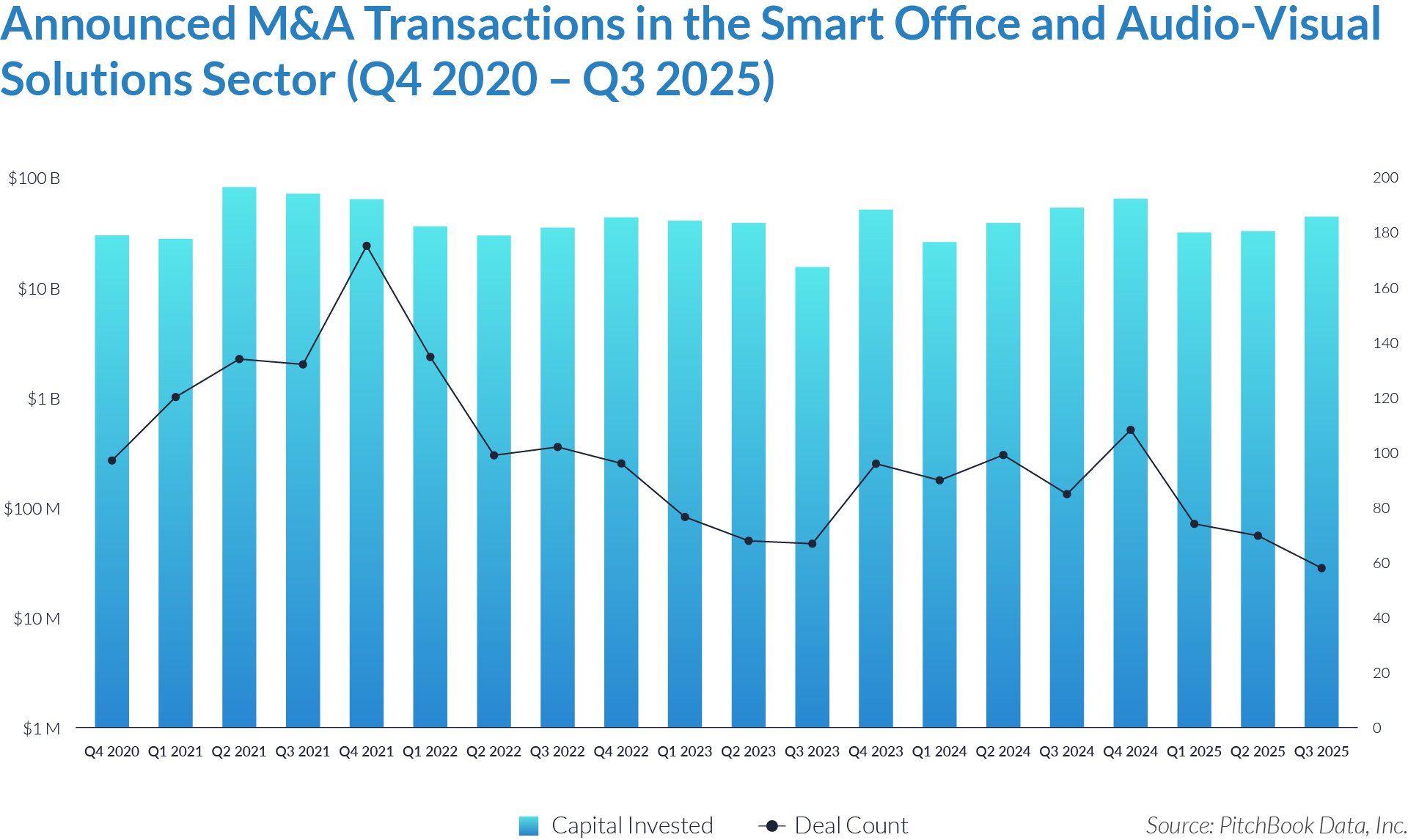

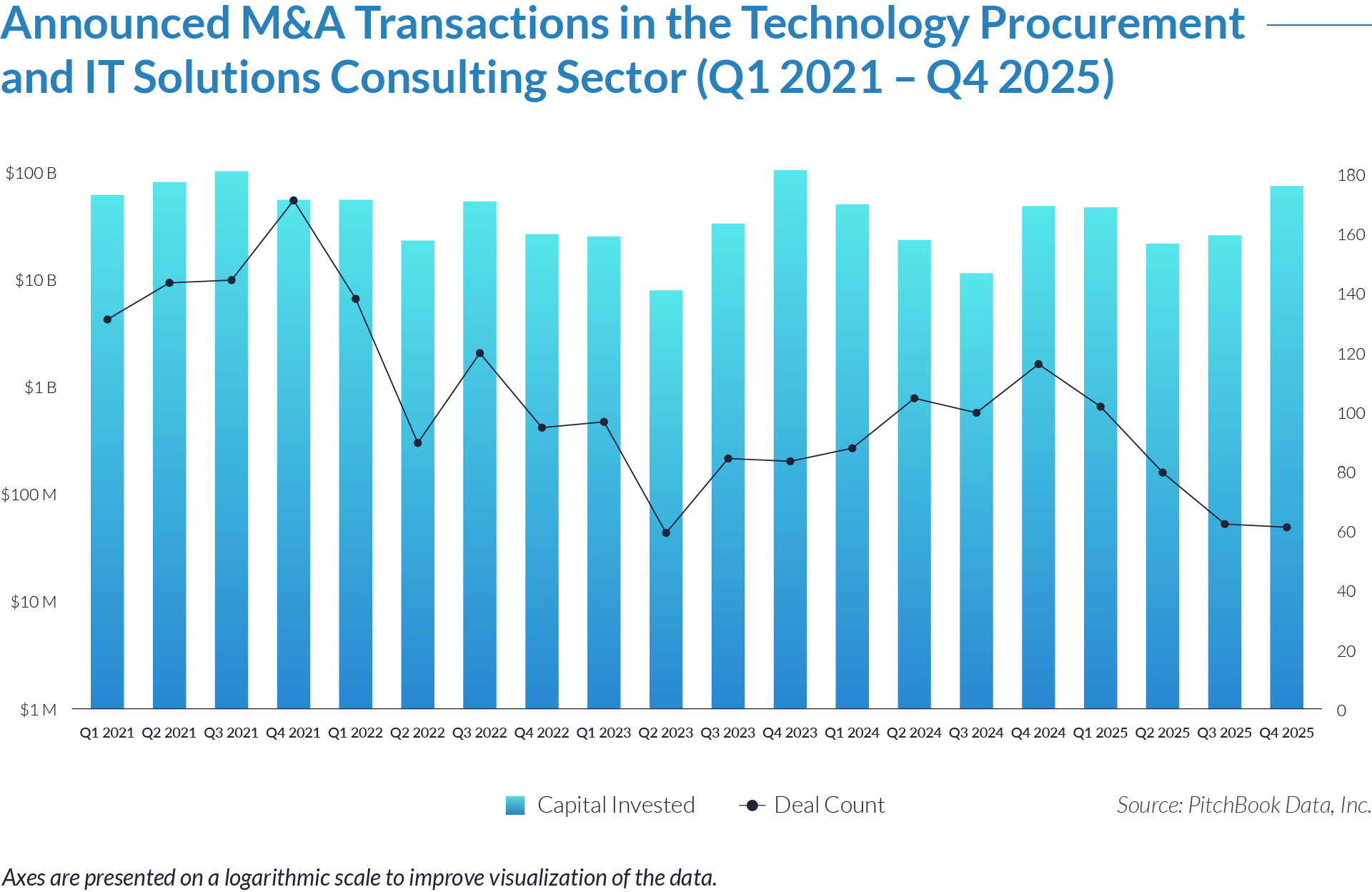

- Over the 20-quarter period, the sector recorded approximately $854 billion of total capital invested across 2,053 transactions, underscoring the strategic importance of technology procurement and IT solutions consulting platforms as mission-critical infrastructure within enterprise IT ecosystems. The scale of aggregate capital deployed signals sustained investor conviction in advisory-led, asset-light models despite broader macroeconomic volatility.

- Capital deployment reached elevated levels in 2021, with multiple quarters exceeding $70 billion to $93 billion, reflecting favorable financing conditions, strong valuation environments, and accelerated platform consolidation. This was followed by a pronounced normalization through 2022 and early 2023, when quarterly capital investment fell below $25 billion in several periods, including a trough of $7 billion in Q2 2023, indicating valuation compression, tighter financing conditions, and a shift toward more disciplined underwriting.

