Consumer Packed Goods Customization Technology Sector M&A Transactions and Valuations

Consumer Packed Goods Customization Technology Sector M&A Transactions and Valuations

The consumer packaged goods (CPG) customization technology sector merges technology with consumer products to enhance personalization and functionality by integrating advanced technologies for scalable personalization. This sector allows companies to meet increasing consumer demands for personal and practical solutions with customizable products. These firms extend their market reach and generate revenue by licensing their technologies, a strategy that supports growth and diversification for both startups and established companies.

This analysis covers the period from Q1 2020 to Q4 2024, focusing on transaction trends, valuation metrics, and regional dynamics within the sector. It emphasizes the sector’s crucial role in enhancing consumer engagement and satisfaction across various industries where adaptability significantly impacts consumer choices and competitive positioning. The report examines capital flows and deal structures, highlighting key M&A activities such as Shutterfly’s investment in Spoonflower, Redbubble’s acquisition of TP Apparel, and Zazzle’s purchase of Coveroo. These cases illustrate strategic motives and their impact on market consolidation. Additionally, it delves into M&A valuation multiples, including EV/revenue and EV/EBITDA, providing an overview of market trends and valuation patterns.

Targeted at financial advisors, entrepreneurs, and executives, this report offers valuable insights into the drivers of M&A activity and valuation trends in the CPG customization technology sector, helping stakeholders understand and navigate the evolving market landscape.

- Valuation multiples are based on a sample set of private and public M&A transactions in the CPG customization technology sector, using data collected on January 23, 2025.

- A broad spectrum of EV/revenue and EV/EBITDA multiples defines the CPG customization technology sector, reflecting the diverse strategies, development stages, and risk profiles of companies. This variability shows that investors do not follow a uniform valuation approach, as they choose between stable, lower-risk companies and high-potential, higher-risk ventures. High multiples highlight companies with strong market positions and unique technological advantages, while lower multiples indicate companies refining strategies or addressing competitive pressures.

- Companies with lower enterprise values (below $500 million) frequently display very high EV/EBITDA multiples, sometimes exceeding 100x. These high multiples reflect how investors perceive significant speculative growth potential and strategic advantages in the markets. Investors accept higher risks in exchange for the possibility of substantial rewards, emphasizing the dynamic and speculative nature of investments in this sector.

- Larger firms, especially those with enterprise values in the billions, maintain lower and more stable EV/revenue and EV/EBITDA multiples, typically ranging between 1x to 10x. These firms deliver stable performance, predictable cash flows, and established market positions, which reduce investment risk and cap growth premiums. Investors prioritize this stability to achieve predictable returns and minimize volatility, aligning their expectations with the balance between a company’s size and its future earnings potential.

Capital Markets Activities

The data highlights transaction trends, valuation metrics, and regional dynamics in the CPG customization technology sector. Rising consumer demand for personalized products, coupled with advancements in digital and manufacturing technologies, has fueled M&A activity and shaped valuations. Investors are adopting innovative deal structures and targeting strategic geographic markets to leverage the increasing demand for scalable, efficient platforms. These approaches are transforming M&A dynamics, driving innovation, and reshaping the competitive landscape in this rapidly evolving sector.

