B2B Subscription Company M&A Valuation Drivers

B2B Subscription Company M&A Valuation Drivers

Table of Contents

B2B Subscription Metrics and Industries

Mergers and acquisitions (M&A) in the B2B subscription space have distinct characteristics compared to other industries due to the need to demonstrate secure recurring revenue streams, minimize customer acquisition costs, expand contract-based customer bases, optimize operational efficiencies in subscription billing and retention, leverage predictable cash flows for financial structuring, and maximize long-term value for investors and shareholders. Acquirers focus on ensuring that all these factors align with their strategic goals as they directly impact long-term value creation. Investors and buyers in this space are primarily interested in capital appreciation and value growth rather than short-term liquidity. They prioritize scalable revenue streams, strong customer retention, and operational synergies that enhance enterprise value over time. The integration process post–M&A often involves precise management of technology, contracts, customer relationships, and other intangible assets.

This report explores the key valuation drivers in B2B subscription M&A deals by analyzing the specific ratios and KPIs that potential buyers prioritize and assess differently than other M&A deals.

B2B subscription companies generate income through recurring subscription fees, upselling, and value-added services. As such, the management of customer acquisition costs, subscription revenues, and retention efforts plays a critical role in shaping a company’s financial performance and overall valuation.

Important B2B Subscription Company Valuation Drivers

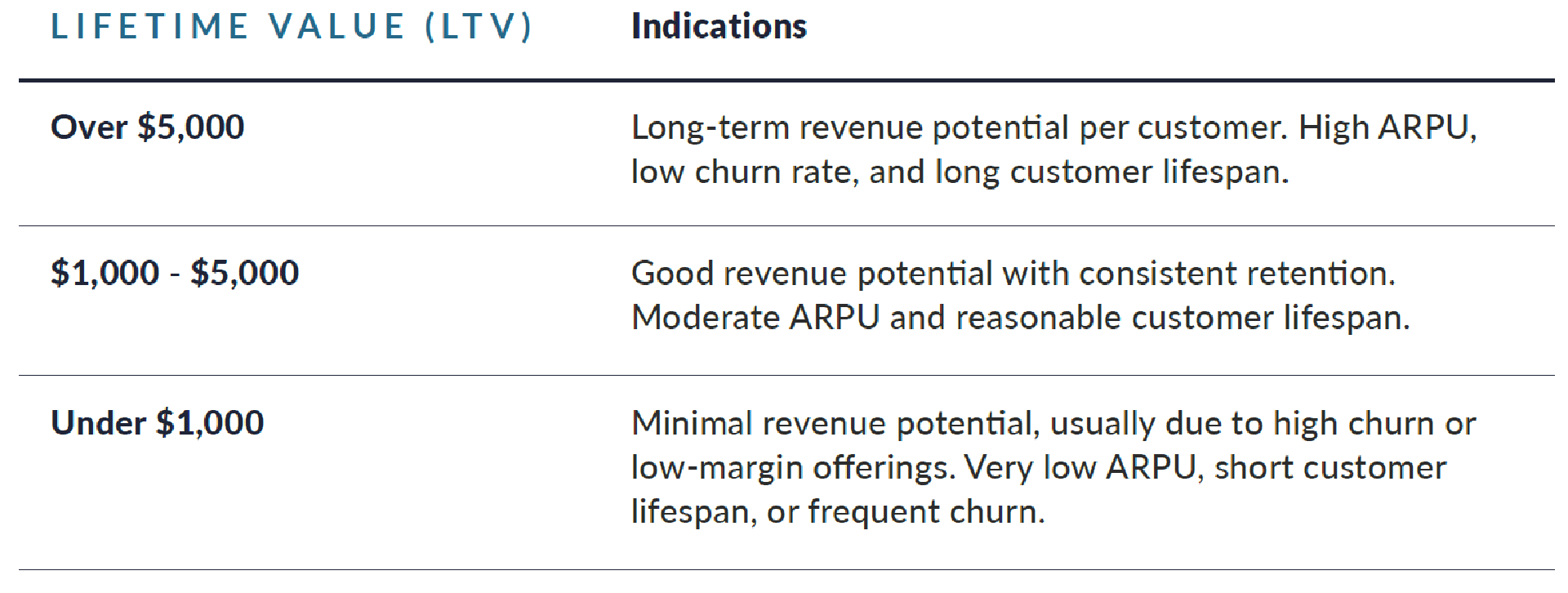

LTV (Lifetime Value)

Lifetime value (LTV) measures the total revenue a customer is expected to generate over the duration of their relationship with a business. It is especially important in the subscription model because it reflects long-term profitability and the sustainability of a business. Greater LTV commands a greater valuation in an upfront consideration. LTV also demands more weight to upfront and less weight to contingent payment consideration in an M&A transaction.

B2B subscription companies with high LTVs typically operate in industries where their solutions are deeply embedded into the customer’s operations. These companies may provide enterprise software solutions and excel at upselling and cross-selling, and hence are more valuable. B2B subscription companies with low LTVs face high churn rates, limited upsell opportunities, or low customer engagement, increasing risk and therefore commanding lower values. Startups and newer businesses may struggle with low LTVs, as they operate in highly competitive markets with commoditized offerings, making it easier for customers to switch providers.

HIGH LIFETIME VALUE

In M&A, LTV often correlates with well-established customer success practices and a high-quality product, reducing the risk of churn post-customer acquisition. Acquirers see high LTV as a sign of potential for future growth and a faster return on investment (ROI). Low LTV reduces a target company’s appeal, as it requires additional investment post-acquisition to address the underlying causes, such as revamping customer success, refining pricing strategies, altering target customers, or enhancing product offerings. These risks can lead to lower valuations or deal structures that lean more toward earnouts or performance-based incentives to mitigate uncertainties. However, these structures increase seller risks by tying a portion of the sale price to future performance, which may be influenced by changes the acquirer makes post-acquisition, leading to uncertainty, loss of control, and the potential for reduced financial returns if key metrics are not met.

Example

Adobe’s transition from selling perpetual licenses to a subscription model in 2013 increased its recurring revenue and lifetime value. Adobe’s Creative Cloud offers a suite of tools that are constantly updated, with different plans available for individuals, businesses, and students, which make it accessible to various customer segments. This ensures that customers always have access to the latest features without the need for costly upgrades.

