Global Vertical Farming Market

Global Vertical Farming Market

Vertical farming is an agricultural method to grow crops in vertically stacked layers. It incorporates controlled environment agriculture using soilless farming techniques, which provides better food quality with higher crop yields.

The COVID-19 pandemic and global geopolitical factors have impacted the food and agriculture sector, from supply chain disruption to shortage of food supplies. This has led many to adopt vertical farming technologies, to improve food security and increase farming capacity in urban and local environments. These major factors are contributing to the growth of this market, with a remarkable interest among investors to invest in vertical farms.

Overview of the Vertical Farming Industry

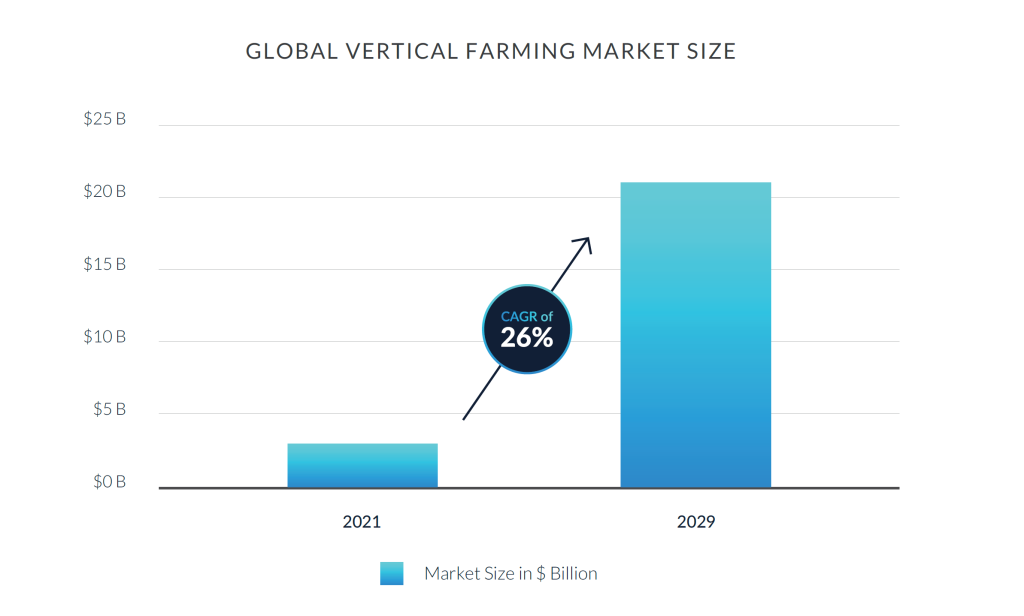

The global vertical farming industry is expected to grow from $3 billion in 2021 to $4 billion in 2022. Further, the market is forecast to grow at a compound annual growth rate (CAGR) of 26% to $21 billion by 2029. With the increase in population and the rise in demand for healthy and safe food, farmers are tending to use new methods and technologies in the agriculture industry, known as vertical farming. This report outlines announced investments made globally in vertical farm deals between 2017 and 2022.

Key Subsectors of the Vertical Farming Industry

Key Subsectors of the Vertical Farming Industry

1 – The Methodologies Of Vertical Farming

Vertical farming methodologies can be divided into hydroponics, aeroponics, and aquaponics based on the use of soil and water in the agricultural process. Farmers can have total control over a hydroponic system by using water more efficiently and improving the quality and taste of the produce. These and many other reasons are driving hydroponics to grow as a vertical farming methodology. Aeroponics leverages air to grow crops. Aquaponics is a method of growing plants and raising fish in water. Fish will feed the plants with their waste that converts into nitrates, and the plants will clean and filter the water before it returns to the fish tank.

2 – Structure Analysis

New and abandoned buildings are being used to deploy and develop vertical farms. Building-based vertical farms are growing across cities. For example, the NYC farming company Bowery Farming developed urban farms inside abandoned warehouses that provide fresh produce to local retailers and restaurants. The shipping container-based structure of vertical farming is projected to gain traction and growth in the coming years. These structures are used for developing indoor farms by controlling and monitoring all systems remotely from a computer or smartphone.

3 – Component Analysis

Various manufacturing components are used within vertical farming processes. LED lighting is becoming ideal for farms for its low operational cost and power consumption. This component, along with climate control, sensors, irrigations, and fertigation components, are driving the segment to grow rapidly and steadily.

Global Capital Market Activity Overview

- Between 2017 and 2022, $14 billion was deployed across a total of 1,520 vertical farming deals in the analyzed period with an average deal size of $9 million during this period.

- More than $660 million was deployed into 221 deals within the vertical farm sector in 2017, with an average deal size of $3 million.

- The COVID-19 pandemic boosted investments in the vertical farms market between 2020 and 2021. The most active year for vertical farming has been 2021, with $6 billion deployed across a total of 332 deal counts and an average deal size of $17 million.

Announced Vertical Farming Deal Counts

- Approximately 72% of deal counts were attributed to small deal sizes up to $5 million. This indicates the availability of a remarkable number of different start-ups and innovative technologies.

- The deal sizes ranging from $5 million to $25 million own 18% of the total deal count. Compared to small deal sizes, these growth-stage companies indicate that there are many start-ups doing well in the market and gaining traction.

- The lowest share of deal count goes to over $25 million deal sizes. This shows that the market is still fragmented with relatively few mature players.

- The USA is leading the majority of deal counts in the vertical farming market with a 48% share of the global deal counts. This indicates the high presence of many vertical farms across the USA and the adoption of new technologies. The legalization of cannabis in the USA has also helped in the growth of the vertical farming market.

- Europe holds second place for the highest deal count with 29% of the global count. This region is projected to drive the development of vertical farms in the upcoming years.

- The Asia Pacific region, with 17% of the deal count, will continue to grow due to the scarcity of water and increased food demand for the vast population like in China and India. Climate change and the financial challenges that the farmers in this region face will drive the need for the adoption of vertical farming techniques.

- The Middle East and Africa showcase the lowest count of deals with 6%. This region is expected to have remarkable growth in the future due to the rise of water scarcity and the growing research and development activities by market players to boost the development of advanced farming techniques.

With the increase in population and the shift in the global food market to healthier and safer products, farmers are adopting new technologies and farming methods. In contrast to the traditional agriculture methods, these new methods known as vertical farming are a game-changer for the agriculture technology industry. The rise of this global trend is leading to a continuous spike in interest among investors like venture capitalist firms to invest in vertical farms and drive the markets’ growth in the upcoming years.

Sources: Pitchbook Data.