Global Mobile Application Publishing M&A Transactions and Valuations

Global Mobile Application Publishing M&A Transactions and Valuations

The global mobile application publishing sector is expanding as AI-driven marketing, programmatic advertising, and user acquisition technologies improve efficiency. Advances in mobile ad monetization, predictive analytics, and customer data platforms (CDPs) enhance engagement, revenue growth, and application lifecycle optimization. M&A activity and investments in the sector focus on scalability, automation, and data-driven decision-making in mobile application publishing.

This report examines M&A transaction trends, valuation metrics, and investment patterns from Q1 2020 to Q4 2024, with a focus on industry consolidation, capital deployment, and strategic acquisitions. It analyzes major deals, including Blackstone and BoxGroup’s acquisition of Liftoff, Unity’s merger with ironSource, and Rokt’s acquisition of mParticle, assessing their strategic rationale, valuation multiples, and market impact.

Additionally, the report evaluates valuation trends, including EV/revenue and EV/EBITDA multiples, to determine pricing patterns and investment dynamics. It provides insights for investors, financial advisors, corporate executives, and industry leaders, offering a detailed perspective on the competitive landscape, emerging opportunities, and strategic direction of the mobile app publishing businesses.

- Valuation multiples are based on a sample set of M&A transactions in the global mobile application publishing and related sectors, using data collected on March 11, 2025.

- Mobile app publishers with EV/revenue ratios above 8x signal strong growth expectations, driven by high user acquisition, engagement, and monetization potential. In contrast, lower ratios indicate mature or slower-growing publishers with steady revenue streams.

- Some mobile app publishers trade at EV/EBITDA multiples exceeding 100x, reflecting either rapid expansion opportunities or investor speculation. These high valuations often stem from heavy reinvestment in user acquisition and platform development, delaying profitability.

- Most publishers in the dataset fall within an EV/revenue range of 2x to 8x and an EV/EBITDA range of 10x to 40x. This suggests a typical financial profile for companies balancing expansion with sustainable monetization.

Capital Markets Activities

The data highlights transaction trends, valuation metrics, and geographic investment patterns in the global mobile application publishing sector. Growing demand for mobile-first experiences, in-app monetization, and AI-driven personalization has fueled M&A activity and investment. Strategic acquisitions and private equity buyouts are scaling app distribution platforms, mobile ad networks, and AI-powered user engagement solutions. These trends are driving market consolidation, innovation, and the integration of machine learning, predictive analytics, and cloud-based app ecosystems.

- Investors injected $474 billion into 2,453 deals over 20 quarters, reflecting sustained confidence in the sector. The high deal volume underscores a competitive M&A landscape where companies actively pursue acquisitions to expand user bases, enhance monetization, and strengthen market positions.

- Investment peaked in Q4 2021 at $56 billion across 213 deals, marking a surge in investor activity. This spike likely resulted from strong mobile adoption, increased app spending, and aggressive expansion by major players. The record-breaking quarter suggests a race to acquire high-performing apps, optimize ad networks, and expand digital ecosystems.

- By Q4 2023, investment dropped to $5 billion across 90 deals, signaling cautious capital deployment. Economic uncertainty, regulatory shifts, and changes in mobile advertising likely contributed to the decline. However, the sector rebounded in 2024, with Q3 investment rising to $26 billion, reflecting renewed confidence in mobile engagement, subscription-based models, and AI-driven app experiences.

- Quarterly deal volume ranged from 80 to 213, showing that while investors adjusted capital flows, M&A remained a key growth strategy. Even in periods of lower investment, companies pursued acquisitions to diversify revenue, enhance app discovery, and capitalize on trends like gaming, fintech, and AI-driven personalization.

The graphs below present the geographic distribution of transactions, providing additional detail on regional trends and investment dynamics.

- The United States led mobile app investment, contributing 58% of total capital and 37% of deal activity. A strong venture capital ecosystem, tech-driven economy, and large consumer base fueled its dominance. The US remains a key hub for mobile publishing, driving innovation in AI-driven personalization, gaming, and subscription-based monetization. The disparity between capital share and deal volume suggests that high-value transactions were concentrated in the US, while smaller deals occurred elsewhere.

- Investors actively explored opportunities in emerging and international markets, which accounted for 48% of deals and 28% of total capital. This imbalance reflects a growing interest in mobile-first economies, digital payments, and untapped user bases. Rapid mobile adoption and high engagement in regions like Asia, Latin America, and Africa position these markets as prime targets for app publishers and ad-tech platforms.