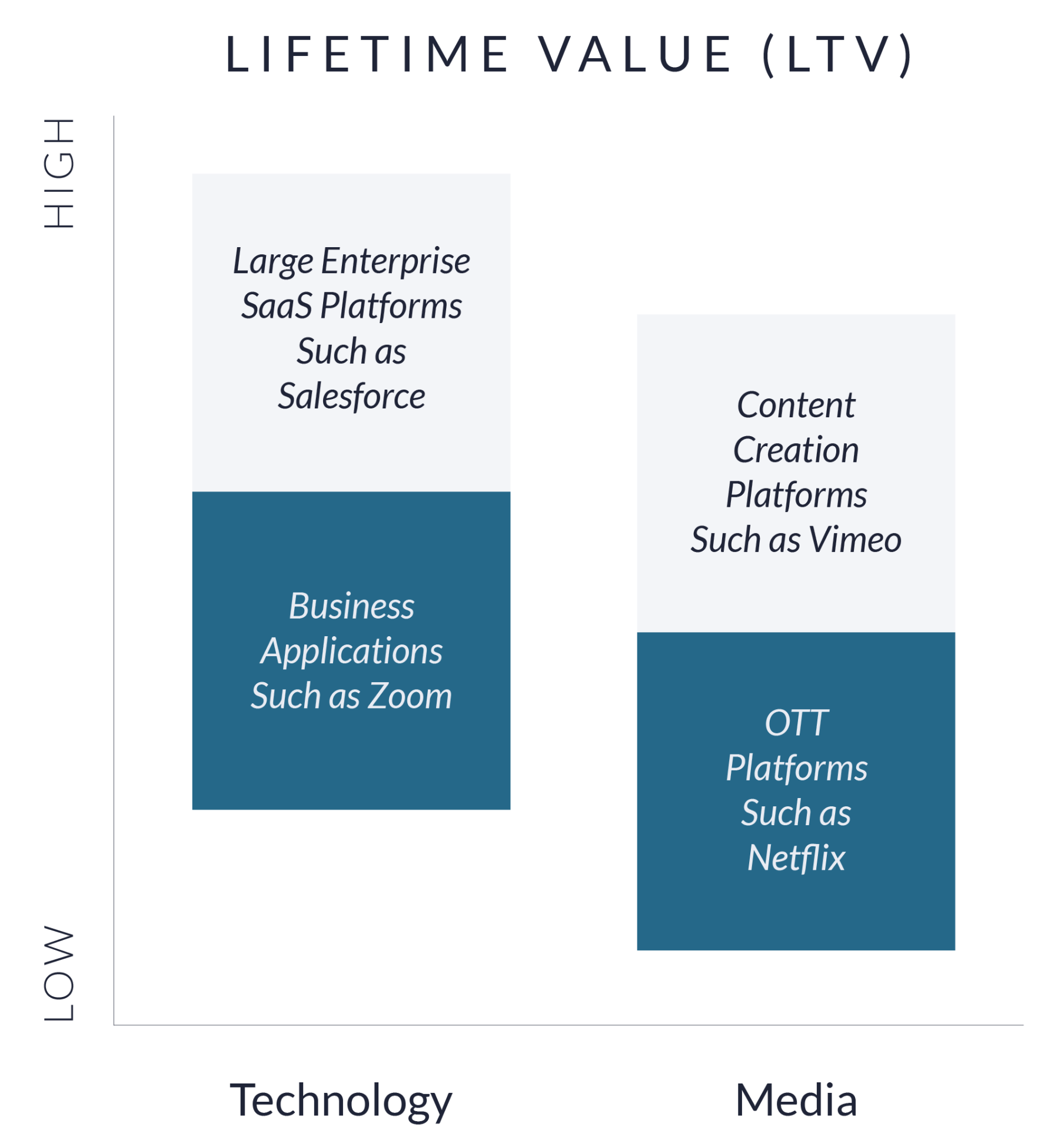

High customer retention and enterprise-focused contracts yield high LTV. Also, industries with high switching costs such as enterprise SaaS naturally score higher.

Media platforms like Vimeo and Netflix often face price-sensitive customers, potentially limiting LTV.

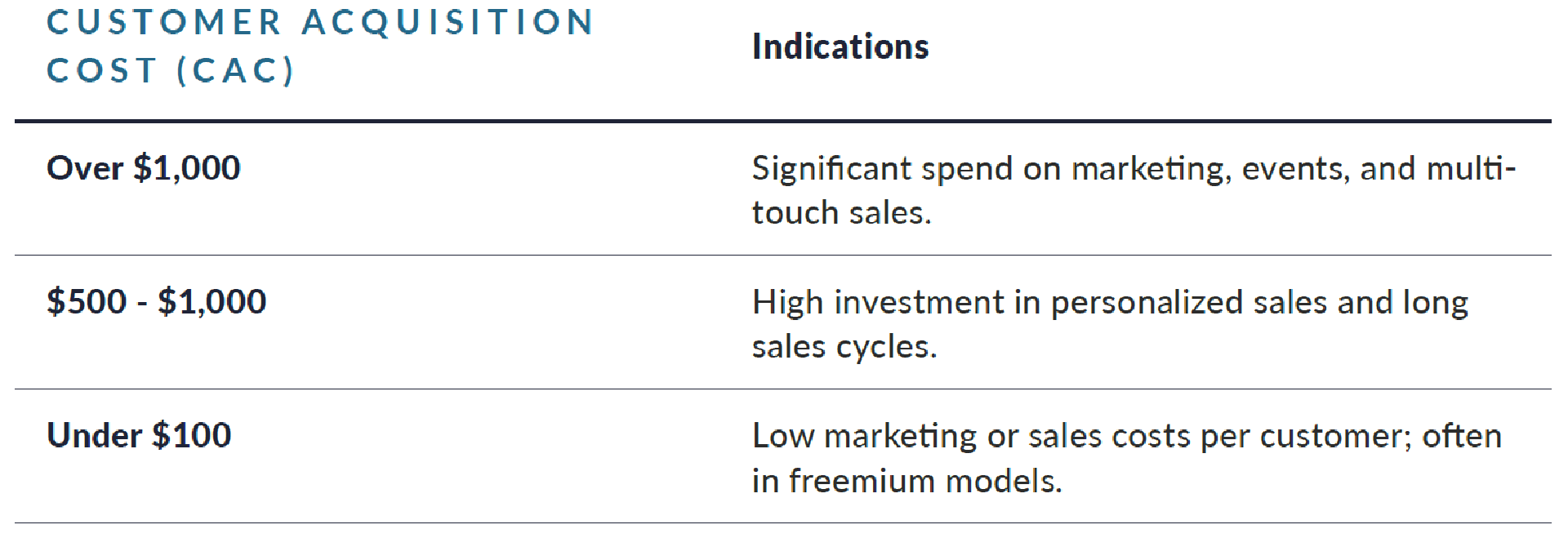

Customer Acquisition Cost (CAC)

CAC indicates the total cost of acquiring a customer, including marketing, advertising, and sales team expenses.

The key components of CAC for B2B subscription companies include marketing costs, sales costs, and other acquisition costs. Marketing costs encompass expenses for digital ads, content marketing, search engine optimization (SEO) efforts, events, trade shows, and both inbound and outbound lead generation tactics. Sales costs cover salaries, commissions, CRM tools, and other resources related to sales personnel and processes. Additionally, other acquisition costs may involve tools, software, or third-party agencies used for lead generation, prospecting, or analytics. CAC can greatly impact valuation and M&A payment consideration, especially in transactions where sellers have high but inconsistent acquisition costs, making future growth less predictable.

HIGH CUSTOMER ACQUISITION COST (CAC)

A high CAC suggests that the company takes longer to recoup its customer acquisition costs, which can strain cash flow and limit the ability to reinvest in scaling the business. Extended sales cycles result in multiple touchpoints and months required to close deals, thereby increasing costs and dependence on sales teams to further increase CAC, as their involvement directly influences acquisition efficiency. Additionally, if retention rates are low and churn is high, the extended payback period worsens the financial burden, delaying profitability. The varying effectiveness of marketing channels also impacts CAC, as some channels may underperform, requiring continuous optimization to maintain cost efficiency in customer acquisition.

A low CAC indicates that a company can recoup its customer acquisition costs quickly, leading to faster payback periods and healthier cash flow. This efficiency can be attributed to factors like optimized marketing channels, strong brand recognition, lower sales cycle durations, or the effective use of marketing strategies.

Example

HubSpot, a leading provider of inbound marketing, sales, and customer service software, has successfully built a low customer acquisition cost (CAC) through a combination of content marketing, SEO, and free resources. Its inbound marketing strategy focuses on attracting leads via valuable content such as blogs, e-books, webinars, and courses, which reduces reliance on paid advertising or large outbound sales teams. Several factors contribute to HubSpot’s low CAC, including its strong brand presence, which positions the company as an industry thought leader, making it easier to attract organic leads. HubSpot also offers a range of free tools (like CRM and marketing automation) that help capture leads and build trust with potential customers before converting them to paid plans. This self-service model allows many customers to sign up, implement, and use the platform with minimal direct sales interaction, further reducing the need for a large sales team. For instance Shore, a company that adopted HubSpot’s inbound methodology, achieved a 12x increase in leads and reduced customer acquisition costs by 35%. The integration of HubSpot’s free tools and self-service model meant that Shore could scale its lead generation efforts without the need for a large, costly sales team. As a result, Shore was able to achieve a significant increase in the volume of leads while simultaneously lowering its CAC, thus improving overall marketing efficiency and profitability.