- The dataset reflects periodic capital spikes, notably in Q4 2023 and Q4 2025, when investment levels surged to $96 billion and $68 billion, respectively, despite relatively moderate deal counts. This divergence between capital invested and transaction volume suggests the presence of large-scale platform acquisitions and sponsor-led transactions, reinforcing the bifurcation between scaled, market-leading advisory platforms and smaller tuck-in acquisitions.

- While deal activity peaked at 169 transactions in Q4 2021, volumes generally trended lower through 2023–2025, stabilizing at approximately 60 to 100 deals per quarter. Capital investment rebounded selectively in 2024 and 2025, implying a market characterized by fewer but larger and higher-quality transactions, with acquirers prioritizing scaled, recurring-revenue platforms embedded within enterprise technology procurement and vendor management workflows.

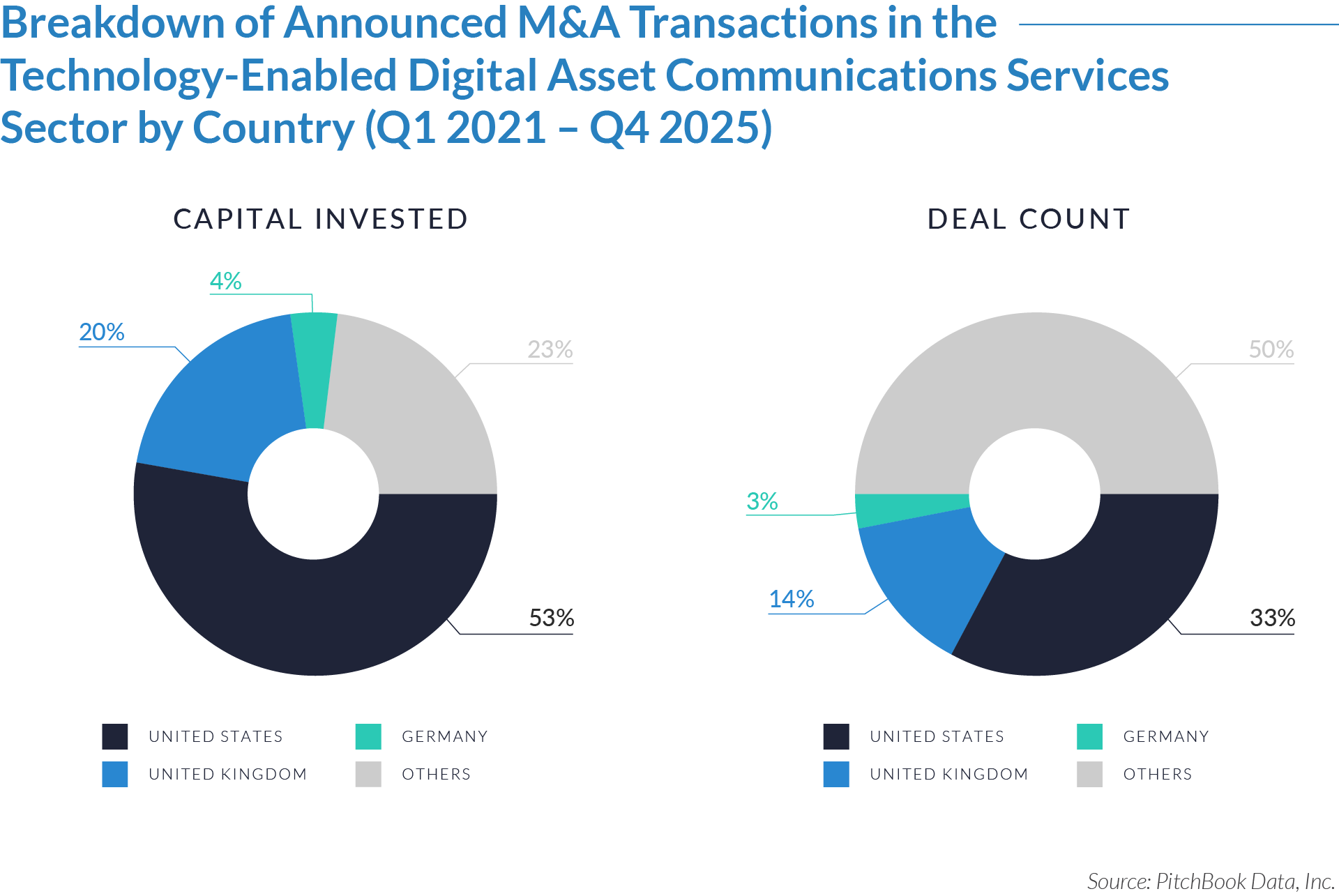

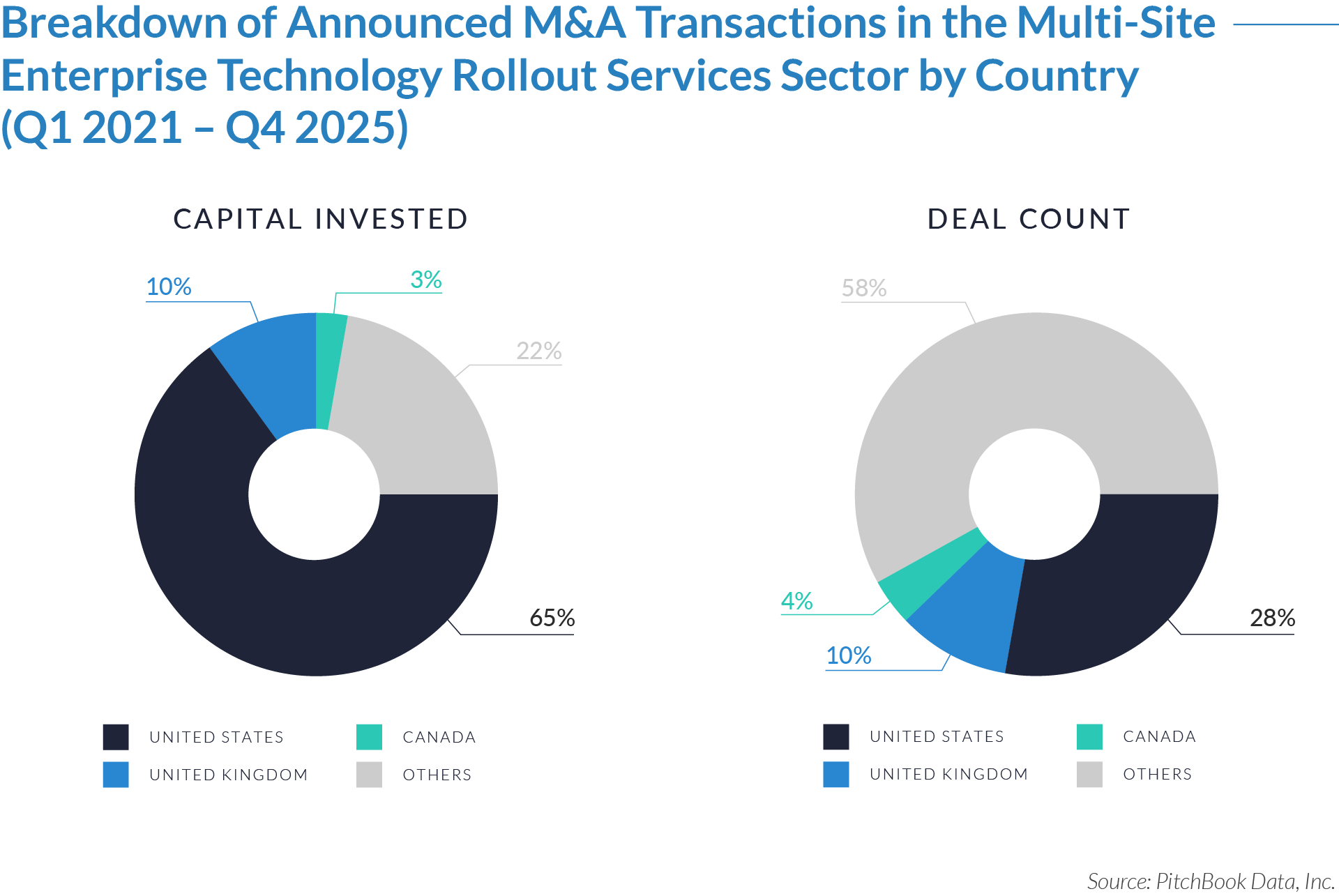

