How to Perform a Disciplined Sell-Side M&A Process to Maximize Results

How to Perform a Disciplined Sell-Side M&A Process to Maximize Results

The sell-side M&A process, facilitating the sale of a business, is long and complex. Bringing a company to market does not guarantee the company will achieve its M&A goals. The M&A process is challenging for three reasons:

1. It is difficult to build consensus among a large number of stakeholders.

2. Gathering relevant, transparent, and adequate data is complicated, particularly in private markets.

3. The M&A process contains many steps, and within each step, there are many opportunities for things to go wrong.

This report contains the step-by-step guide Jahani and Associates (J&A)—an NYC-based professional services and advisory firm—uses to maximize results for its clients. Each step in the sell-side M&A process is driven by activities, deliverables, and solutions.

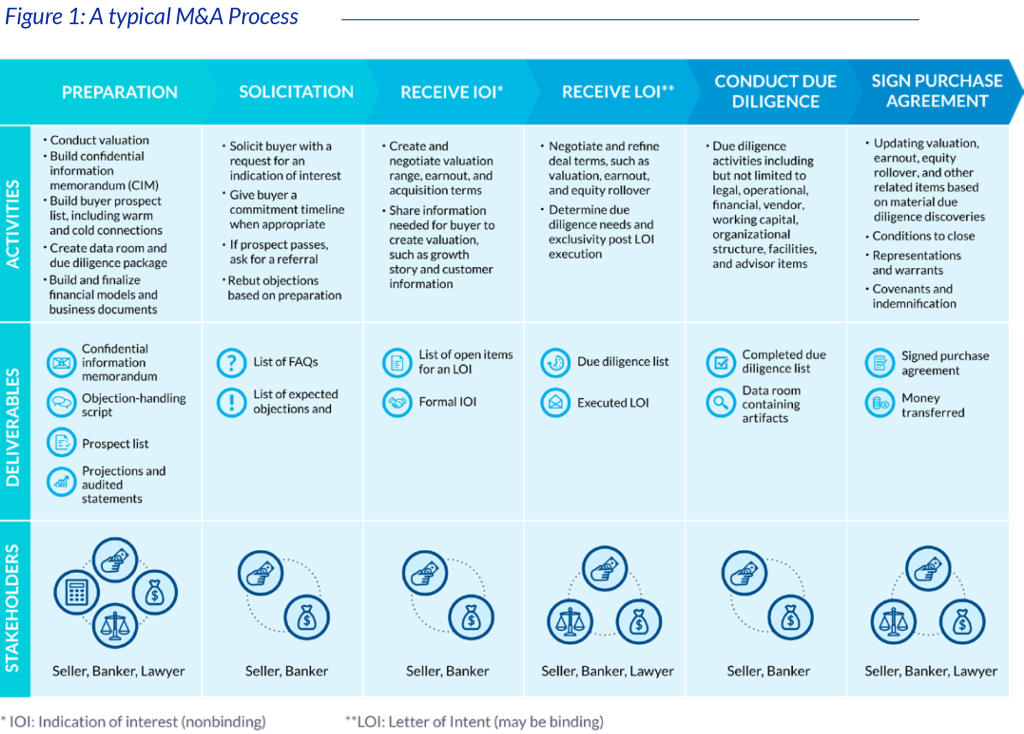

STEP 1: Preparation to Solicitation

Preparation for solicitation requires the company and their investment banker to generate the artifacts buyers need to make an offer for the company. This information includes but is not limited to financial information, the growth history of the company, intangible asset information (e.g., customer relationships and proprietary technology), and the reasons the owners are selling the business.

Industry-standard deliverables, such as a confidential information memorandum (CIM) and audited financial statements, are used in this phase to market the business to potential buyers. This phase is vital because any delays while in market can impact the outcome of a transaction.

STEP 2: Solicitation to IOI

Reaching a sufficient number of solicitations to find an interested buyer is difficult and crucial, particularly in the lower-middle and middle markets. J&A recommends only sending detailed material during the preparation phase to potential buyers after they have signed an NDA. Common sources of buyer solicitations include direct connections from an investment banker’s network, direct solicitations of qualified buyers determined from research (e.g. PitchBook), and targeted emails to qualified lists of buyers.

IOIs (Indications of Interest) contain valuation ranges and general expectations of earn-out, which should be negotiated as necessary to have a smooth transition from an IOI to an executable letter of intent (LOI). IOIs are non-binding.