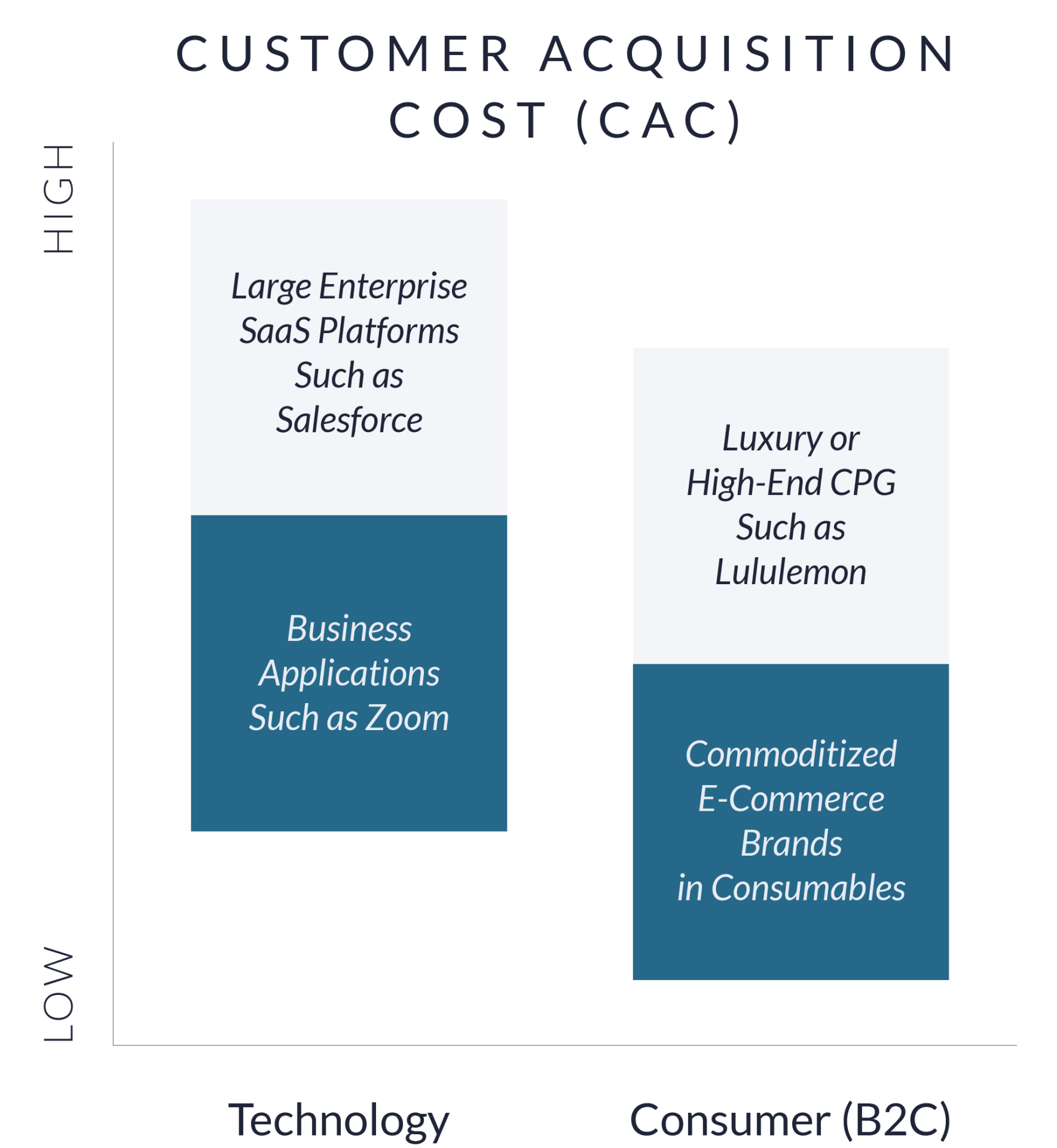

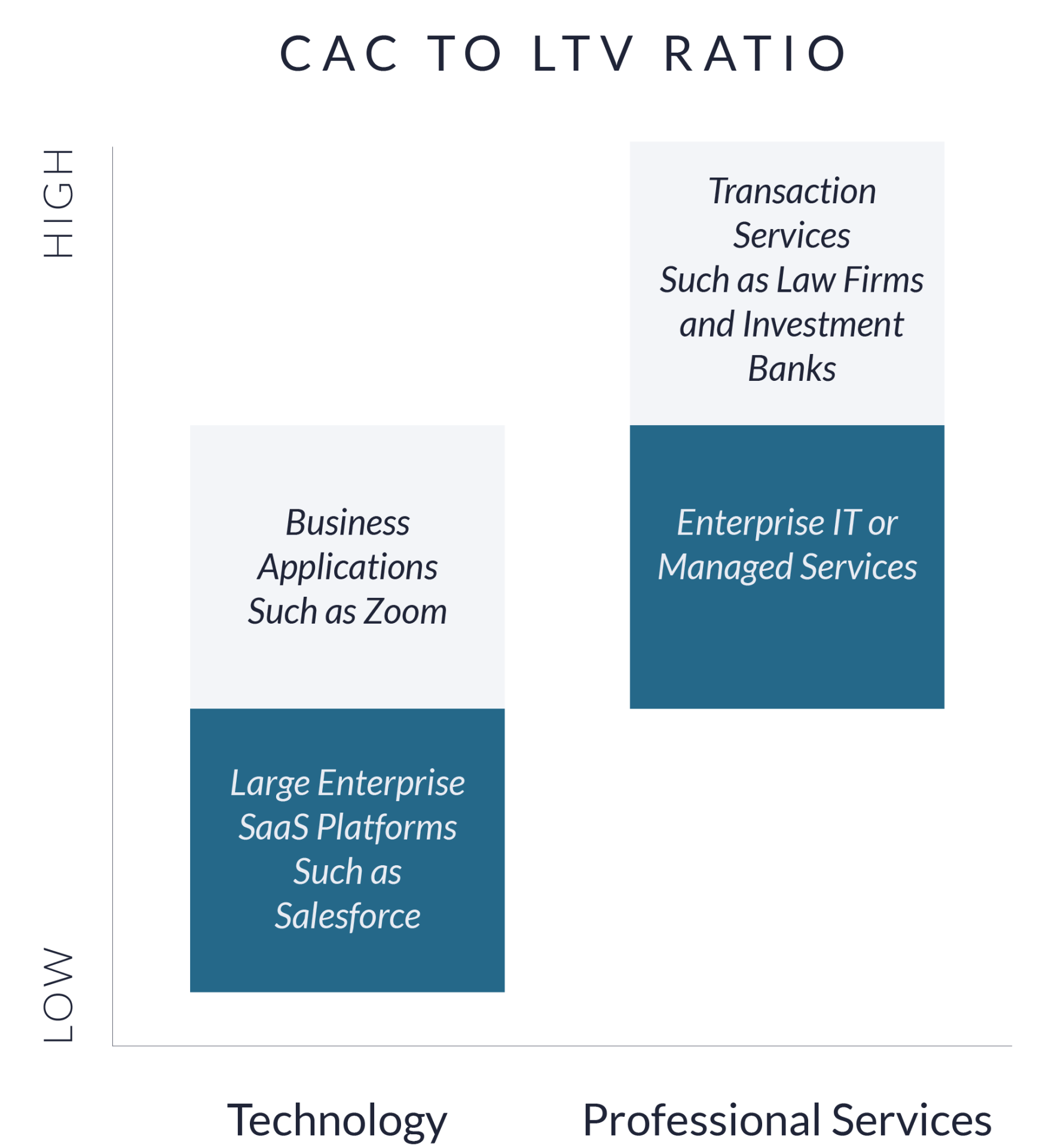

Sectors requiring long sales cycles, relationship-building, or high levels of customer education tend to have higher CACs (enterprise SaaS). Salesforce spends heavily on enterprise sales, marketing, and customer onboarding, justifying a high CAC, while Zoom has a lower CAC due to its freemium model, viral adoption, and word-of-mouth marketing. Many users onboard themselves, which minimizes sales costs.

Consumer-facing sectors such as e-commerce generally exhibit lower CACs due to scale and simpler acquisition models, compared to enterprise sectors with bespoke sales.