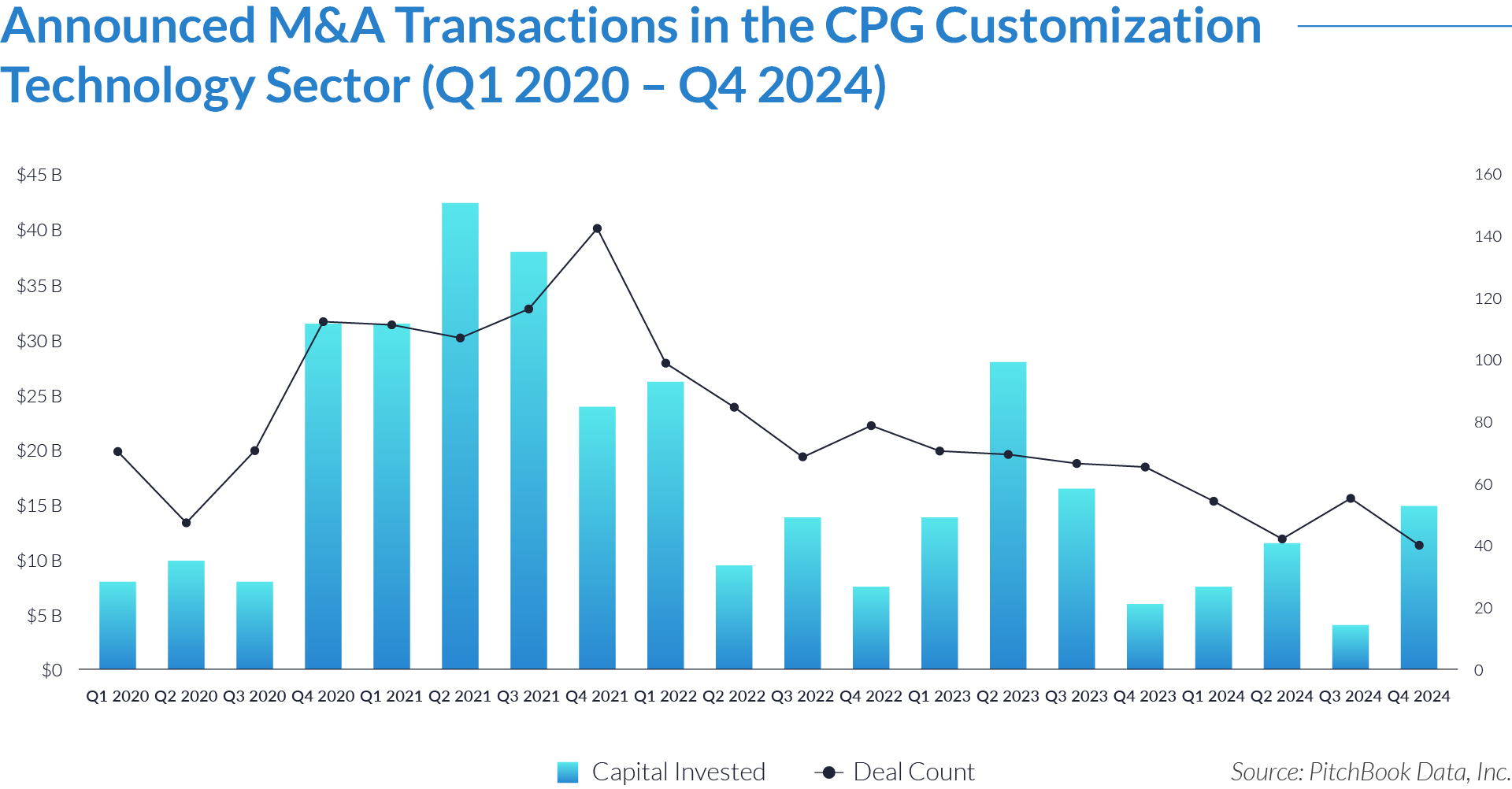

- Investors allocated approximately $348 billion across 1,559 deals from Q1 2020 to Q4 2024, driving significant growth in the CPG customization technology sector. These investments supported the development of advanced personalization tools, scalable platforms, and technologies to meet increasing consumer demand for tailored products, establishing the sector as a key innovator in the consumer goods market.

- Capital investment peaked at $42 billion in Q2 2021, while deal activity reached a high of 141 transactions in Q4 2021. During this period, companies used funding to expand market presence, accelerate technological advancements, and acquire innovative technologies to address rising demand for customized products.

- After the 2021 peak, capital investment and deal count declined, reflecting a shift toward a more mature market. By Q3 2024, deal activity stabilized at 55, as investors focused on fewer, higher-quality transactions emphasizing efficiency, innovation, and sustainable growth. Companies prioritized technologies that could deliver long-term value and enhance competitive positioning in a selective investment environment.

