[vc_row dfd_row_config=”full_width_content”][vc_column][vc_column_text el_class=”blog-glance”]

[/vc_column_text][/vc_column][/vc_row][vc_row dfd_row_config=”full_width_content” el_class=”blog-img-section”][vc_column][vc_single_image image=”9178″ img_size=”full”][/vc_column][/vc_row][vc_row dfd_row_config=”full_width_content”][vc_column][vc_column_text]The Gulf states and Israel provide an opportunity for the US to participate in a global economy that will be more centered on the Middle East than it was before the virus. This future must be a cornerstone of US policy, as well the legacy issues around security.

Covid has threatened the mature economies of the US and Europe, accelerated China’s inevitable rise, and given opportunity to the region’s often more agile and adaptable countries.

There are few countries in the world who have (almost) put the pandemic behind them and are on good terms with both the US and China. Those are the countries who are set to lead the world in the 21st century. They are almost exclusively in the Middle East.

The rise of the Middle East as a gateway between the US and China presents an opportunity for Biden to re-engage with Beijing through the neutral soil of Israel and the Gulf states. Biden should not be afraid of celebrating and building on the diplomatic progress achieved under the Trump administration through the end of the GCC rift and the Abraham accords.

Being the “new Europe” is something that Middle Eastern leaders are understandably motivated by, particularly in light of their relations with both DC and Beijing. Europe was the middle ground for the Soviet-US Cold War, and the Middle East is the same for the China-US relationship — geographically, politically and economically.

Rather than continue to fight yesterday’s conflicts and ignore today’s achievements (perhaps focused on distancing himself from Trump’s policies), Biden should craft policy based on the reality that the Middle East is transitioning from a 20th century defined by conflict and insecurity to a 21st century where the Silk Road is once again the social, economic, cultural, and political center of the world.

This is a future into which the Middle East is rapidly progressing. Three of the top five countries with the most Covid vaccinations (excluding the Seychelles and Maldives) are in the Middle East — namely the UAE, Israel, and Bahrain. In addition to a successful vaccination campaign, total death rates in these countries and others in the region have remained low. All this while key industries, including tourism, have often remained open.

Saudi Arabia has been working to almost triple its non-oil revenues, and is investing billions into futuristic cities like NEOM and “The Line.” The UAE successfully completed a mission to Mars during the pandemic and recently announced plans to double Dubai’s population, all while commentators in London and New York discuss the “death of cities.”

Gulf economies also benefit from a low debt to GDP ratio, which will allow them to maintain growth while more developed and leveraged economies struggle in the wake of the pandemic. The US currently has a debt to GDP ratio of over 100 percent; in Saudi Arabia and the UAE, the debt to GDP ratio is only 20 percent, meaning those governments will have spending power well into the future for public and private projects.

China is busy building deeper links in the region, where doing business is more important than talking politics. It is important to Biden’s legacy that US policymakers and investors do the same, and foster both cultural and economic connections to the new Middle East rather than allowing themselves to be crowded out.

To this day, too many American political and business leaders are driven by the impulses that impacted actions between them and the Middle East at the start of the millennium. Twenty years on, the White House should look to the future. It must adapt to the rise of China by utilizing the Middle East’s neutral ground to increase cooperation with Beijing.

It’s high time an American president looked to the Middle East for its entrepreneurship, adaptability and its e-governance, rather than simply for its oil.

Joshua Jahani is a Cornell alum, public speaker and investment banker with a focus on the Middle East and Africa

https://www.independent.co.uk/voices/biden-china-meeting-middle-east-b1819729.html[/vc_column_text][/vc_column][/vc_row][vc_row el_class=”more-from-report”][vc_column][vc_column_text]