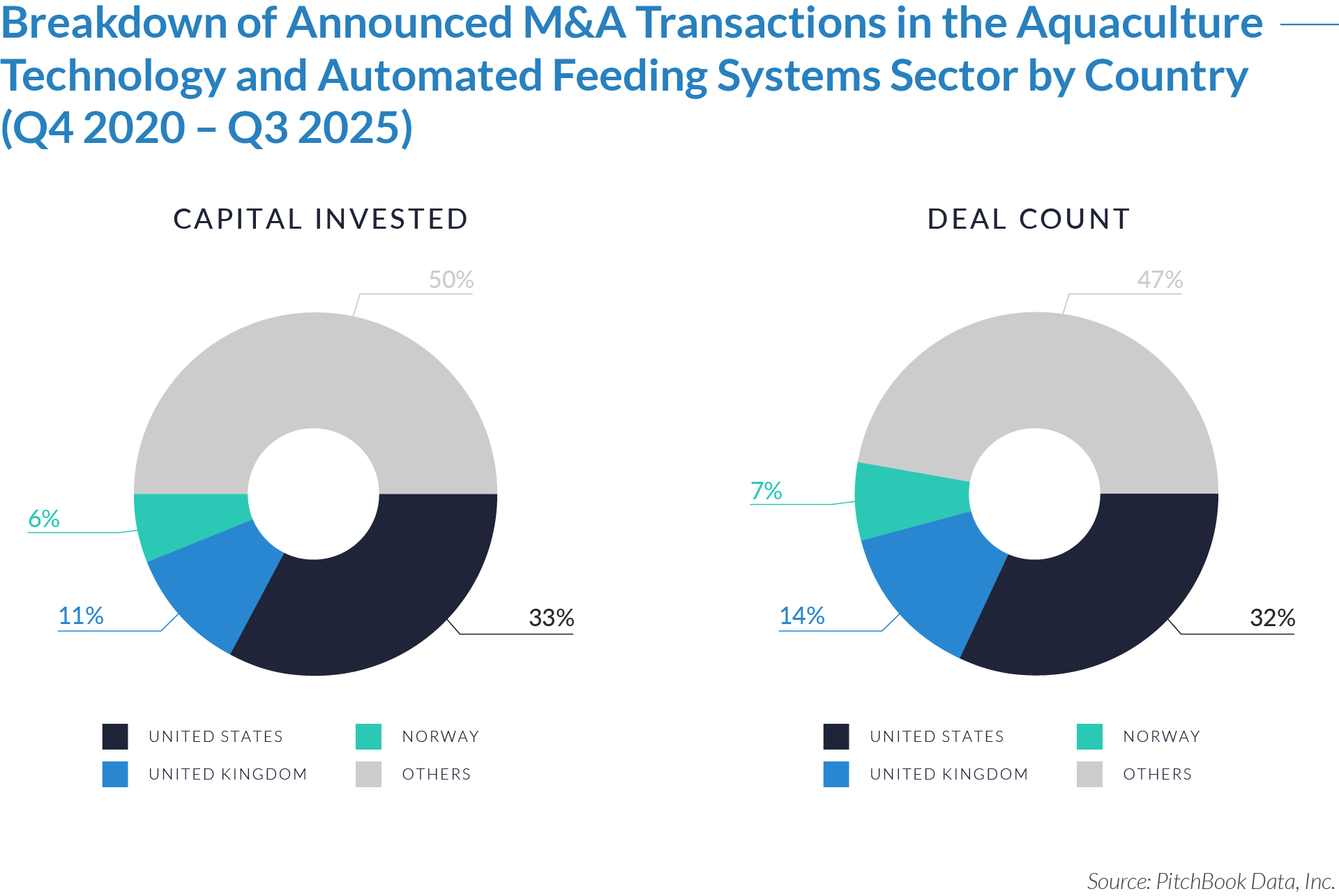

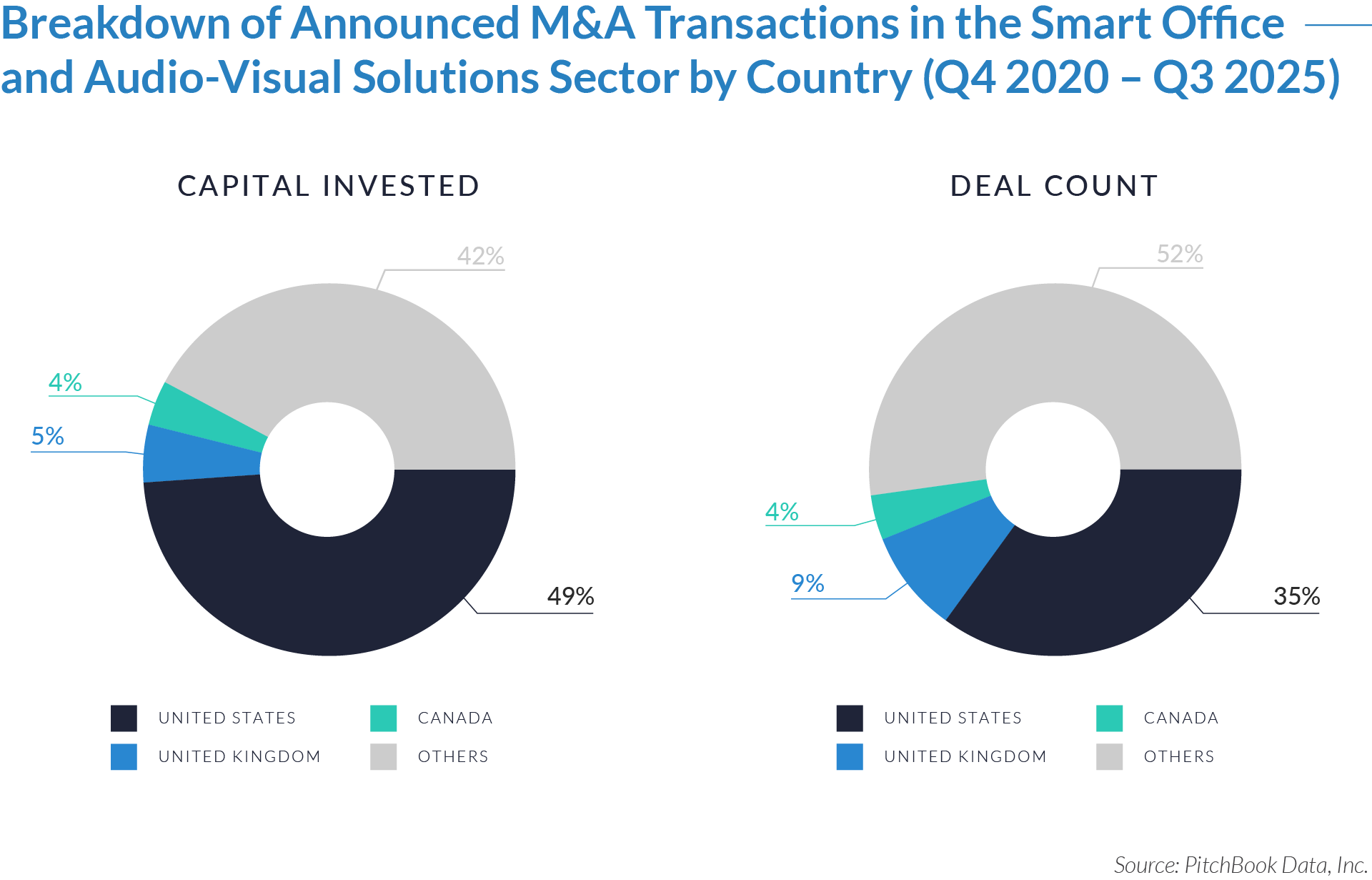

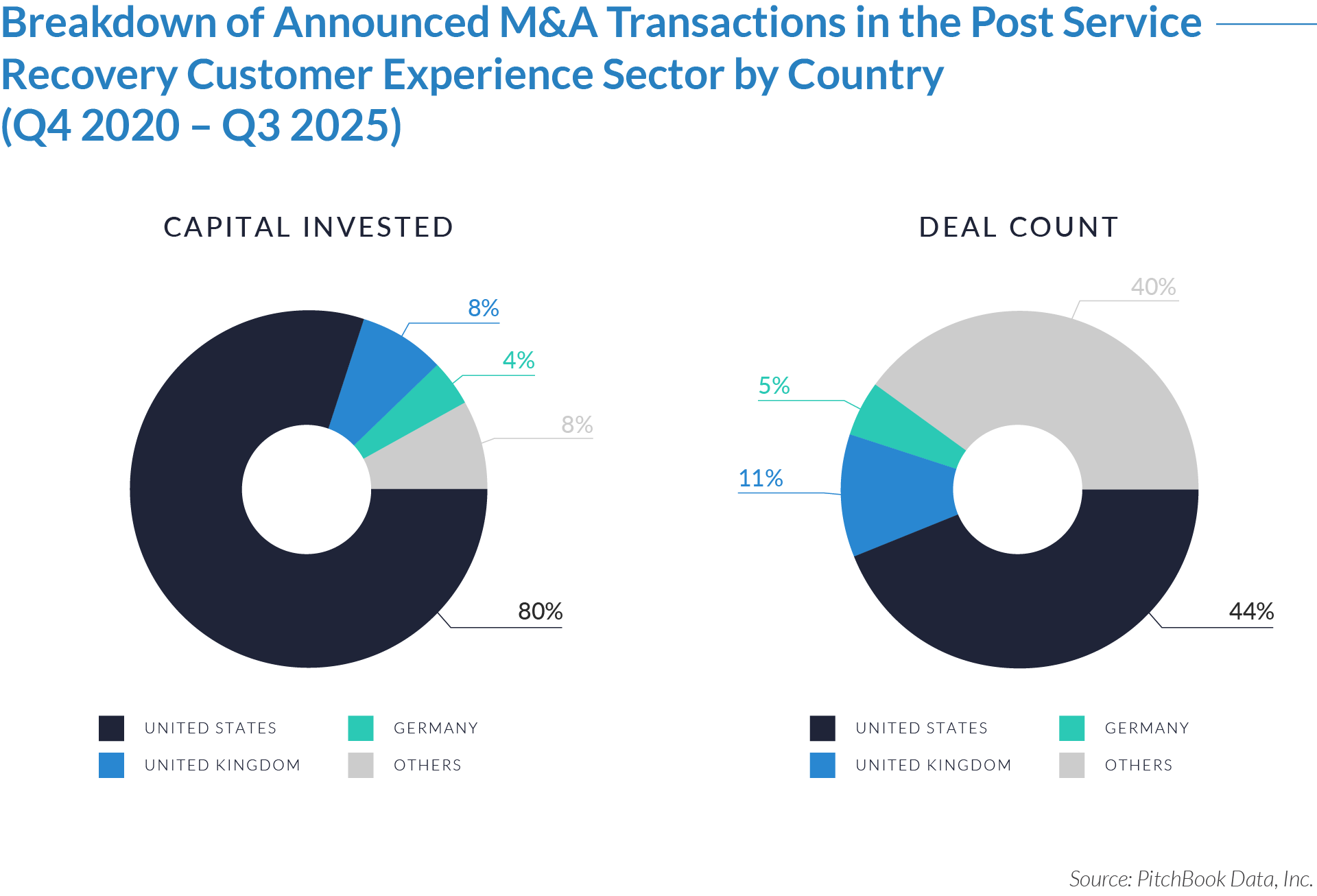

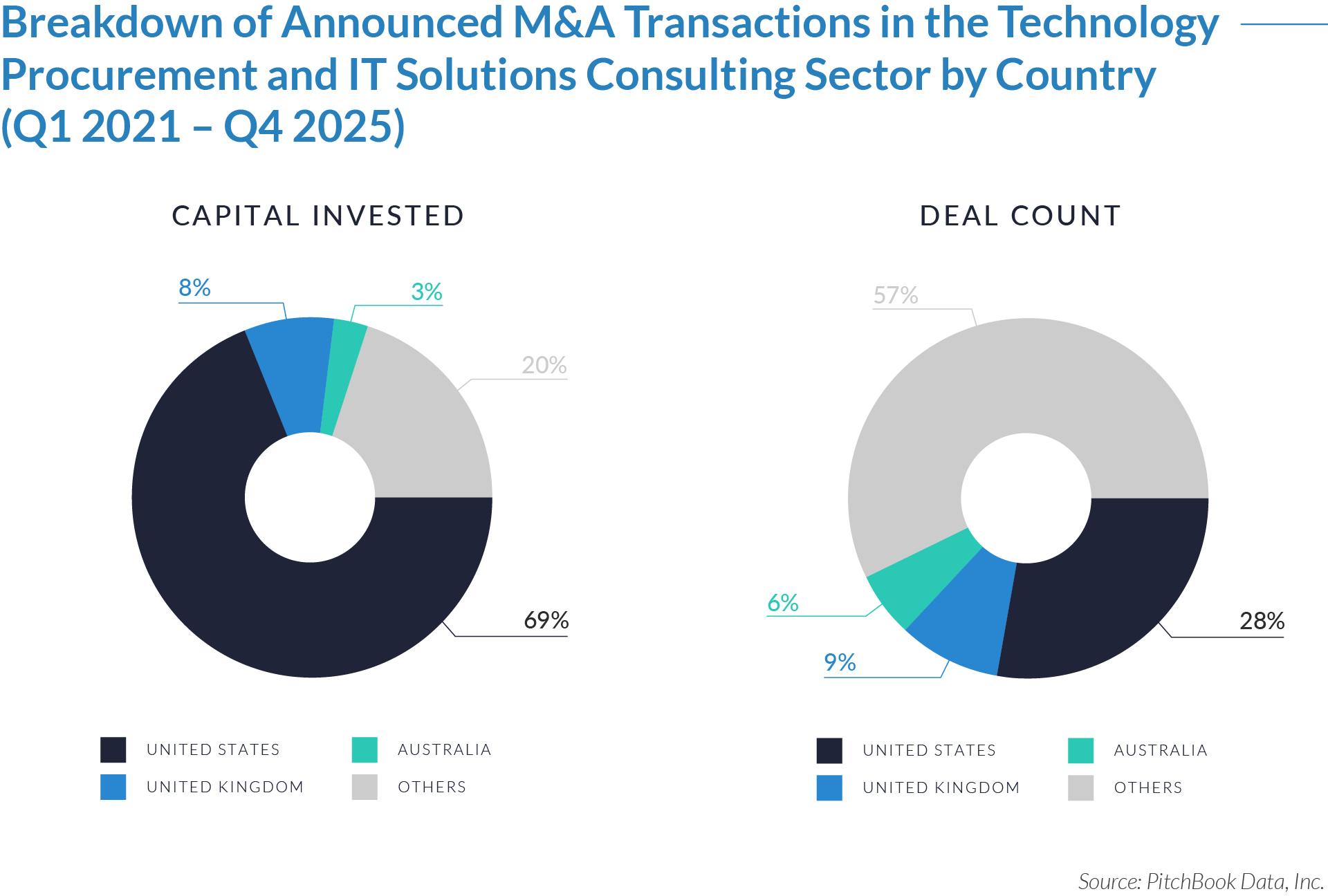

- The United States accounts for approximately 69% of total capital invested, yet represents only 28% of total deal count. This imbalance reflects larger average transaction sizes in US-led deals and underscores the role of US strategic acquirers and financial sponsors as primary global consolidators within the technology procurement and IT solutions consulting sector. Deep capital markets and a mature ecosystem of advisory and brokerage platforms position US buyers to execute large-scale platform acquisitions and pursue cross-border expansion strategies.

- The United Kingdom accounts for 8% of invested capital and 9% of deal count, indicating a relatively balanced relationship between capital deployment and transaction activity. The UK’s established technology services ecosystem, supported by a strong venture capital environment and a concentration of advisory and managed services providers, positions the country as a key market for technology procurement and IT solutions consulting activity.

- Australia accounts for 3% of invested capital and 5% of deal count, reflecting an active but smaller-scale domestic market. The country’s advanced enterprise IT adoption and growing demand for outsourced procurement and advisory services support steady transaction activity, positioning Australia as a regional hub for technology services and IT advisory consolidation within the broader Asia-Pacific market.

- Other international markets account for approximately 20% of capital invested, while they represent 57% of total deal count, highlighting a highly fragmented global transaction landscape. This distribution suggests smaller average deal sizes across international markets, where technology procurement and IT advisory platforms remain more fragmented and continue to attract incremental consolidation opportunities across Europe, Asia, and other regions.