- Capital investment dropped to $4 billion in Q3 2024 due to cautious investor sentiment amid changing economic conditions, but rebounded to $15 billion in Q4 2024, signaling stabilization and a renewed focus on transformative growth opportunities. Investors targeted scalable solutions and impactful technologies that addressed evolving consumer demands for personalization, demonstrating the sector’s resilience and continued ability to attract strategic investments.

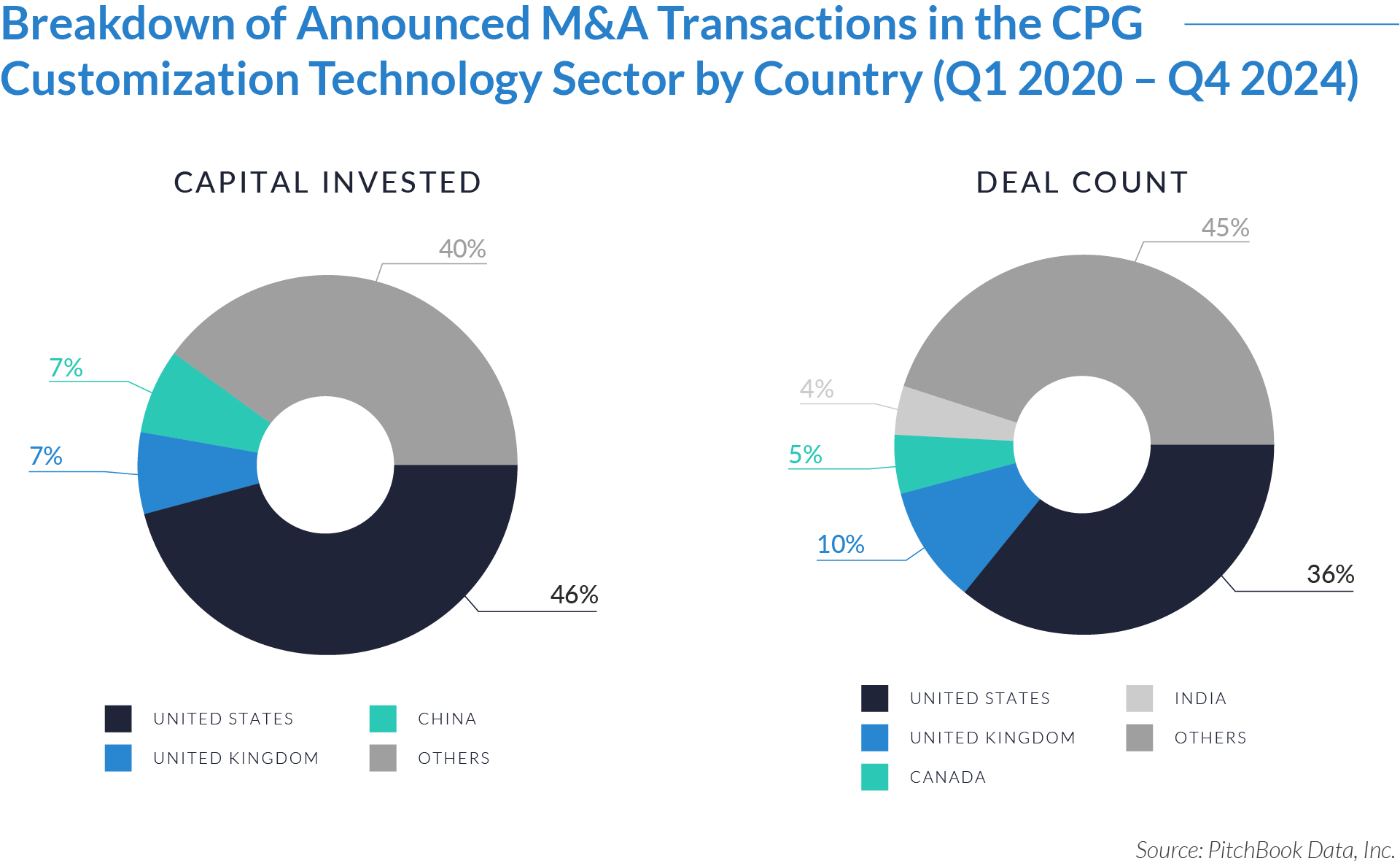

The graphs below present the geographic distribution of transactions, providing additional detail on regional trends and investment dynamics.