[/vc_column_text][vc_row_inner][vc_column_inner width=”1/2″][vc_column_text]https://www.bbc.com/news/world-middle-east-35221569[/vc_column_text][vc_column_text]https://www.politico.com/news/2021/03/29/us-biden-iran-nuclear-deal-478354[/vc_column_text][vc_column_text]https://www.reuters.com/article/us-iran-nuclear-usa/bidens-iran-approach-praised-as-deft-despite-lack-of-progress-idUSKCN2AW2SB[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/2″][vc_column_text]https://www.bbc.com/news/world-middle-east-42008809[/vc_column_text][vc_column_text]https://www.washingtonpost.com/world/2021/03/19/biden-iran-deal-stalemate/[/vc_column_text][vc_column_text]https://www.nbcnews.com/politics/national-security/biden-administration-says-it-s-ready-nuclear-talks-iran-n1258299 [/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row el_class=”more-from-report” disable_element=”yes”][vc_column][vc_column_text]

[/vc_column_text][vc_row_inner][vc_column_inner width=”1/2″][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/2″][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][vc_column_text]Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam[/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row dfd_overlay_color=”#e9ecf2″ el_class=”access-article”][vc_column width=”1/2″][vc_column_text]

[/vc_column_text][/vc_column][vc_column width=”1/2″][dfd_button button_text=”Explore the full article” buttom_link_src=”url:%23|||” style=”style_1″ box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” hover_box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” el_class=”blue-btn”][dfd_button button_text=”Download the PDF” buttom_link_src=”url:%23|||” style=”style_1″ box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” hover_box_shadow=”box_shadow_enable:disable|shadow_horizontal:0|shadow_vertical:15|shadow_blur:50|shadow_spread:0|box_shadow_color:rgba(0%2C0%2C0%2C0.35)” el_class=”blue-btn”][/vc_column][/vc_row]

Taiwan’s rail company says 36 people are known to have died, and dozens injured. Myanmar’s deposed leader Aung San Suu Kyi had already been accused of breaking COVID-19 rules and illegally possessing walkie-talkies—now she’s been charged with violating the country’s official secrets act. And the story of the Italian businessman who tried to fake his own kidnapping for financial gain, but ended up as a prisoner of a jihadist group for three years.

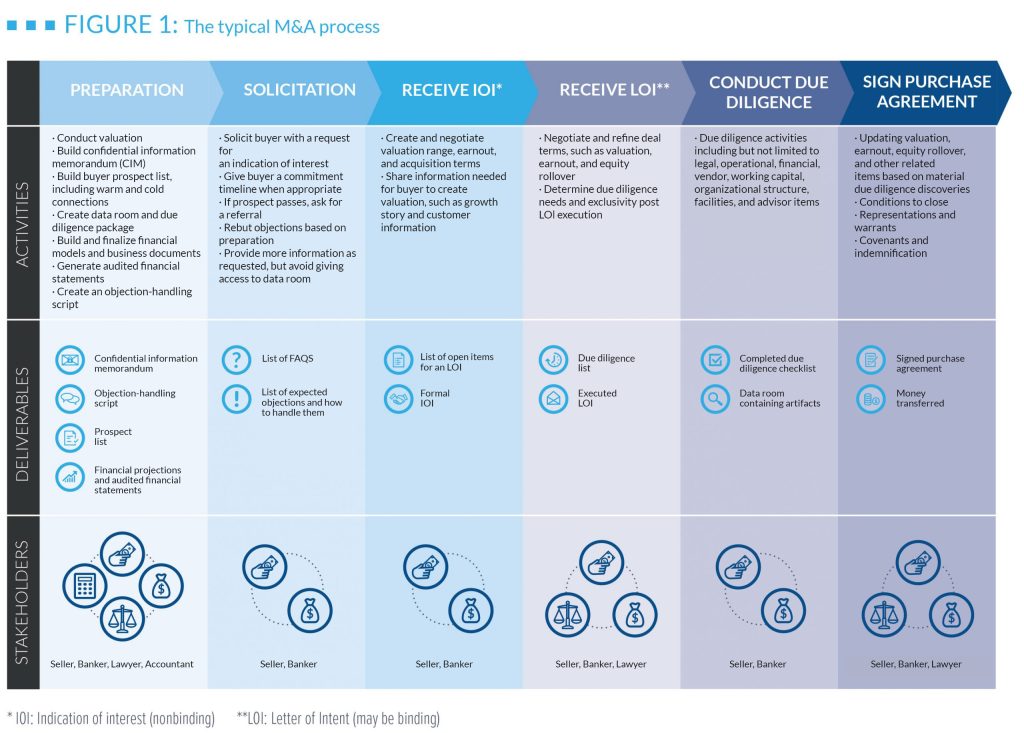

The sell-side M&A process is long and complex. Bringing a company to market does not guarantee the company will achieve its M&A goals. The M&A process is challenging for three reasons:

This report contains the step-by-step guide Jahani and Associates (J&A)—an NYC-based global independent investment bank—uses to maximize results for its clients. Each step in the sell-side M&A process is driven by activities, deliverables, and solutions.

Preparation to solicitation requires the company and their investment banker to generate the artifacts buyers need to make an offer for the company. This information includes but is not limited to financial information, the growth history of the company, intangible asset information (e.g., customer relationships and proprietary technology), and the reasons the owners are selling the business.1 This information must be woven together and organized correctly so buyers can efficiently formulate their offers.

Industry-standard deliverables, such as a confidential information memorandum (CIM) and audited financial statements, are used in this phase to market the business to potential buyers.

This is arguably the most important part of the sell-side M&A process. Reaching the sufficient number of solicitations to ultimately find an interested buyer is difficult and incredibly important, particularly in the lower-middle and middle markets. The volume of solicitations necessary is higher than most professionals expect. The methods to generate qualified buyer leads also vary based on the industry, region, and type of investment bank (e.g., healthcare investment bank, agritech investment bank, etc.). Solicitation is initiated with a blind teaser, using a code name in lieu of the company’s name. Buyers may request more information after the teaser—at which point a nondisclosure agreement (NDA) is required. J&A recommends only sending detailed material during the preparation phase to potential buyers after they have signed the NDA. For sellers to create a succinct and consistent story for all potential buyers at this stage, it is very important not to provide too much information.

Common sources of buyer solicitations include direct connections from an investment banker’s warm network, introductions and referrals from partners in the investment banker’s network, direct solicitations of qualified buyers determined from research (e.g., PitchBook), and target emails to qualified lists of buyers. Coordinating all four types of outreach is a complicated task. Figure 2 demonstrates common reasons for failure and how J&A recommends sellers and their advisors avoid them.

IOIs contain valuation ranges and general expectations of earnout. These should be negotiated as necessary to have a smooth transition from an IOI to an executable letter of intent (LOI). IOIs are nonbinding.

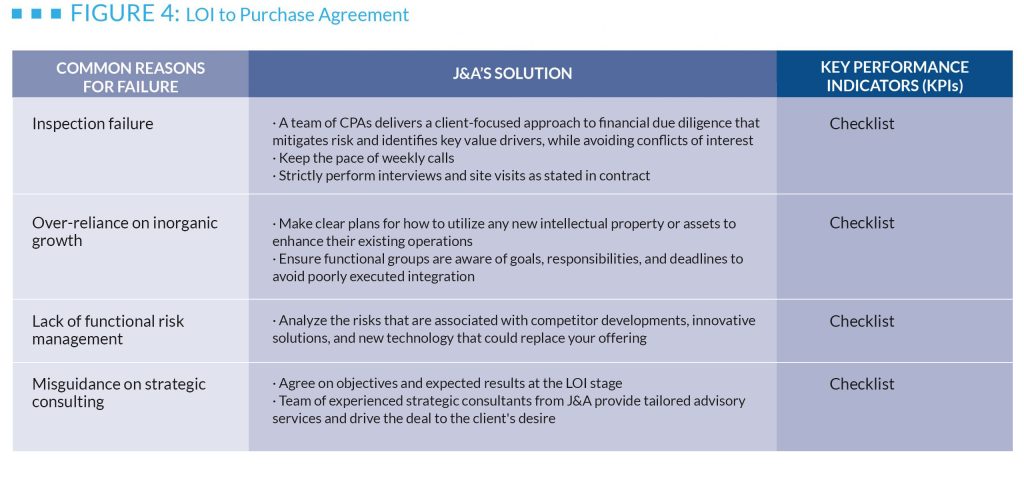

A site visit usually occurs while transitioning an IOI to an LOI. The visit is an opportunity for the buyer and seller to meet and conduct a deep dive into any outstanding items that need to be settled before executing an LOI. Since LOIs are legally binding, many buyers will require exclusivity after an executed LOI, which is also referred to as a “no-shop clause.” This means the seller will not be able to conduct sale-related conversations during the no-shop period and must ensure the upcoming due diligence will be satisfactory in order to close the deal.