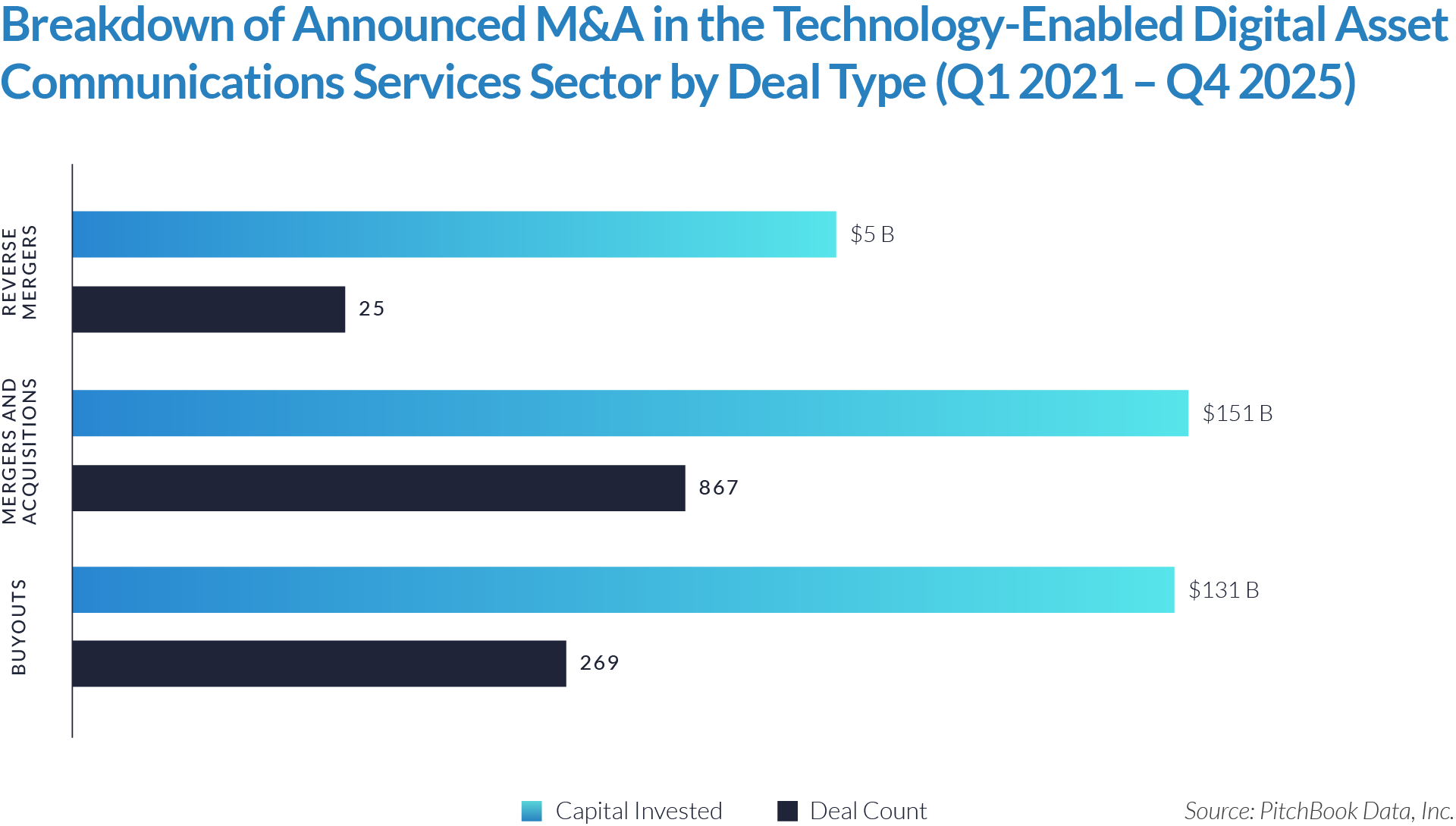

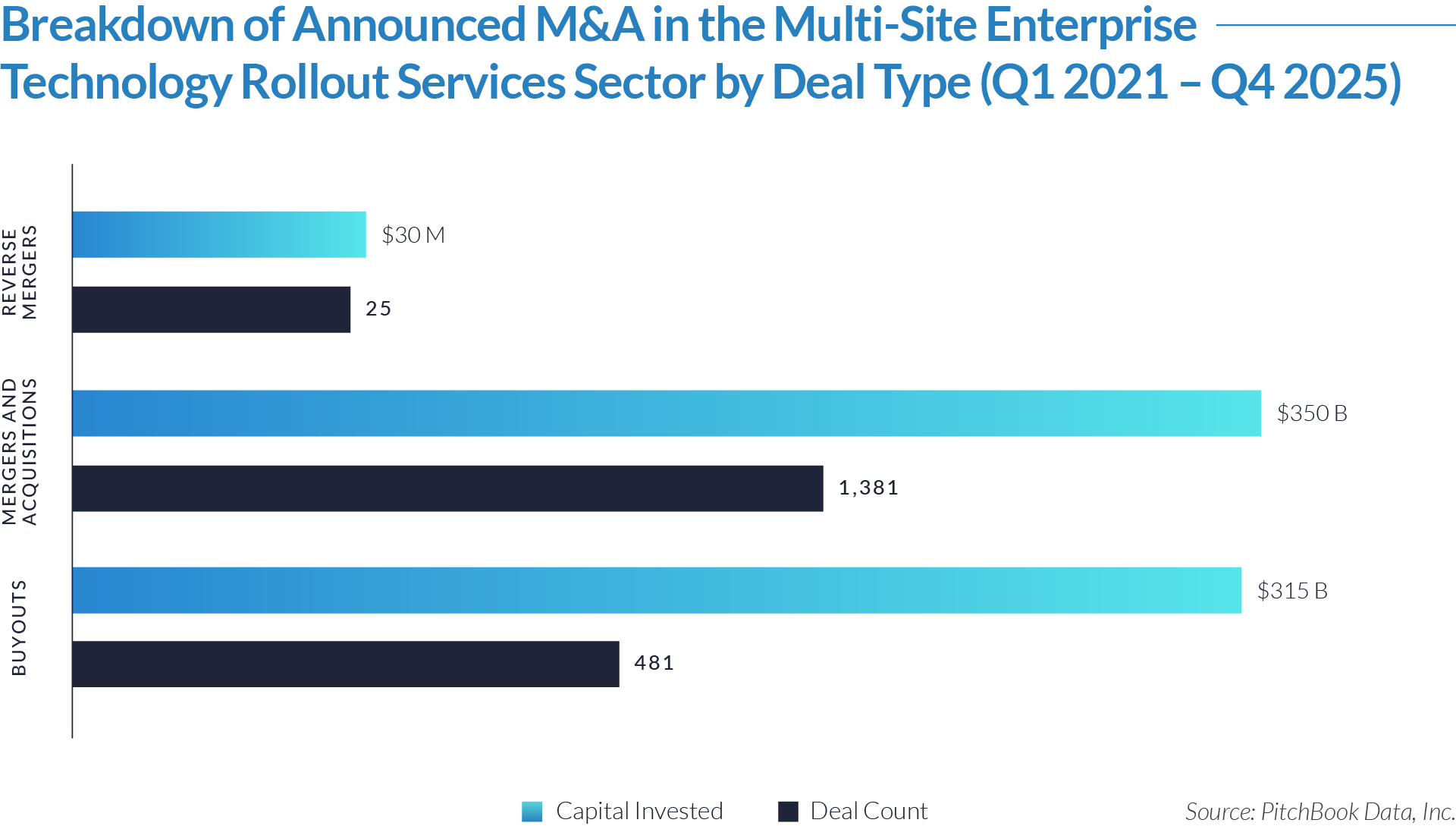

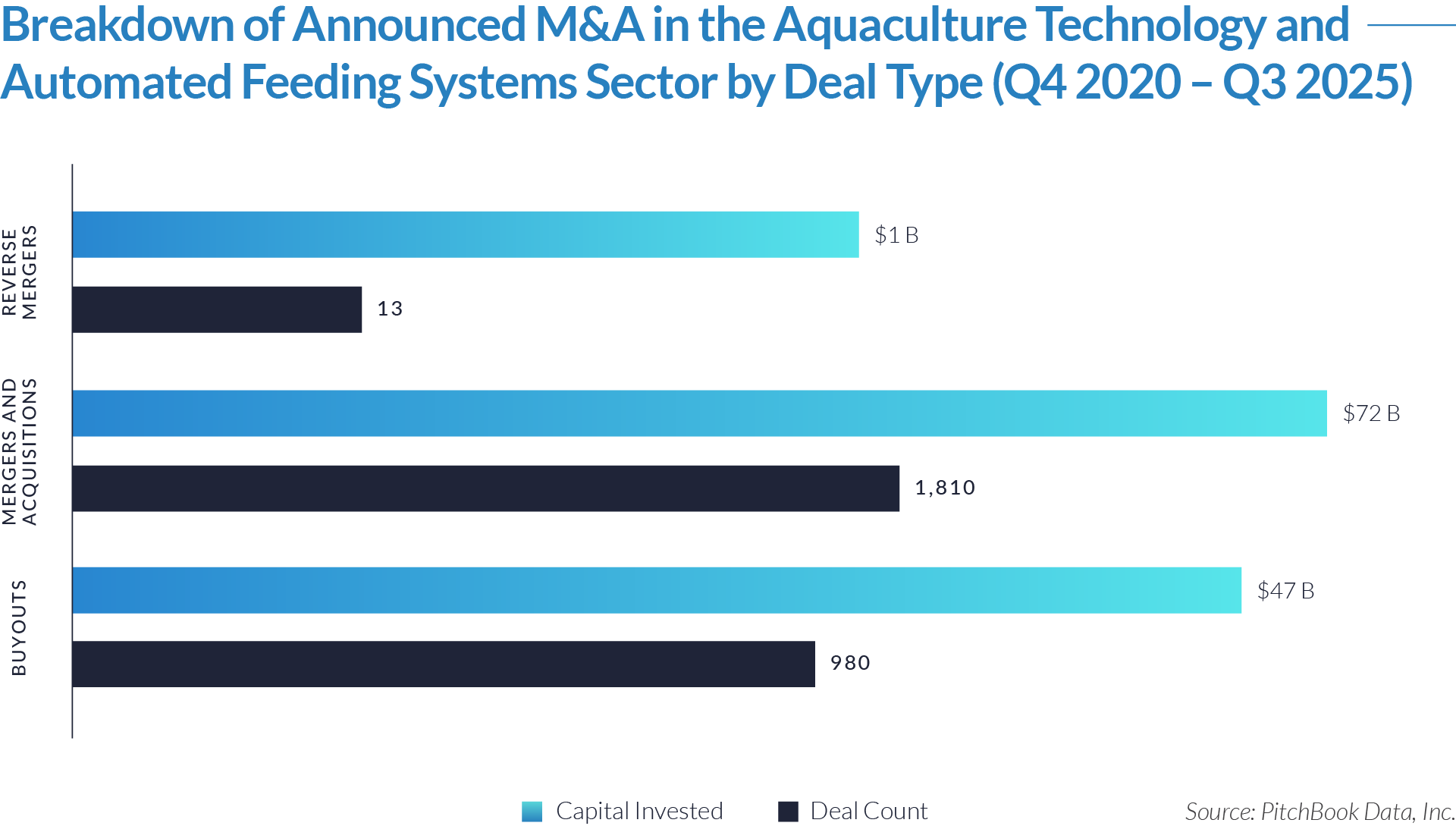

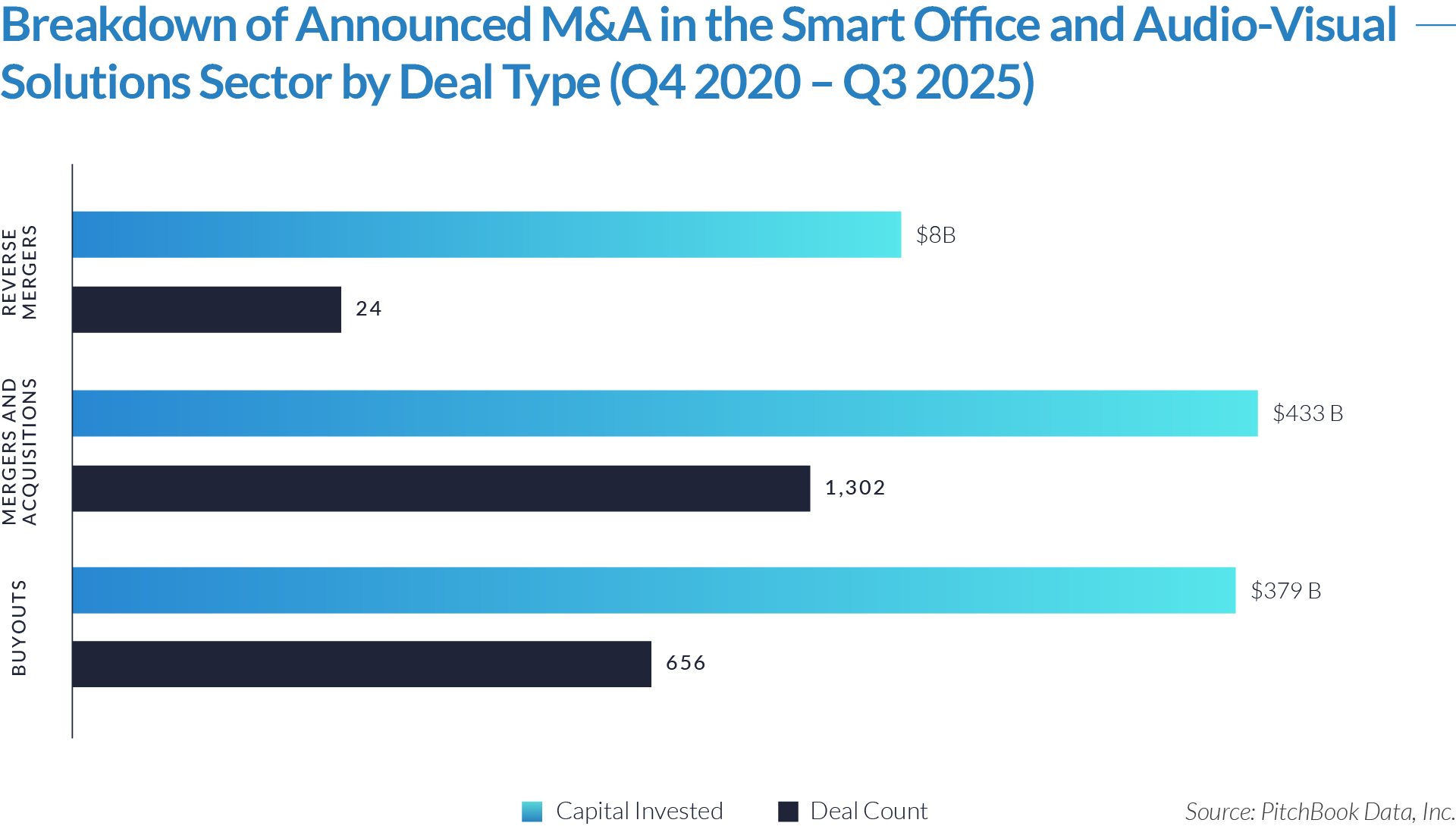

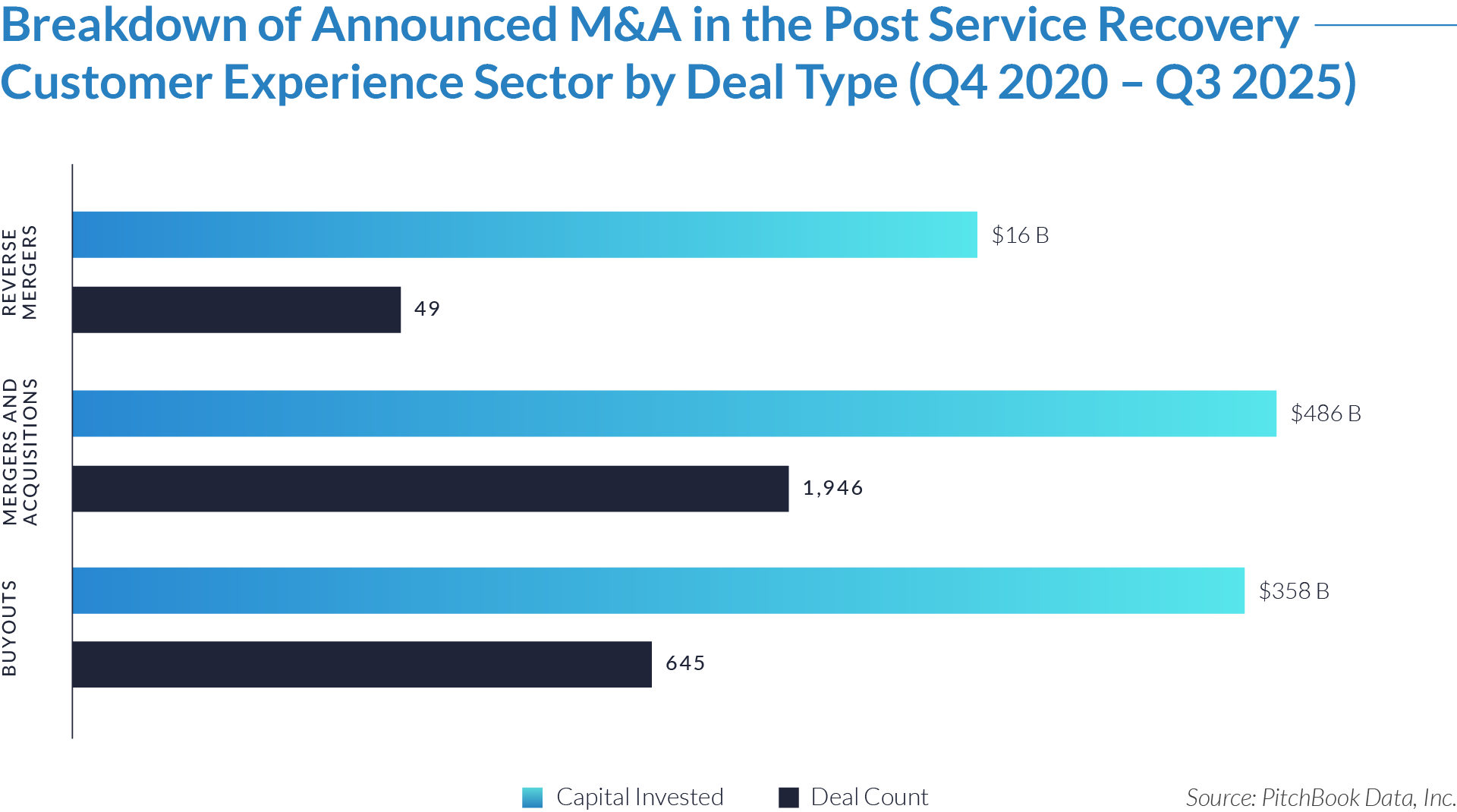

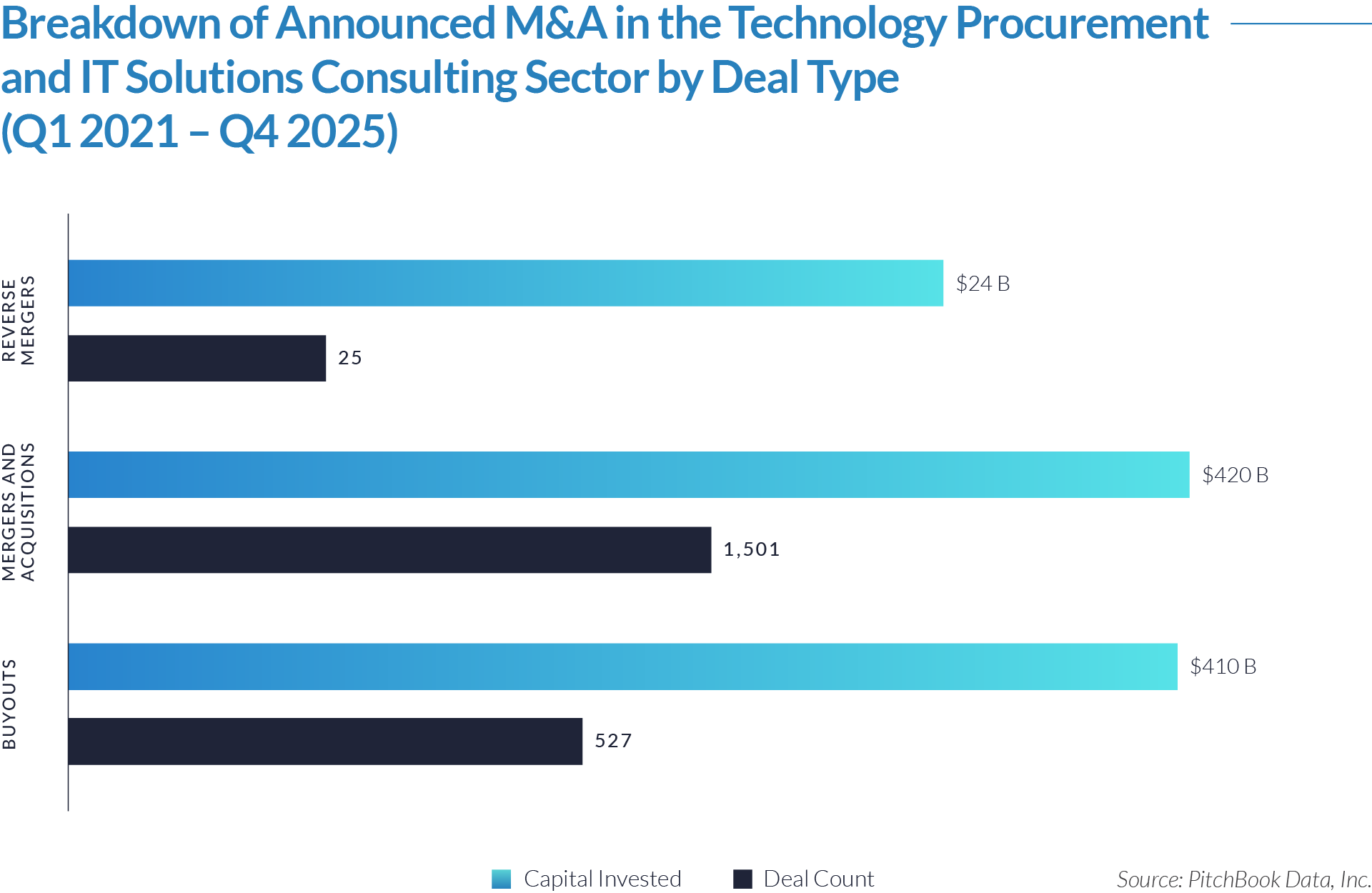

- Mergers and acquisitions accounted for 1,501 transactions, representing the majority of deal activity and deploying approximately $420 billion of capital. The scale of strategic participation reflects sustained consolidation across technology procurement and IT solutions consulting platforms, with acquirers prioritizing capability expansion, service breadth, and deeper integration within enterprise technology sourcing and vendor management workflows.