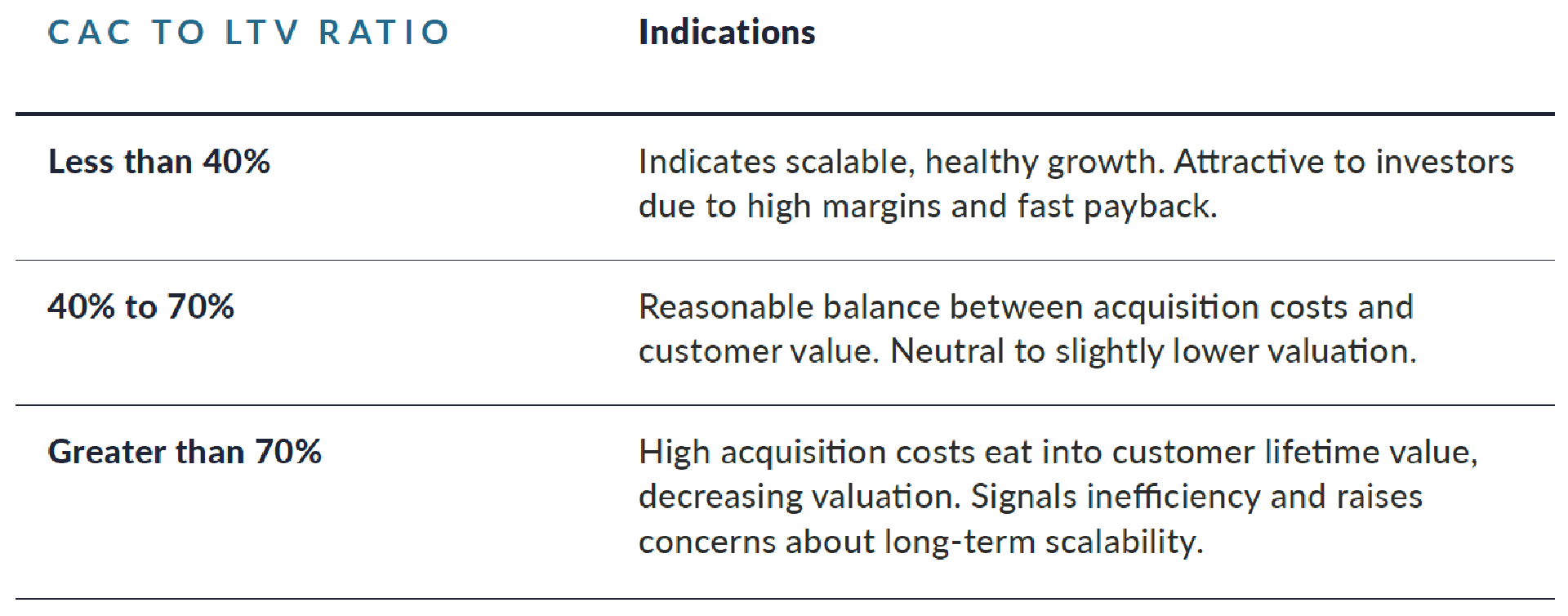

Customer Acquisition Cost to Lifetime Value (CAC to LTV)

The CAC to LTV ratio measures how much a company spends to acquire a customer relative to the total revenue that the customer is expected to generate over their lifetime.

LOW CAC TO LTV RATIO

For B2B subscription companies, a high CAC/LTV ratio suggests that the company is spending material amounts to acquire each dollar of customer value, which signals inefficiency and lower profitability. In contrast, companies with low CACs and high LTVs are particularly attractive because they demonstrate efficient growth and resilient revenue streams. Acquirers may offer higher upfront payment consideration for these companies as they are less risky and more likely to generate long-term returns.

Enterprise SaaS companies with complex sales cycles tend to have higher CACs, but this can be offset by strong LTVs, especially when customers are committed to long-term contracts or rely on a platform for operations. In contrast, companies in more competitive industries or those with lower switching costs may struggle to maintain a favorable CAC to LTV ratio. OTT platforms like Vimeo often face this challenge due to price-sensitive customers and high churn rates, leading to lower LTVs and therefore a less favorable ratio.

Example

Slack, prior to its acquisition by Salesforce, maintained a CAC to LTV ratio driven by a freemium model and low-touch sales. Slack’s product-led growth strategy minimized customer acquisition costs while maximizing lifetime value through enterprise expansion and user retention. This ratio contributed to its high valuation in the acquisition.