Due diligence is often the longest part of the sell-side M&A process. Depending on the size and complexity of the deal, it may take up to 120 days.2 Due diligence is the process of affirming the information the buyer has used to make its offer and determining whether or not the company is in good standing with the relevant administrative, legal, financial, technological, security, operational, and other information in its possession.

Once due diligence is complete, executing the purchase agreement is the final step in the sell-side M&A process. These agreements can either be asset purchases or stock purchases. The purchase agreement is the binding contract where ownership officially changes hands. If due diligence went as expected, this step should be relatively simple. The changes that may affect purchase agreement negotiations are material discoveries in due diligence, economic forces, material alterations in the business’ operations, and management changes. It is very important for business activities to go according to plan during due diligence.

Jahani and Associates collected common challenges that exist in each step of the sell-side M&A process and the best way to resolve them. It is important for M&A stakeholders to plan ahead and know where expected weaknesses may lead to exacerbated challenges.

It is imperative the investment banking team has a plan to resolve these challenges before they even arise in order to avoid disruptions or delays in the M&A process.

Companies most often do not go from preparation to solicitation when seller management teams are not aligned or properly prepped for the sell-side M&A process. This can occur when multiple stakeholders are involved, particularly in companies boasting a significant capital raise. A seller may also not move to the solicitation phase due to major market forces negatively affecting business performance. If a business undergoes a change that materially reduces the company’s desired valuation, management often decides to postpone the process.

Fundamentally, solicitation to IOI is a sales process. Therefore, sellers and their teams are most prepared when they view this as a sales exercise. This is often the most difficult step in the process for unprofitable companies in the lower-middle market.

Moving from an IOI to LOI is a matter of negotiation and mutual understanding between the buyer and seller. A site visit is often used in between the IOI and LOI to develop a relationship between the buyers and sellers.

Due diligence is the process of confirming the buyer’s understanding of the business at the time they made their offer. Due diligence is time-consuming. Material information that changes the valuation and earnout identified in the LOI may be discovered during due diligence. This will be negotiated as part of the purchase agreement. Purchase agreements may be made for either cash or stock, each of which has its own tax, legal, and strategic considerations.

The challenges, solutions, and KPIs in this paper are not exhaustive, but they provide an overview of the way to maximize success in sell-side M&As. It is important that all stakeholders understand the challenges they will face and how to alleviate them as quickly as possible. Establishing a consensus among stakeholders from the outset will also help mitigate any issues that may unfold. Focusing on a problem-solution-KPI framework gives transparency to the client and allows the investment banker to increase the size of their team while preserving client service and information sharing. Experience in dealing with these issues is paramount to successfully delivering M&A results, and that experience must be coupled with actionable outcomes.

Any business owner seeking to sell their business must carefully consider all these factors. Being aware of expected obstacles and how to overcome them early will significantly increase the likelihood that a company successfully completes a sell-side M&A transaction. The analysis contained herein is based on decades of experience and is included to support business owners across the world as they achieve a maximally successful exit.

In 2019, Jahani and Associates surveyed hundreds of business owners about successful and failed M&A deals, why they failed, and how those failures could have been avoided. J&A then compared these stories with its own processes and tools to determine the best way to anticipate and avoid these failures in any M&A scenario. The resulting analysis is this document that outlines common reasons for failure and how to avoid them. This document is meant to serve as a resource to business owners and other service providers to give the best strategic advice and service for their businesses or clients.