- The United States, accounting for 46% of the capital and 36% of the deals, demonstrates its dominance as a central hub for substantial investments and market activity within the CPG customization technology sector. This significant involvement highlights the US’s role in executing high-value, strategic transactions that not only cater to its substantial infrastructure and market appetite for customized products but also reinforce its position as a leader in fostering innovation and shaping global market trends.

- The United Kingdom accounts for 7% of the capital and 10% of the deal count, actively participating in smaller-scale, mid-market investments in the sector. This involvement not only diversifies transaction dynamics but also aligns with the UK’s strategic emphasis on expanding CPG technologies, which benefits from a strong regulatory framework and supportive industry policies that promote innovation and investment in the sector.

- Other markets account for 40% of the capital invested and 45% of the deal count, showcasing active and widespread investment in the sector. This engagement shows the global appeal and potential for international expansion of CPG customization technologies. The contrast between the diverse, global investment strategies and the US’s concentrated, large-scale investments emphasizes the sector’s dynamic presence and innovative growth worldwide.

The deal-type dynamics below set the stage for understanding how capital flows and strategic priorities shape the CPG customization technology sector’s growth and landscape.

- The CPG customization technology sector actively invests in mergers and acquisitions, allocating $226 billion across 1,238 deals. This strategic emphasis on growth through acquisition enables companies in this sector to rapidly advance their technological capabilities and widen their market reach. In the dynamic field of CPG customization, companies significantly enhance their competitive edge by acquiring advanced technologies through M&A.

- Although less frequent than M&A activities, the 321 buyout deals, totaling $122 billion, underscore their strategic significance. Buyouts in the CPG customization technology sector usually result in complete ownership transitions, which provide acquiring companies with direct control over product development and strategic alignment with broader corporate goals. This direct control is vital for fully integrating innovative technologies and maximizing their impact on corporate growth.

- A significant investment gap between M&A and buyouts shows a consolidation trend in the CPG customization technology sector. Larger companies acquire smaller, niche technology providers to reduce competition and broaden their product lines. This consolidation strategy, aimed at leveraging synergies and optimizing the supply chain, is crucial for maintaining competitiveness in a market with rapidly changing consumer preferences.

M&A Transactions Case Studies

Three key M&A transactions in the CPG customization technology sector—Shutterfly’s acquisition of Spoonflower, Redbubble’s acquisition of TeePublic, and Zazzle’s acquisition of Coveroo—demonstrate advancements in market reach, technological integration, and operational efficiency. These deals expanded customer bases, strengthened product portfolios, and leveraged innovative capabilities like print-on-demand and licensed artwork to meet growing demand for personalized products. Each acquisition scaled operations, broadened offerings, and enhanced customer engagement, setting new industry benchmarks.

Case Study 01

SPOONFLOWER

Spoonflower is an e-commerce platform headquartered in North Carolina that specializes in custom, print-on-demand fabrics, wallpaper, and home decor. It allows users to upload their own designs or select from a marketplace of independent artists. Spoonflower appeals to DIY enthusiasts, crafters, and interior designers, with a strong emphasis on sustainability through eco-friendly materials and water-based inks.

Transaction Structure

Spoonflower was acquired by Shutterfly, backed by Apollo Global Management, for $225 million in 2021 through a leveraged buyout.