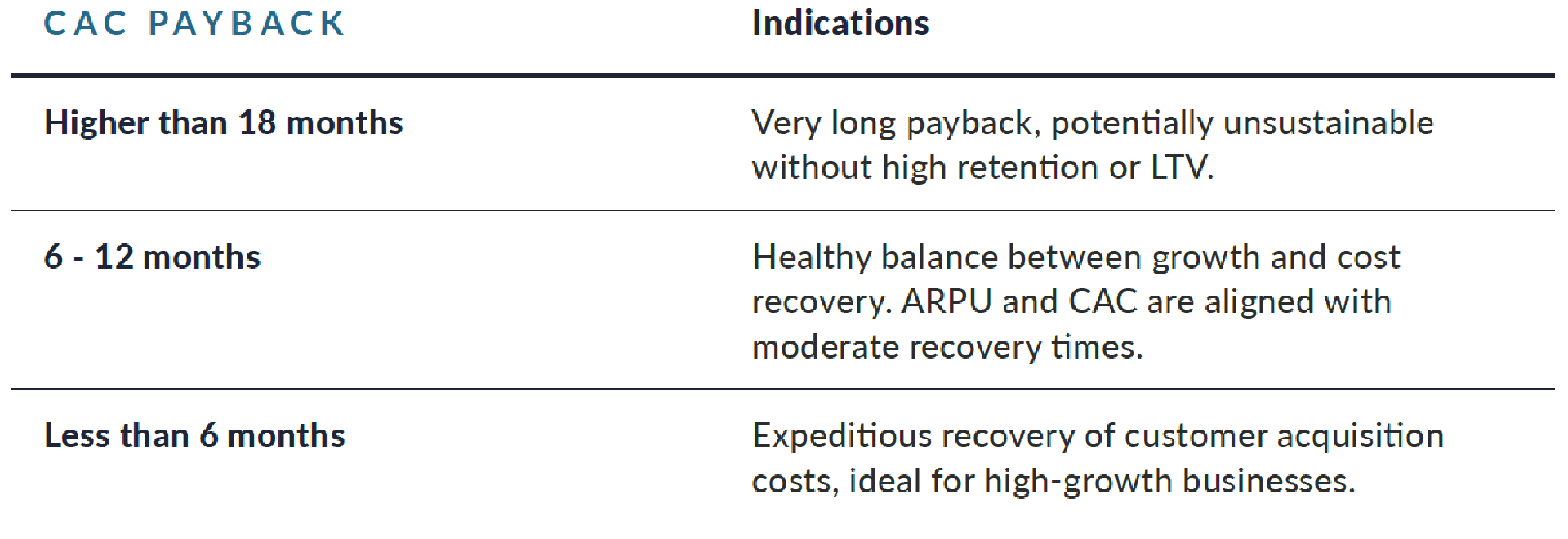

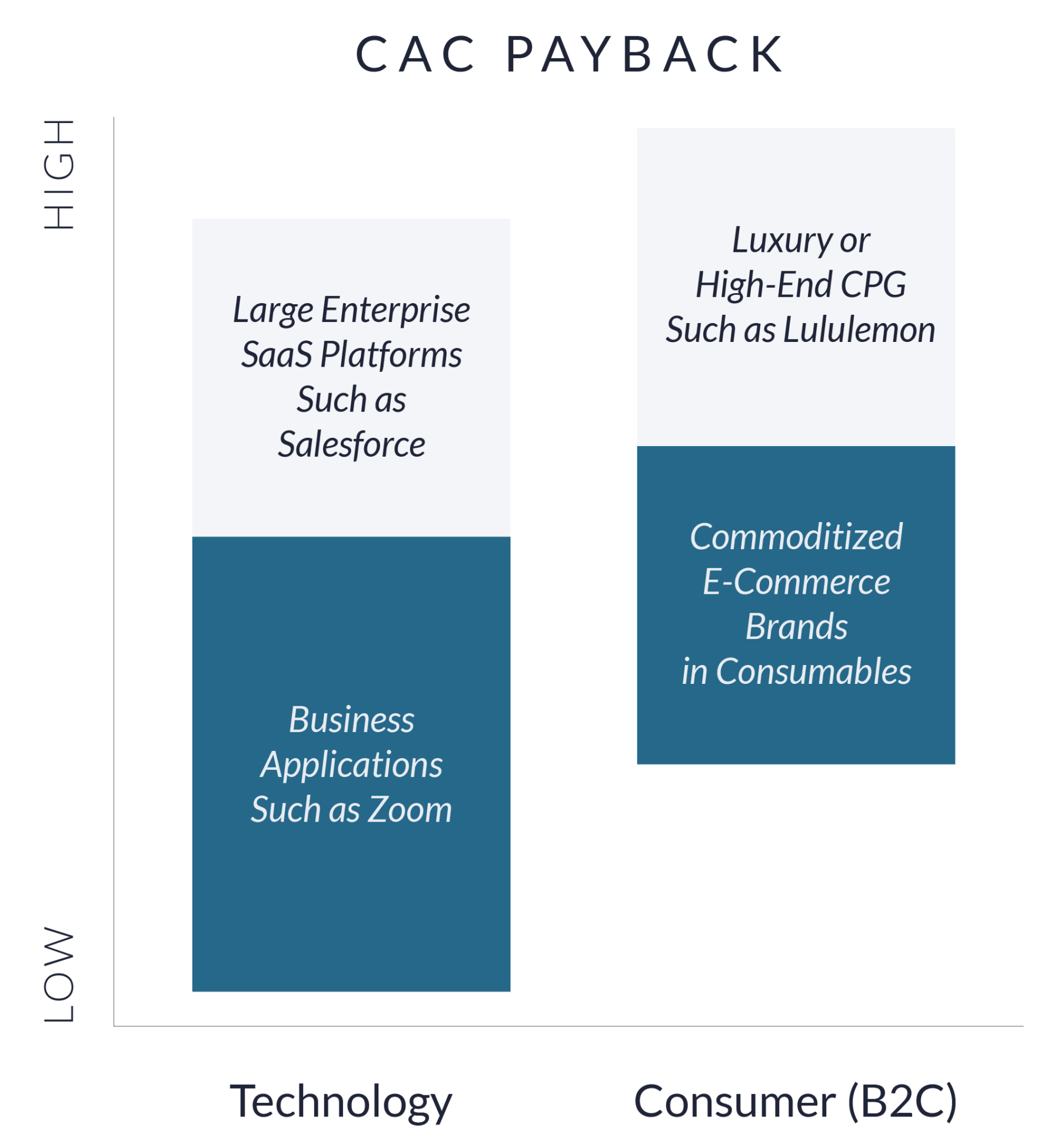

CAC Payback

CAC payback measures how long it takes to recoup the cost of acquiring a customer. This period is typically expressed in months and helps companies understand when they can start generating profit from a new customer after recouping the initial acquisition cost. A shorter CAC payback period directly improves EBITDA, influencing both the upfront payment consideration and overall valuation in M&A transactions.

A longer payback period means that a company takes more time to recoup the costs of acquiring customers, which can put pressure on cash flow, especially if the business is growing rapidly or dealing with high customer acquisition costs.

SHORT CAC PAYBACK PERIOD

Challenges in optimizing the CAC payback period include high customer acquisition costs, where expensive marketing channels or large sales teams can extend the payback period. Additionally, companies with lower pricing models or high-cost structures may struggle with longer payback periods, even if they have healthy customer acquisition costs. High churn further complicates this, as customers leaving before the business can recover their acquisition costs lengthens the payback period.

A shorter CAC payback period (under 12 months) indicates that the company can recoup its customer acquisition costs relatively quickly, making it easier to reinvest in acquiring new customers and scaling the business. It contributes to faster profitability by ensuring faster cash flow, enabling the company to reinvest in growth initiatives without significant financing needs.

Investors often review the CAC payback period to evaluate the financial health and scalability of a subscription business. Companies with short payback periods are often more attractive to investors because they are seen as more resilient and capable of sustaining growth without needing large amounts of capital.

Example

For Netflix, estimates suggest that the CAC payback period for new US-based subscribers is approximately 11 months. This means that it takes about 11 months for Netflix to recover the costs incurred in acquiring each new US-based subscriber.

In contrast, Amazon’s Prime program reportedly has a CAC payback period of around 2 years. This extended period reflects Amazon’s substantial upfront investments in customer acquisition, which are offset by significant long-term value from Prime members through increased loyalty and higher lifetime spending.

SaaS and subscription-based businesses recover CACs faster due to predictable, ongoing revenue streams. For example, Salesforce has a short CAC payback period because it uses its strong brand and inbound leads to drive scalable sales. Many customers are subject matter experts, with shorter onboarding and sales cycles. Recurring subscription revenue ensures consistent payback. Zoom also has short CAC payback because of the freemium model. Many customers start with free plans and upgrade to paid tiers with minimal sales efforts.

The CAC payback period tends to be higher for luxury and high-end CPG companies, especially those with premium price points and longer customer lifetimes, as their investments in brand-building and customer acquisition may take longer to recoup compared to mass-market brands.

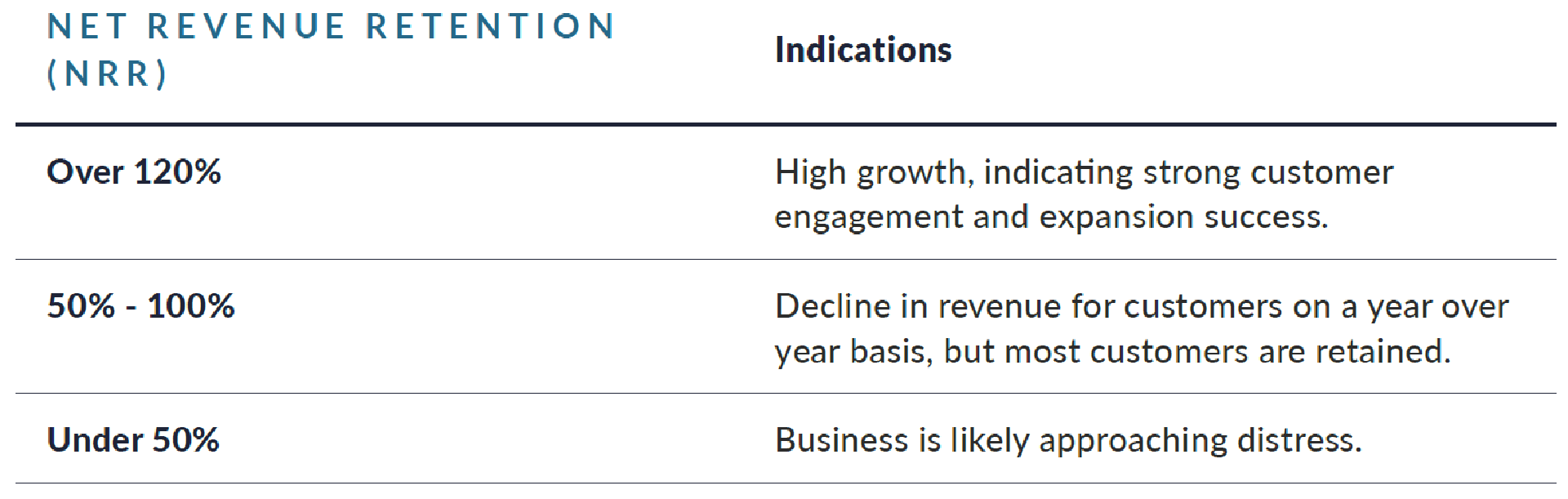

Net Revenue Retention (NRR)

Net revenue retention (NRR) measures a firm’s ability to retain and grow revenue from existing customers. NRR measures how much revenue a company retains over a given period, including upgrades, downgrades, and churn. A high NRR has a significant impact on valuation as well as the upfront payment consideration sellers receive at closing, as it indicates strong customer retention and expansion potential, reducing the risk for buyers.

An NRR over 100% indicates a firm is increasing year-over-year revenue with existing customers. Investors and acquirers place a valuation premium on acquisition targets with an NRR over 100%. A higher NRR reduces dependency on new sales, reduces overall operating risks, and promotes a higher EBITDA margin for the business by keeping sales and marketing costs low. In mergers and acquisitions, NRR is a key metric to evaluate the quality of recurring revenue. Acquirers often prioritize companies with NRR above 100%.