Jahani and Associates (J&A) is an independent investment bank located in New York, New York. The firm specializes in healthcare and technology and provides specialized M&A and capital markets advisory services. The combination of J&A’s unmatched skills in technology, engineering, and business operations allows the firm to create sustainable value for its clients. J&A works at the intersection of cutting-edge financial theory and business practicality. Creativity is highly valued within the firm, which allows J&A to continually improve the way businesses thrive.

The Gulf states and Israel provide an opportunity for the US to participate in a global economy that will be more centered on the Middle East than it was before the virus. This future must be a cornerstone of US policy, as well as the legacy issues around security.

The COVID-19 pandemic has threatened the mature economies of the US and Europe, accelerated China’s inevitable rise, and given opportunities to the region’s often more agile and adaptable countries.

There are few countries in the world that have (almost) put the pandemic behind them and are on good terms with both the US and China. Those are the countries that are set to lead the world in the 21st century. They are almost exclusively in the Middle East.

The rise of the Middle East as a gateway between the US and China presents an opportunity for Biden to re-engage with Beijing through the neutral soil of Israel and the Gulf states. Biden should not be afraid of celebrating and building on the diplomatic progress achieved under the Trump administration through the end of the GCC rift and the Abraham Accords.

Being the “new Europe” is something that Middle Eastern leaders are understandably motivated by, particularly in light of their relations with both DC and Beijing. Europe was the middle ground for the Soviet-US Cold War, and the Middle East is the same for the China-US relationship—geographically, politically, and economically.

Rather than continue to fight yesterday’s conflicts and ignore today’s achievements (perhaps focused on distancing himself from Trump’s policies), Biden should craft policy based on the reality that the Middle East is transitioning from a 20th century defined by conflict and insecurity to a 21st century where the Silk Road is once again the social, economic, cultural, and political center of the world.

This is a future into which the Middle East is rapidly progressing. Three of the top five countries with the most COVID-19 vaccinations (excluding the Seychelles and the Maldives) are in the Middle East—namely the UAE, Israel, and Bahrain. In addition to a successful vaccination campaign, total death rates in these countries and others in the region have remained low. All this while key industries, including tourism, have often remained open.

Saudi Arabia has been working to almost triple its non-oil revenues, and is investing billions into futuristic cities like NEOM and “The Line.” The UAE successfully completed a mission to Mars during the pandemic and recently announced plans to double Dubai’s population, all while commentators in London and New York discuss the “death of cities.”

Gulf economies also benefit from a low debt-to-GDP ratio, which will allow them to maintain growth while more developed and leveraged economies struggle in the wake of the pandemic. The US currently has a debt-to-GDP ratio of over 100%; in Saudi Arabia and the UAE, the debt-to-GDP ratio is only 20%, meaning those governments will have spending power well into the future for public and private projects.

China is busy building deeper links in the region, where doing business is more important than talking politics. It is important to Biden’s legacy that US policymakers and investors do the same, and foster both cultural and economic connections to the new Middle East rather than allowing themselves to be crowded out.

To this day, too many American political and business leaders are driven by the impulses that impacted actions between them and the Middle East at the start of the millennium. Twenty years on, the White House should look to the future. It must adapt to the rise of China by utilizing the Middle East’s neutral ground to increase cooperation with Beijing.

It’s high time an American president looked to the Middle East for its entrepreneurship, adaptability, and its e-governance, rather than simply for its oil.

In the first two articles of this series, Identifying Intangibles in Ad Tech M&A Value and Developing Intangibles in Ad Tech M&A Value, we specified how you, the business owner, can identify and develop your company’s most valuable intangible assets to maximize your value.

In any M&A deal, sellers highlight the importance of their intangibles so the buyer can use them to create a competitive advantage. The third step in this process, learning how to monetize your business’ intangible assets, is where you reap the fruits of your labor. This step occurs when the buyer pays a price for the intangibles you have identified and developed. This includes the steps leading up to the sale, such as valuation, negotiation, pitching, and due diligence. So how do you monetize intangibles?

An M&A valuation can be conducted in several ways, including through a business appraisal or the valuation of a public company’s stock. The valuation of your company often amounts to a number that is negotiated between the seller and the buyer. Middle-market companies in particular possess a range of values based on the buyer’s profile. Fair market valuation is the most common valuation technique.