- Buyouts totaled 527 transactions but accounted for approximately $410 billion of invested capital, nearly matching total strategic M&A capital despite significantly fewer deals. This imbalance highlights substantially larger average transaction sizes and reflects private equity’s focus on scaled, recurring-revenue advisory and brokerage platforms with strong cash flow visibility and expansion potential.

- Reverse mergers comprised just 25 transactions yet deployed approximately $24 billion of capital. Although limited in frequency, these transactions indicate periodic use of public market entry strategies, likely concentrated during periods of favorable equity market conditions or when traditional IPO pathways were less accessible.

M&A Transactions Case Studies

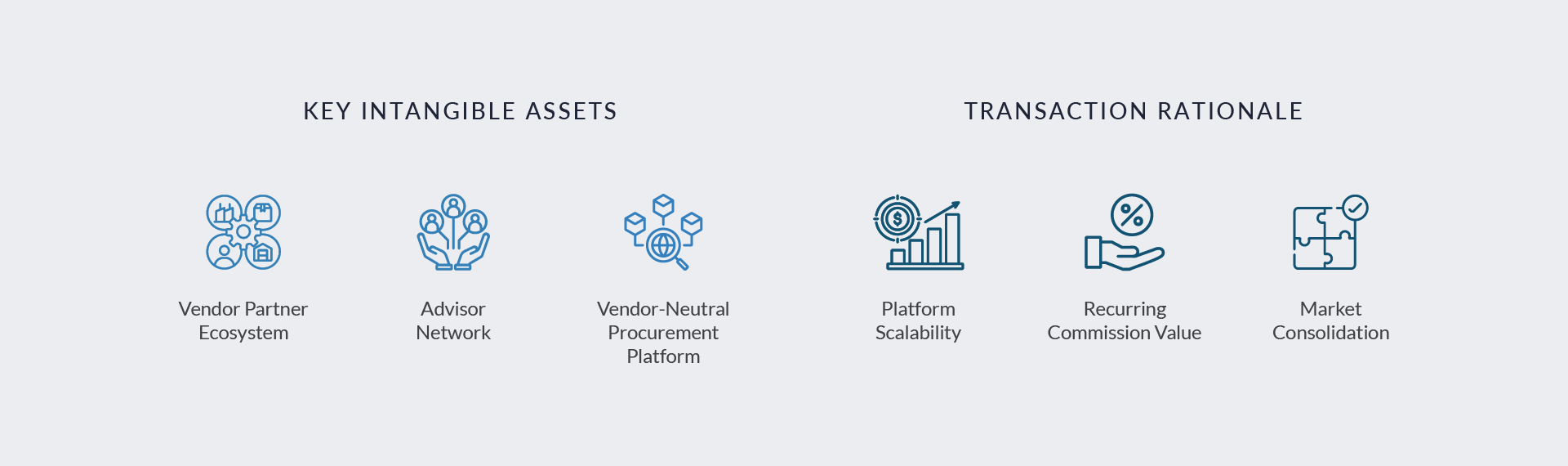

Three transactions in the technology procurement and IT solutions consulting sector highlight growing private equity and strategic interest in vendor-neutral advisory and brokerage platforms embedded in enterprise IT purchasing decisions. Acquirers are targeting asset-light, commission-based models that connect businesses with telecom, cloud, cybersecurity, and infrastructure providers through scalable advisor networks. These platforms generate recurring revenue, benefit from diversified vendor relationships, and demonstrate strong customer retention, positioning them as durable, cash flow–generative infrastructure within the evolving technology services ecosystem.