HIGH NET REVENUE RETENTION (NRR)

Example

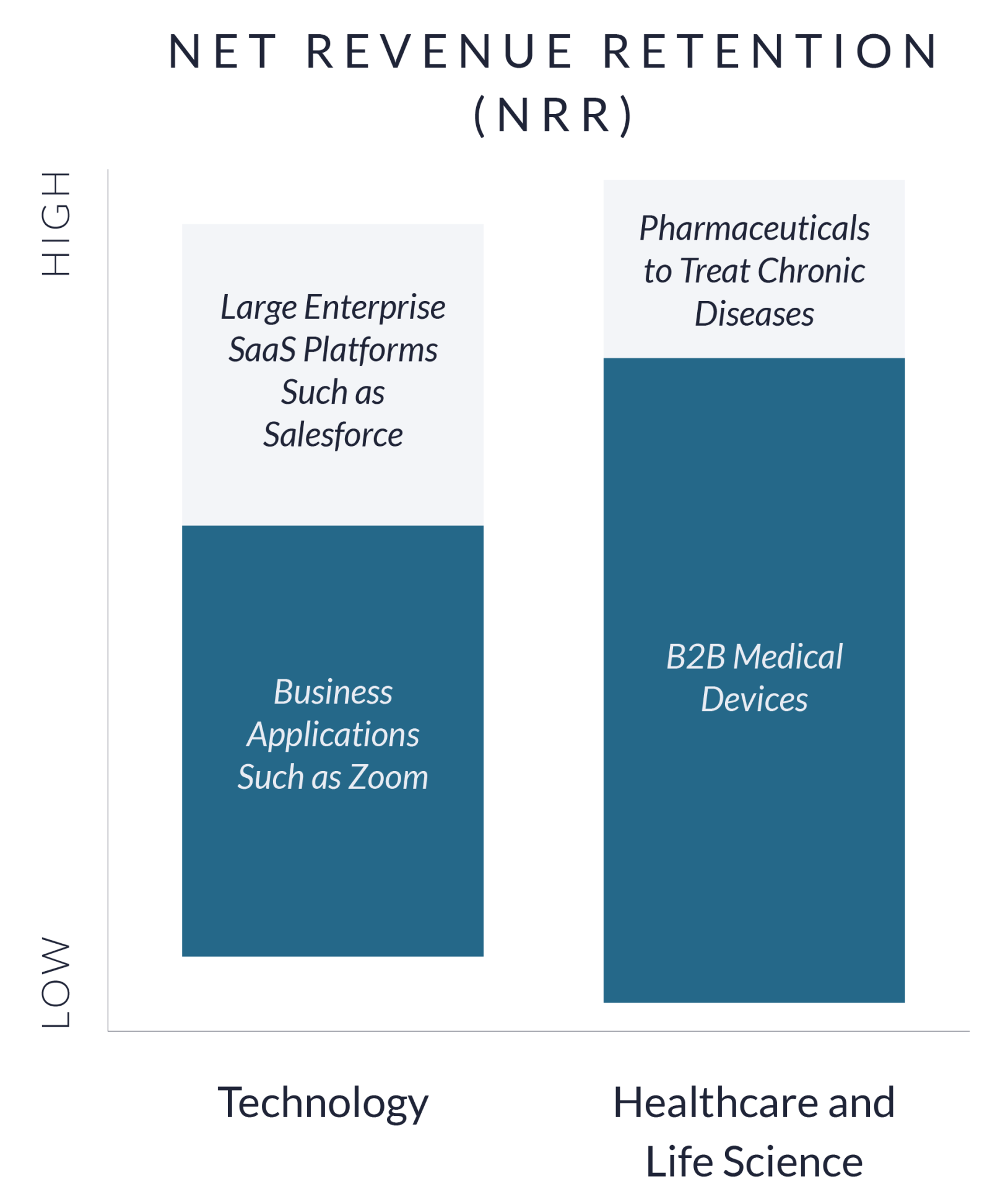

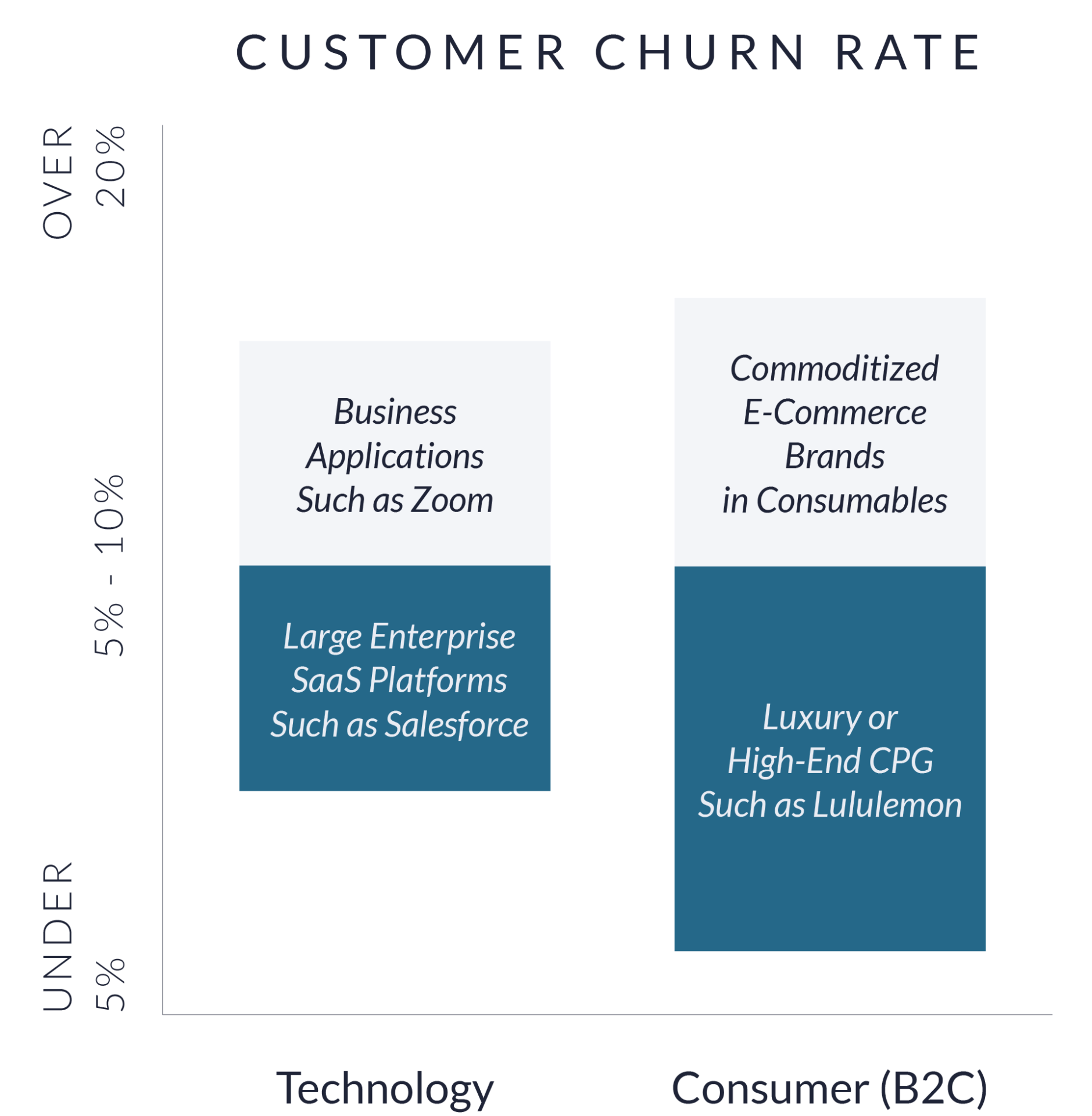

Zoom Video Communications has historically reported a strong NRR, particularly with enterprise clients, where its NRR exceeded 130% during the pandemic. However, in recent reports, Zoom’s NRR from its enterprise segment was 101% in Q4 2024, down from 115% in 2023. Zoom increases its NRR by encouraging enterprise clients to add users, upgrade to premium features, and host webinars. NRR can be negatively impacted by competition and customers opting for less expensive plans. NRR can be benchmarked relatively across industries. The following chart indicates what kinds of industries can expect the highest or lowest NRR ratios.

Since NRR is a function of how stable current contracts are plus how much contracts are expanded with existing customers, contracts that are long-term and multi-year in nature support an overall higher NRR. As such, SaaS companies with multi-year agreements generally exhibit the greatest NRR compared to their peers. The easier it is for customers to switch products or services, or the number of competitors offering a similar product or service, will also lower NRR within a given industry or company sector because it is easier for customers to cancel current contracts and receive products and services from a comparable provider.