Fair market valuation occurs when you determine how similar businesses have sold based on multiple types and multiple factors. Multiple types include earnings before interest, taxes, depreciation, and amortization (EBITDA), annual recurring revenue (ARR), and, in some cases, book or tangible asset value. Multiple factors (referred to as 3X, 4X, or 10X) simply identify the number you agree to multiply the selected factor by to determine the valuation number.

Obviously, multiple types and factors depend on industries with similar characteristics to the company being valued. For example, industry growth, the strength of the management team, competitive advantages, access to suppliers, and access to buyers can all influence multiple types and factors.

The Accounting Standards Codification (ASC) 805 allows the business owner to understand how the expected purchase price can be broken down based on the transaction’s fair market valuation and associated purchase premium or goodwill. In the ad tech industry, the amount paid for goodwill makes up, on average, 70% of the purchase price. This means, for example, that a company with a fair market valuation of $100 and 70% goodwill was purchased for $170.

At J&A, our banking practice conducts detailed M&A studies of goodwill and purchase price allocation to understand why companies command a premium and how business owners can make sure they land at the top of valuations when selling their businesses. After looking at over 500 M&A transactions executed by technology giants over a six-year period, we segmented purchases by industry and certain goodwill parameters, narrowing our study to 34 purchased companies. These 34 ad tech M&A transactions completed at the greatest premiums had the following two things in common: the target company increased the data interfaces of the acquiring company and the target company increased the data processing power of the acquiring company.

Data interfaces and data processing power are both intangible assets. These intangibles were systematically identified and developed by the business owners over time before they sold their companies. The monetization of those assets became effective when the companies were purchased at higher than average premiums.

This analysis becomes the cornerstone of an effective M&A strategy. Armed with the framework of identifying, developing, and monetizing intangible assets, business owners have a predefined plan they can take to increase their company’s value.

As a business owner, you should always study different purchase premiums in your industry to identify drivers that will create the highest return for your business. Using ASC 805 principles to uncover M&A value allows you to create a roadmap that will help you land on the high end of valuation because it is a scientific way to tie your valuation to intangible assets.

Intangible assets can only be monetized if you have measured them in-depth. There is an infinite number of intangible assets you can identify, develop, and monetize.

As a business owner, you must determine which ones you can leverage most effectively. Trusted advisors can help you create a clear vision and strategy to maximize your company’s value. The role of intangible assets in M&A markets will increase over time. The most successful companies will use the information presented in these articles to maximize the value of their company.

Part I: Identifying Intangibles in Ad Tech M&A Value >

Part 2: Developing Intangibles in Ad Tech M&A Value >

Photo by Vincent Tantardini on Unsplash

In our earlier article Identifying Intangibles in AdTech M&A Value, we explored how you, as a business owner, can identify the intangible assets that make your company more valuable during the M&A process. After identification is complete, the next step is to develop those same intangible assets. Developing intangible assets relies on key performance indicators (KPIs) in the same way identifying intangibles does. KPIs are the metrics you choose to represent the performance of an intangible asset.

Developing an intangible asset is the set of actions you will take to optimize a KPI. For example, we previously explored how more data interfaces can lead to optimized conversion. Therefore, the intangible asset is the data interface and conversion is the KPI. Optimizing conversion means increasing or decreasing it based on drivers like technology, advertising spends, or advertising quality.

To measure conversion, you must define the desired final action you wish your customer or visitor to take. This could include clicking an ad, buying a product, or providing an email address. The development of the intangible asset (e.g., data interfaces) becomes any action, investment, or improvement you perform to accomplish the final objective (e.g., click, buy, provide email). These developments increase M&A value. In our next article, Monetizing Intangibles in Ad Tech M&A Value, we will show you how to monetize them.

There are multiple ways to develop an intangible asset. Building a company for sale requires considering accounting and banking principles as well as intuitive, strategic ones. Imagine a company that performs direct digital marketing. If this firm wants to increase the number of people who click ads served to drive more website traffic, they have several options to encourage their users to do so:

The best choice for the company is likely a mixture of the five options laid out above. The company must understand that each choice represents a distinct set of intangible assets, all of which are inherently identified and developed when the decision is made. The investments made in one, some, or all of these options are a part of “developing” the intangible asset. The intangibles must be measured and monitored so they can increase corporate value at the time of M&A.