Market and Customer Segments Combination

The combination of Spoonflower and Shutterfly expanded Shutterfly’s reach into the home decor and DIY crafting markets. Spoonflower’s marketplace of independent artists and eco-conscious customer base aligned well with Shutterfly’s focus on personalized photo products. Together, they served a broad range of consumers, from crafters and designers to individuals seeking unique, sustainable home decor solutions.

Acquisition Strategic Rationale

The acquisition enhanced Shutterfly’s portfolio by incorporating Spoonflower’s print-on-demand capabilities and artist network. This allowed Shutterfly to enter new categories, including custom fabrics and wallpapers while leveraging Spoonflower’s eco-conscious practices. The transaction reinforced Shutterfly’s leadership in personalization by offering greater variety and depth in its product range, appealing to a growing market of customization-oriented consumers.

Case Study 02

TP APPAREL

TP Apparel LLC operates TeePublic, an e-commerce platform specializing in custom apparel and designs. The platform enables independent artists to upload and sell their creations on products such as t-shirts, hoodies, stickers, phone cases, and mugs. TeePublic serves as a marketplace where artists connect with consumers looking for unique and high-quality designs. Following its acquisition by Redbubble, TeePublic retained its brand identity, while TP Apparel LLC functions as its legal and operational entity under Redbubble’s ownership.

Transaction Structure

Redbubble acquired TeePublic for $41 million. The transaction included an initial cash payment of $35 million at closing, with a contingent payout of $6 million tied to the achievement of specific performance milestones.

Market and Customer Segments Combination

The merger brought together two major platforms for independent artists and consumers of personalized products. TeePublic’s focus on custom apparel and its strong foothold in the US market complemented Redbubble’s global presence and diverse product catalog. The integration enabled both platforms to scale their customer and artist networks while leveraging their combined expertise in design-oriented e-commerce.

Acquisition Strategic Rationale

The acquisition reinforced Redbubble’s position in the personalized product market. By incorporating TeePublic’s platform, Redbubble expanded its product offerings and improved operational efficiencies. This move also supported its strategy to strengthen its market share in key regions, particularly in the US, while fostering innovation and community engagement.

Case Study 03

COVEROO

Coveroo specialized in creating personalized covers and cases for mobile devices, including phones, tablets, and MP3 players. It developed a patented customization platform that allowed users to design one-of-a-kind products. These designs featured artwork from major brands such as Major League Baseball, the National Hockey League, and DC Comics, as well as independent artists.

Transaction Structure

Coveroo was acquired by Zazzle on November 24, 2015, for an undisclosed amount. The details of the transaction structure, including payment type and any performance-based terms, were not publicly disclosed.

Market and Customer Segments Combination

The acquisition brought together two prominent companies in the customizable product market. Coveroo’s focus on personalized tech accessories complemented Zazzle’s expansive catalog of customizable goods. This integration expanded Zazzle’s offerings to include high-quality mobile device cases while providing Coveroo access to Zazzle’s international customer base. Together they served a wide audience, including individual consumers, businesses, and fans of licensed brand artwork.

Acquisition Strategic Rationale

The acquisition enabled Zazzle to strengthen its customization capabilities by integrating Coveroo’s patented technology for mobile accessories. Coveroo’s expertise in licensed artwork and tech-focused products further diversified Zazzle’s portfolio. The deal also aligned with Zazzle’s strategy to deepen partnerships with major brands and broaden its market appeal.

The CPG customization technology sector has experienced significant growth from Q1 2020 to Q4 2024, driven by substantial M&A activity focused on scaling advanced personalization technologies, expanding market reach, and consolidating leadership in a dynamic market. Strategic acquisitions, such as Shutterfly’s purchase of Spoonflower, Redbubble’s acquisition of TeePublic, and Zazzle’s acquisition of Coveroo, highlight the sector’s emphasis on innovation, operational synergies, and market expansion. As the market continues to mature, strategic M&A remains crucial for addressing evolving consumer demands, fostering innovation, and driving long-term growth in this rapidly evolving industry.

Source: MarketScreener, Redbubble, Zazzle, Businesswire, Pitchbook Data.