STEP 3: IOI to LOI

A site visit usually occurs while transitioning an IOI to an LOI and is an opportunity for the buyer and seller to meet and conduct a deep dive into any outstanding items that need to be settled before executing an LOI. Since LOIs are legally binding, many buyers will require exclusivity after an executed LOI, which is also referred to as a “no-shop clause.” This means the seller will not be able to conduct sale-related conversations during the no-shop period and must ensure the upcoming due diligence will be satisfactory, in order to close the deal.

STEP 4: LOI to Purchase Agreement, Including Due Diligence

Due diligence is the process of affirming the information the buyer has used to make his offer and determining whether or not the company is in good standing with all relevant information in its possession. It is often the longest part of the sell-side M&A process, as it may take up to 120 days.

Once due diligence is complete, executing the purchase agreement, where ownership changes hands, is the final step in the sell-side M&A process. Agreements can be asset purchases or stock purchases. If due diligence went as expected, which is vastly important, this step should be relatively simple. Changes that may affect purchase agreement negotiations are material discoveries in due diligence, economic forces, material alterations in business operations, and management changes.

Problems and Solutions: Quickly Resolving Challenges Requires

Deep Thinking and Preparation

Jahani and Associates has collected common challenges that exist in each step of the sell-side M&A process and the best way to resolve them. In order to avoid disruptions or delays in the M&A process, it is important for M&A stakeholders to plan ahead and know where weaknesses may rise, and also imperative that the investment banking team has a plan to resolve these challenges before they even arise.

Preparation to Solicitation

Companies most often do not go from preparation to solicitation when seller management teams are not aligned or properly prepped for the sell-side M&A process. This can occur when multiple stakeholders are involved, particularly in companies boasting a significant capital raise. If a business undergoes a change that materially reduces the company’s desired valuation, management often decides to postpone the process.

Solicitation to IOI

As a solicitation to IOI is fundamentally a sales process, sellers, and their teams are most prepared when they view this as a sales exercise. This is often the most difficult step in the process for unprofitable companies in the lower-middle market.

IOI to LOI

Moving from an IOI to LOI is a matter of negotiation and mutual understanding between the buyer and seller. A site visit is often used between the IOI and LOI to develop a relationship between the buyers and sellers.

LOI to Purchase Agreement, Including Due Diligence

Due diligence is the process of confirming the buyer’s understanding of the business at the time they made their offer. Due diligence is time-consuming and material information that changes the valuation, and earn-out identified in the LOI may be discovered during due diligence. This will be negotiated as part of the purchase agreement, which may be made for either cash or stock, each of which has its own tax, legal, and strategic considerations.

The sell-side M&A process is challenging, but the seller’s success will be maximized when a disciplined process is followed.

The challenges, solutions, and KPIs in this paper are not exhaustive, but they provide an overview of the way to maximize success in sell-side M&As. It is important that all stakeholders understand the challenges they will face and how to alleviate them as quickly as possible. Establishing a consensus among stakeholders and then focusing on a problem-solution-KPI framework gives transparency to the client and allows the investment banker to increase the size of their team while preserving client service and information sharing. Experience in dealing with these issues is paramount to successfully delivering M&A results, and that experience must be coupled with actionable outcomes.

Any business owner seeking to sell their business must carefully consider all these factors and be aware of expected obstacles in order to significantly increase the likelihood that their company successfully completes a sell-side M&A transaction. The analysis contained herein is based on decades of experience and is included to support business owners across the world as they achieve a maximally successful exit.

In 2019, J&A surveyed hundreds of business owners about successful and failed M&A deals, why they failed, and how those failures could have been avoided. J&A then compared these stories with its own processes and tools to determine the best way to anticipate and avoid these failures in any M&A scenario. The resulting analysis is this document that outlines common reasons for failure and how to avoid them. This document is meant to serve as a resource to business owners and other service providers to give the best strategic advice and service for their business or clients.

Sources:

1. Baird, Les, David Harding, Peter Horsley, and Shikha Dhar. “Using M&A to Ride the Tide of Disruption.” Bain & Company, January 23, 2019.

2. Buesser, Gary. “For the Investor: Internally Generated Intangible Assets.” Accessed November 22, 2019.

3. Corporate Finance Institute. “What is the No Shop Provision?” No-Shop Provision. Accessed November 22, 2019.

4. Deloitte. “Cultural issues in mergers and acquisitions.” Leading through transition: Perspectives on the people side of M&A. Last modified 2009.