As a business owner, how you choose to develop an intangible asset affects the accounting options available to your management team. Capitalization is a common technique for recording expenses as assets to minimize long-term costs. Specific rules exist about how and when to capitalize expenses that overlap with the development of the intangible assets recommended here. For example, you can capitalize costs to develop patents, copyrights, trademarks, and even proprietary software intangibles, but those costs must be recorded correctly. You cannot simply download a credit card statement 11 months after the expenses were incurred and then claim them as assets.

The principles of identifying and developing intangibles are relevant to business owners because they tie together strategies for growth, development, accounting, and exits. When used correctly, they break down silos between business units and bring together the operation and value of a business. Most venture-capital investors wait for companies to be purchased so the investor can then achieve liquidity. All owners desire M&A options for their hard work. Developing intangibles is the only way to combine the traditional business operations of growing, scaling, and building a company with the gritty accounting principles that affect the valuation and closing of an M&A deal.

Companies are rarely acquired with the intention to conduct business the same way it was conducted before the purchase. Therefore, it is important for you, the seller, to highlight the most valuable intangible assets of your business through their development and investment. This allows the buyer to utilize these intangibles to their own advantage. Ad tech companies are driven by these intangible assets, such as data interfaces, and new technology development that engages specific customers. Measuring these intangibles through the life cycle of the company will affect your exit valuation, creating a more accurate picture of what a buyer is ultimately paying for.

Part 1: Identifying Intangibles in Ad Tech M&A Value >

Part 3: Monetizing Intangibles in Ad Tech M&A Value >

Photo by Alice Achterhof on Unsplash

Identifying Intangibles is the first article in our series about intangible assets.

Part 2: Developing Intangibles in Ad Tech M&A Value >

Part 3: Monetizing Intangibles in Ad Tech M&A Value >

What makes your company special, unique, or valuable? As a business owner, you will be asked this question countless times when you are talking to potential buyers for your ad tech company. But the value of a company is not inherently defined; value is defined differently by parties based on their respective goals, biases, and objectives. For a banker, this discussion is the foundation for all buy-side and sell-side M&A conversations. Based on our experiences and research at Jahani and Associates (J&A), intangible assets make up over 90% of M&A value. There are simple, repeatable processes you can use to increase your company’s value, especially in the ad tech industry (J&A, “Understanding Ad Tech M&A Value”). So how to identify intangibles for M&A?

In 2014, the Financial Accounting Standards Board released an update to ASC 805 addressing how to account for intangible assets in business combinations. ASC 805 is the basis for the financial reporting of intangible assets post-acquisition. Although it is not necessary for you to follow the ASC 805 framework, if you do not utilize it to uncover and measure your company’s intangible assets, you will ultimately limit that value. Businesses can use FASB’s ASC 805 as a framework for maximizing their value prior to beginning M&A conversations.

The first step to maximizing your company’s value is to determine which intangible assets are the most valuable. In order to do so, you must define your desired business objectives. If you are not sure where to start, begin by asking yourself the following questions:

Your business’ relationship with its customers is a symbiotic one: your company exists to serve your customers and your customers are the ones who keep your company in business. Utilizing valuable intangible assets will only enhance the business-customer relationship.

For example, if your desired business objective is to increase the number of users who click the ads placed on your platform (in other words, increase conversion), you need to provide more relevant ads to the user. Tracking cookies from a user’s browser history to service these ads is a common practice to accomplish this relevant placement. This is also known as retargeting. At its core, retargeting is accomplished by increasing the number of data interfaces an ad publisher uses to determine which ads are shown to a user.

Therefore, driven by the objective to increase conversion, data interfaces are intangible assets. Collecting this browser history allows ad publishers to uncover novel patterns, enhance ad relevance, and create new solutions that increase conversion. According to an analysis conducted by Gallup, “companies that apply the principles of behavioral economics outperform their peers by 85% in sales growth and more than 25% in gross margin.”