Enterprise SaaS and healthcare consistently achieve high NRR due to recurring revenue streams, upselling opportunities, and high switching costs for customers to move to a competitor. Sectors with sticky products (pharmaceuticals, enterprise IT) outperform sectors relying on one-off purchases (transactional services, e-commerce).

Customer Churn Rate

Customer churn rate measures the percentage of customers who cancel or do not renew their subscription over a specific period, relative to the total number of customers at the start of that period. It tracks the number of customers lost, not the revenue associated with them. Companies with low customer churn command higher valuations due to their ability to maintain and grow their customer relationships effectively. However, this is not paid upfront in M&A transactions, as it needs to be evaluated by the buyer to assess its long-term impact on revenue stability.

High customer churn rates indicate that a significant portion of a company’s customer base is leaving within a specific period, signaling potential issues with product quality, product fit, customer satisfaction, or competitive pressure. This can lead to increased customer acquisition costs (CAC) as the company must consistently replace lost customers to sustain growth. High churn may also hinder word-of-mouth referrals, reduce brand loyalty, and negatively affect overall customer lifetime value (LTV). A low customer churn rate demonstrates strong customer satisfaction, loyalty, and engagement with the product or service.

LOW CUSTOMER CHURN RATE

Retaining customers is generally more cost-effective than acquiring new ones, allowing companies with low churn to allocate resources more efficiently toward product improvements, scaling operations, or expanding their market presence. In mergers and acquisitions (M&A), the customer churn rate is closely scrutinized as it provides insights into customer retention, the stickiness of the offering, and the long-term viability of the customer base.

Example

Salesforce has reported a consistent customer churn rate of approximately 8% in recent fiscal periods. In the second quarter of FY 2024 the company maintained this churn rate, aligning with previous periods.

To address customer churn, Salesforce implemented a comprehensive churn analysis program. This initiative involved collecting exit surveys and analyzing customer feedback to identify the root causes of churn, such as product dissatisfaction, pricing concerns, and customer service issues. By categorizing and addressing these areas, Salesforce achieved a 15% reduction in customer churn.

Low churn sectors (technology, healthcare, and enterprise IT) benefit from sustained customer need for their products or services. The long-term demand for these services drives customer loyalty and lowers churn. Companies like Salesforce provide essential platforms that businesses rely on for daily operations. These services often become indispensable to companies’ workflows, making it more likely they will continue using them for the long term. The products are deeply embedded in processes, so businesses have a vested interest in maintaining them.

Luxury or high-end CPGs retain customers due to brand loyalty, though growth may be capped by purchase frequency and consumer spending trends whereas commoditized e-commerce brands and OTT platforms struggle to secure recurring revenue due to low brand loyalty and switching costs.