Case Study 01

AVANT COMMUNICATIONS

Avant Communications is a US-based technology procurement and advisory firm that provides vendor-neutral sourcing, brokerage, and consulting services across telecom, cloud, cybersecurity, and IT infrastructure solutions. The company helps enterprises evaluate technology vendors, negotiate contracts, and optimize IT spending through a combination of strategic advisory and commission-based brokerage services. Avant operates as an intermediary between businesses and technology service providers, leveraging a broad partner ecosystem to deliver customized connectivity, cloud, unified communications, and cybersecurity solutions. Its revenue model is primarily driven by recurring vendor commissions, supplemented by advisory services, enabling scalable growth and durable customer relationships.

Acquirer

Pamlico Capital is a Charlotte-based private equity firm specializing in growth-oriented investments in business services, technology-enabled services, communications, and information services companies. Court Square is a New York-based private equity firm focused on middle-market investments across business services, healthcare, and technology sectors. Both firms have extensive experience scaling platform investments through operational enhancements, strategic acquisitions, and disciplined capital deployment.

Transaction Structure

Avant Communications was acquired through a leveraged buyout transaction completed on December 17, 2025, in which Pamlico Capital partnered with Court Square to recapitalize the business at an enterprise value of approximately $252 million.

Market and Customer Segments Combination

The transaction combined Pamlico Capital and Court Square’s experience investing in scalable business services and technology advisory platforms with Avant’s established vendor-neutral technology brokerage model serving enterprise and mid-market customers. Under sponsor ownership, Avant continued to support organizations seeking optimized technology procurement strategies across telecom, cloud, and cybersecurity markets. The partnership provided additional financial resources and strategic support to expand Avant’s advisor network, strengthen vendor relationships, enhance operational infrastructure, and pursue potential add-on acquisitions to broaden geographic reach and service capabilities.

Acquisition Strategic Rationale

The acquisition reflected sustained private equity interest in technology procurement and advisory platforms that generate recurring commission-based revenue and operate scalable distribution models. Avant’s position as a vendor-neutral intermediary with an established partner ecosystem and diversified customer base provided visibility into recurring cash flows and attractive margin characteristics. The transaction aligned with Pamlico Capital and Court Square’s strategy of investing in asset-light, technology-enabled services platforms with opportunities for organic growth, advisor network expansion, and consolidation within the fragmented technology brokerage market.

Case Study 02

INTELISYS

Intelisys is a US-based technology services distributor and vendor-neutral brokerage platform specializing in telecom, cloud, unified communications, and connectivity solutions. The company operates through a nationwide network of independent sales partners and technology advisors who assist enterprise and mid-market customers in sourcing, negotiating, and procuring IT and communications services. Intelisys generates revenue primarily through recurring vendor commissions and partner-driven distribution relationships, positioning the company as a scalable intermediary within the telecom and cloud services ecosystem.

Acquirer

ScanSource, Inc. is a publicly traded technology distributor headquartered in Greenville, South Carolina. Historically focused on hardware, point-of-sale, barcode, and communications equipment distribution, ScanSource serves value-added resellers and channel partners across North America and internationally. The company has pursued strategic initiatives to diversify its revenue mix toward higher-margin, recurring services-based revenue streams.

Transaction Structure

Intelisys was acquired by ScanSource on August 29, 2016 for approximately $230 million, consisting of approximately $84 million paid in cash at closing and contingent earn-out payments of up to $150 million based on performance over four years following closing.

Market and Customer Segments Combination

The transaction combined ScanSource’s established distribution infrastructure and reseller channel relationships with Intelisys’ vendor-neutral telecom and cloud brokerage platform. By integrating Intelisys’ advisor ecosystem, ScanSource expanded into high-growth telecom and cloud services markets while diversifying beyond traditional hardware distribution. The acquisition enabled ScanSource to offer channel partners a broader suite of services solutions, strengthening its value proposition to resellers seeking recurring revenue opportunities and deeper customer engagement across communications and IT procurement.

Acquisition Strategic Rationale

The acquisition reflected ScanSource’s strategy to diversify its portfolio into higher-margin, recurring services revenue streams within telecom and cloud markets. Intelisys’ advisor-led, commission-based brokerage model provided immediate scale and access to a rapidly growing services distribution channel. The transaction allowed ScanSource to expand its presence within the telecom and cloud ecosystem, enhance cross-selling opportunities across its reseller network, and increase exposure to recurring commission revenue generated by long-term service contracts. The earn-out structure further aligned performance incentives and supported sustained growth following integration.

Case Study 03

MICROCORP

MicroCorp was a US-based technology services distributor and master agent specializing in telecom, cloud, data center, security, and managed services solutions. The company operated through a nationwide network of channel partners and independent technology advisors who assisted enterprise and mid-market customers in sourcing, negotiating, and procuring connectivity and cloud-based IT services. MicroCorp generated revenue primarily through recurring vendor commissions and partner-driven distribution relationships, positioning the company as a scalable intermediary within the telecom and cloud services ecosystem.

Acquirer

AppSmart, a division of AppDirect, is a technology services marketplace platform that enables businesses to evaluate, purchase, and manage cloud, telecom, and IT solutions through a centralized advisory-driven model. AppDirect is a privately held subscription commerce platform headquartered in San Francisco, California, focused on the digital distribution of technology services and recurring revenue business models. The company has pursued strategic initiatives to expand its advisor ecosystem and strengthen its presence within the technology services distribution channel.

Transaction Structure

MicroCorp was acquired by AppSmart on December 7, 2020, in a strategic merger and acquisition transaction. Financial terms of the transaction were not publicly disclosed.

Market and Customer Segments Combination

The transaction combined AppSmart’s marketplace-driven technology distribution platform with MicroCorp’s established national master agent network and vendor relationships. By integrating MicroCorp’s channel partner ecosystem, AppSmart expanded its footprint across telecom, cloud, and managed services markets while strengthening its advisor-led distribution capabilities. The acquisition enhanced AppSmart’s ability to provide end-to-end sourcing support and diversified technology procurement options to enterprise and mid-market customers seeking vendor-neutral advisory solutions.

Acquisition Strategic Rationale

The acquisition reflected AppSmart’s strategy to scale its technology services distribution platform through consolidation of independent master agents. MicroCorp’s commission-based brokerage model provided immediate expansion of advisor relationships and vendor partnerships within high-growth telecom and cloud services markets. The transaction enabled AppSmart to broaden its service portfolio, increase exposure to recurring commission revenue, and strengthen its competitive positioning within the fragmented technology procurement advisory ecosystem. By integrating MicroCorp’s network, AppSmart expanded its national distribution scale and accelerated its long-term growth strategy in recurring technology services.

As enterprise IT environments grow increasingly complex and multi-vendor ecosystems become the norm, technology procurement and IT solutions consulting platforms have evolved from transactional sourcing intermediaries into strategic infrastructure partners embedded within enterprise technology decision-making. Sustained transaction activity over the past five years reflects strong investor conviction that advisory-led, commission-based distribution models with recurring revenue characteristics represent a durable, cash flow–generating asset class rather than a cyclical services segment.

Looking ahead, acquirers are expected to remain focused on scalable platforms that combine vendor neutrality, deep advisor networks, recurring commission and services-based revenue streams, and expanding managed services capabilities. Valuation dispersion is likely to persist, with premium outcomes concentrated among platforms demonstrating network effects, strong revenue visibility, and technology-enabled differentiation. Alongside these scaled platforms, a long tail of smaller, advisory-led procurement and IT consulting firms is expected to remain an important component of the sector, supporting continued fragmentation and localized consolidation opportunities. At the same time, ongoing consolidation among fragmented regional operators is expected to drive continued roll-up strategies and national scale-building across the technology procurement and advisory landscape.

Source: Globenewswire, ScanSource, SEC GOV, Businesswire, Pitchbook Data.