Data interfaces are just one example. As an owner, you must determine the most valuable intangible assets for your business objectives.

Once you have defined your company’s most valuable intangible assets, you must document the way those intangibles affect your company’s revenue streams. How many events must take place for your intangible asset to create revenue? At J&A, we refer to these as “steps removed” in a process flow. For example, when a user clicks on an ad, the platform owner generates revenue. Therefore, if the intangible asset is a data interface and the presence of more data interfaces increases conversion and revenue, then that asset is one step removed from revenue. Social connections are a more complex example. The presence of social connections on a platform encourages a user to spend more time on the platform, and the more time a user spends on a platform, the more ads the user will click over time. This is two steps removed. The number of steps removed in a process flow completely depends on the business model and business objectives employed. Conversion is important for multiple types of businesses, but the steps between conversion and data interfaces can be drastically different for an infrastructure company and a platform company.

We chose to use revenue in this example because our objective was conversion. Other objectives can include reducing costs, managing risk, or increasing cash flow.

Once you have determined which intangible assets are the most valuable, it is important to measure the outcomes for the selected business purpose over time. Generally, intangible asset data and key performance indicators (KPIs) should be measured for at least one year. Business owners need to determine the right KPIs and track them regularly. The KPIs most related to encouraging conversion are traffic, traffic sources, the technology used to serve ads, and the data that determines when an ad is served.

Knowing how and what to measure is essential to increasing your company’s value. Certain interfaces are more valuable than others. A valuable interface must enhance a desired business objective. Therefore, if your goal is to increase conversion and a certain interface supports that, it is an intangible asset. A popular example of this in the M&A world is Facebook’s purchase of Instagram. Facebook approached Instagram for purchase because Facebook’s application program interfaces (APIs) were increasingly being pinged by Instagram users. Before the acquisition, a Facebook API made Instagram more valuable because it allowed Instagram to use Facebook’s large pool of customer data to enhance its own platform. J&A’s research has also shown that more data interfaces lead to higher purchase price premiums (J&A, “Understanding Ad Tech M&A Value”). Before the acquisition, this integration did not necessarily increase the value of Facebook.

Measuring important aspects of your business and tying them together with corporate financial statements is powerful. Data analyses conducted for thousands of M&A transactions confirm that they can be used to maximize the transactional value for both sides of an M&A before the sale is closed (J&A, “Understanding Ad Tech M&A Value”).

As a business owner, you can utilize the information herein to maximize your company’s value. When developed correctly, this material can significantly impact the value of your organization. Along with specialized bankers, you are uniquely positioned to develop the relationship between intangible assets and corporate financial metrics. Defining the assets that are valuable and then measuring those assets over time is the simplest yet most effective process you can use to increase the overall value of your company.

Part 2: Developing Intangibles in Ad Tech M&A Value >

Part 3: Monetizing Intangibles in Ad Tech M&A Value >

Photo by Neven Krcmarek on Unsplash

Joshua Jahani is a Cornell alum, NYU lecturer, and owner of Jahani and Associates, an investment banking firm focused on identifying and developing a company’s intangible assets to maximize its value. The firm’s Intangible Asset Methodology™ (IAM) is built on systems engineering principles to identify, develop, and monetize intangible assets across a variety of verticals. Utilizing proven qualitative and analytical skills driven by business objectives and up-to-date technology, he has spearheaded the movement towards rapid evolution and sustainable growth using rigorous profitability, ROI, and TCO analysis for organizations of all sizes. Working with exciting startups in digital advertising or large Fortune 500 companies keeps him traveling all over the world.

Joshua Jahani earned his M.Eng. in Systems Engineering from Cornell University in 2012 and teaches courses on strategy, finance, and entrepreneurship at NYU. His current research interests are intangible assets, goodwill calculation and sustainability, the customer franchise value in subscription businesses, and value-based healthcare systems and technology. He has a passion for uncovering how to create corporate value that is not shown on financial statements.

641 Lexington Ave. 15th Floor

New York, NY, USA 10018