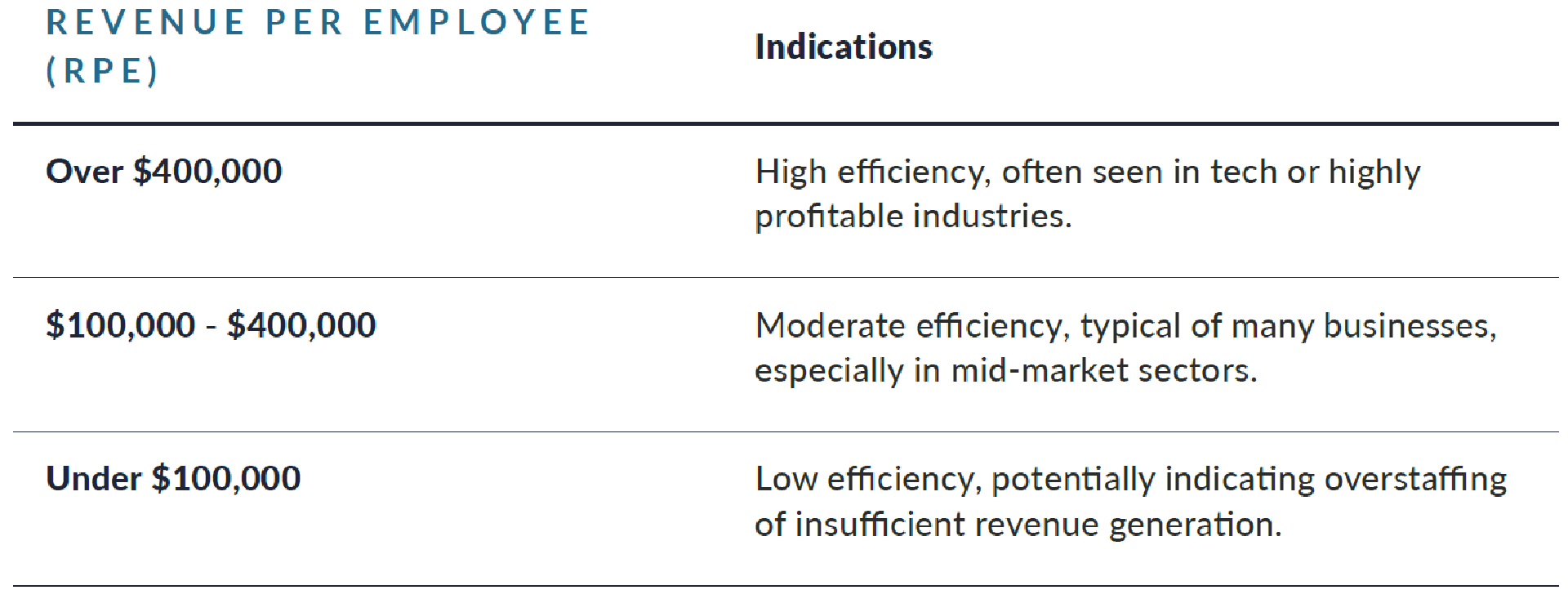

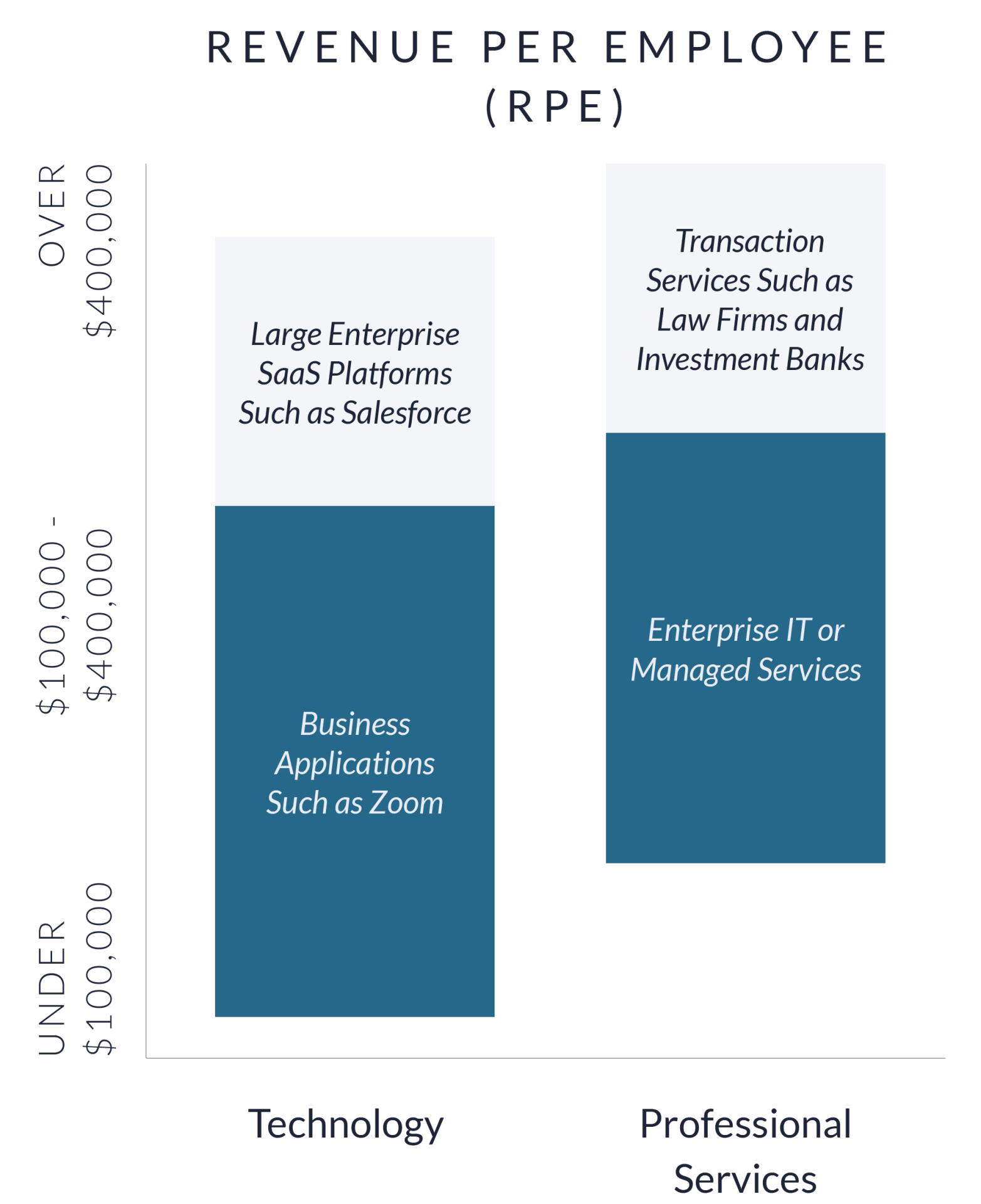

Revenue per Employee (RPE)

RPE indicates how much revenue each employee generates and is used to measure workforce productivity. Since RPE directly reflects a company’s revenue efficiency, it can impact valuation and M&A payment consideration, particularly for subscription-based buyers who prioritize scalable and efficient revenue growth.

A high revenue-per-employee ratio indicates that a company is efficiently utilizing its workforce to generate revenue, often through optimized processes, automation, or the effective use of technology. A low RPE ratio may signal inefficiencies, such as underutilized staff or operational bottlenecks that hinder growth.

HIGH REVENUE PER EMPLOYEE (RPE)

Several factors influence RPE, including the business model, where subscription-based companies with high customer retention and low churn tend to have higher RPE due to recurring revenue. Companies that leverage automation, AI, and other technologies for sales, marketing, and customer support also see higher RPE, as these tools enable them to accomplish more with fewer employees.

Large enterprise SaaS platforms like Salesforce often exceed $400,000 in annual RPE, with fewer employees required to generate revenue.

Example

Shopify, a leading e-commerce platform that enables businesses to set up and manage online stores, demonstrates excellent RPE due to its highly automated and scalable platform. In 2023, Shopify’s revenue per employee (RPE) was approximately $850,000. This high RPE reflects Shopify’s efficient business model, which leverages automation and technology to scale operations without a proportional increase in staff.

Law firms achieve high RPE due to premium pricing and value concentration in the legal services provided by these firms, driven by their focus on specialized client work. For example, Kirkland & Ellis, with a reported revenue per lawyer of $2 million, would see an adjusted RPE of approximately $1.8 million when accounting for non-lawyer employees, assuming a 10% non-lawyer support staff. Similarly, Latham & Watkins’ RPE would adjust from $1.8 million to $1.6 million, and DLA Piper’s from $840,000 to $756,000. All these law firms have RPEs greater than some SaaS benchmarks such as Salesforce.

Unlike law firms, which rely on specialized expertise and high-stakes engagements, enterprise IT companies achieve revenue by leveraging large teams and standardized processes, leading to lower RPE on average.

Intangible Assets That Impact B2B Subscription Company Valuations

Customer Lists

Customer lists are a foundational asset, representing the database of businesses that a B2B subscription company has engaged with or targeted. As a type of intangible asset, customer lists are typically categorized under goodwill or other intangible assets after an acquisition. These lists are usually curated and maintained by marketing and sales teams, who leverage them for customer outreach, segmentation, and lead generation. A well-maintained and segmented customer list can offer insights into market reach, enabling companies to identify high-potential customer segments, therefore driving upselling opportunities by pinpointing existing customers who may benefit from expanded offerings, as well as informing product development to align with customer needs. Additionally, customer demographics derived from these lists help in tailoring marketing strategies, directly influencing future revenue projections. In mergers and acquisitions, the quality and size of customer lists often play a significant role in valuation, as they are key indicators of market reach, revenue potential, and growth opportunities. Customer lists increase valuations in large transactions and represent contingent considerations in M&A structures, as they provide insights into potential growth and customer retention. They can be particularly valuable to strategic acquirers in similar or complementary industries, offering opportunities not only to scale the acquired business but also to cross-sell their own products or services, which drives growth across the acquirer’s core business as well.

CUSTOMER LISTS

Customer Contracts

B2B subscription company transactions revolve around recurring revenue streams underpinned by customer contracts, which are vital intangible assets contributing to a company’s valuation. These contracts formalize the relationship between the company and its clients, detailing terms of service, pricing structures, renewal conditions, and engagement duration. Metrics like annual recurring revenue (ARR), customer lifetime value (CLV), churn rate, and net revenue retention (NRR) highlight revenue predictability, growth, and customer satisfaction. Favorable contract terms, such as auto-renewals, annual price escalations, and service level agreements (SLAs), enhance revenue stability, embed customers in long-term engagements, and reduce churn. They also provide a foundation for upselling and cross-selling opportunities, driving scalable revenue and customer retention. Well-negotiated customer contracts further enhance valuation and can impact the upfront consideration in transaction structures, as they provide stability and reduce risk for the buyer, ensuring future revenue streams are more predictable.

CUSTOMER CONTRACTS

Customer Relationships

Customer relationships encompass the trust and loyalty that a company builds over time, which are especially critical for B2B subscription companies. Strong customer relationships often lead to lower churn rates, higher customer lifetime value (CLV), and a competitive edge in the market. These relationships, while intangible, are a key differentiator as they foster positive word-of-mouth referrals—a tangible indicator of customer satisfaction—and opportunities for upselling or cross-selling. Referrals, in particular, serve as a powerful validation of these relationships, reinforcing a company’s market reputation and reducing customer acquisition costs. Accounting standards (IFRS and US GAAP) generally require intangible assets to be identifiable and measurable, making internally generated customer relationships difficult to record on the balance sheet. However, their value is often reflected in a company’s earnings power, retention metrics, and overall financial stability, significantly impacting its valuation during mergers, acquisitions, or other financial analyses. Customer loyalty, backed by a steady stream of referrals, can translate into higher contract renewals, predictable revenue streams, and long-term growth potential, which are highly attractive to investors and stakeholders. However, customer relationships have the least impact on valuation and upfront payment consideration as their value is more difficult to assess directly.

CUSTOMER RELATIONSHIPS

Valuation Multiples Reflect Subscription Metric Performance

In the B2B subscription space, transaction valuation multiples serve as a reflection of a company’s underlying performance, particularly in key subscription metrics. As shown in the chart above, companies commanding higher valuation multiples, such as Shopify and Salesforce, exhibit stronger subscription-based fundamentals—high customer retention, predictable recurring revenue, and scalable growth models.

Conversely, firms with lower implied multiples, like Medtronic and Slater and Gordon, may operate with less favorable subscription economics, such as weaker renewal rates or higher customer acquisition costs. This is a critical takeaway for both investors and operators: valuation premiums in B2B subscription M&A are not merely a function of revenue size but are deeply tied to the efficiency and quality of the underlying subscription business. Companies aiming for higher valuations in the M&A landscape must prioritize improving their core subscription metrics. Strong net revenue retention, low churn, and a well-optimized customer acquisition engine are among the key drivers that translate into premium multiples in this evolving market. Valuation multiples can be impacted by factors outside the KPIs in this report, but they are definitely a material driver.

The valuation drivers for B2B subscription companies in M&A transactions are influenced by a blend of financial metrics and intangible assets. Key tangible drivers highlighted in this report such as lifetime value (LTV), customer acquisition cost (CAC), net revenue retention (NRR), and intangible assets like customer contracts and relationships are central to shaping valuations in businesses.

Ultimately, acquirers focus on B2B subscription companies that demonstrate financial resilience, operational efficiency, and a strong foundation of customer loyalty, which mitigate risks and enhance future profitability. Business owners must understand and optimize these valuation drivers to position themselves as attractive targets in M&A transactions, showcasing their strength through robust financial reporting, detailed retention and churn metrics, proven customer success strategies, and clear evidence of scalable, recurring revenue growth.