- Canada and the Netherlands played smaller yet strategic roles in deal activity. Canada represented 5% of transactions, with potential for growth as its mobile startups expand globally. The country’s strength in gaming, fintech, and AI-driven applications enhances its presence in mobile publishing. Meanwhile, Dutch investors contributed 6% of total capital, demonstrating targeted interest in scaling European mobile publishers and ad-tech firms. With its innovation-driven economy and strong digital infrastructure, the Netherlands serves as a key base for mobile app expansion across Europe.

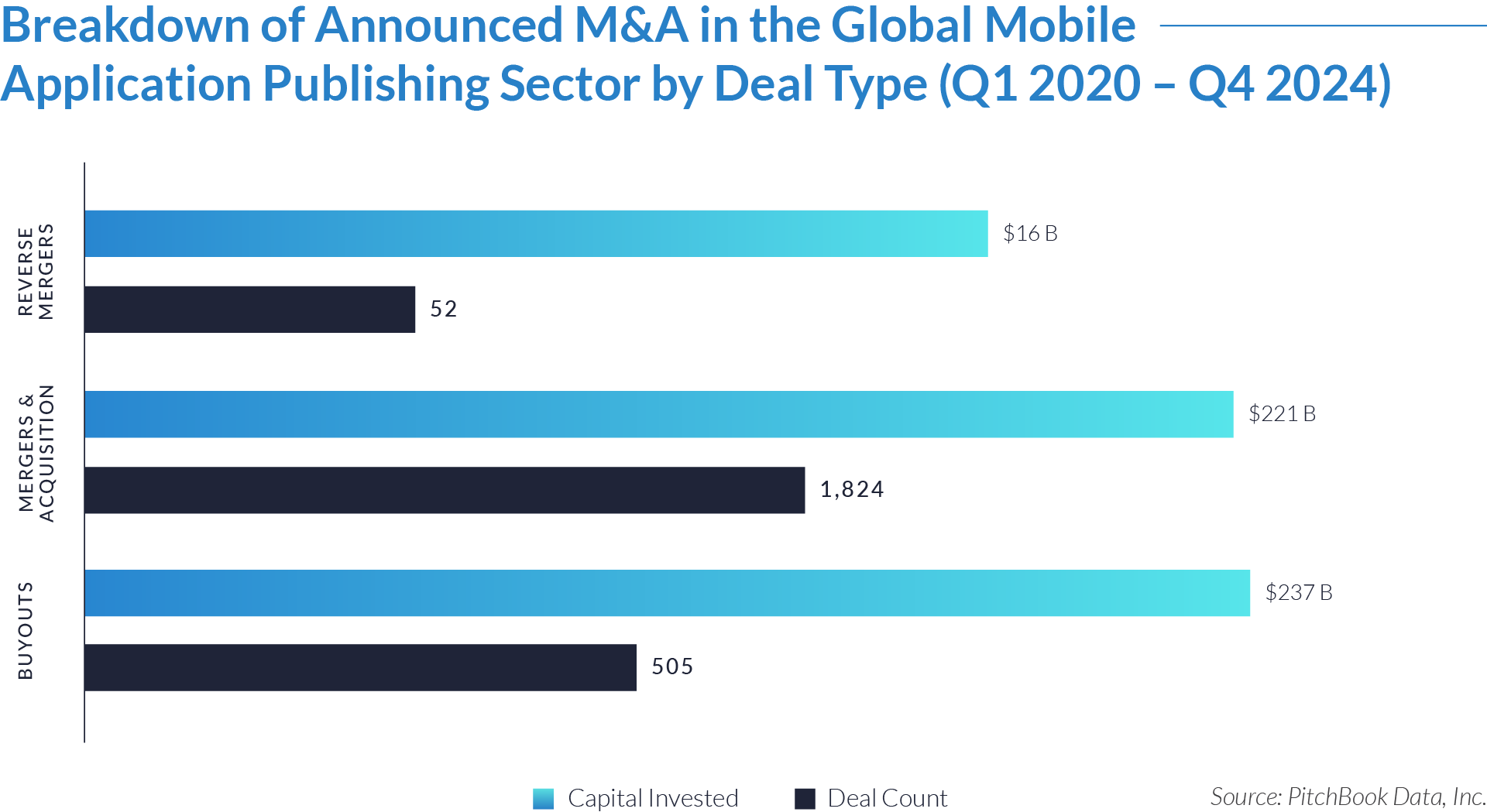

The deal-type dynamics below set the stage for understanding how capital flows and strategic priorities shape the global mobile application publishing sector’s growth and landscape.

- Investors committed $237 billion to 505 buyouts, aiming for full ownership and control in the mobile app publishing sector. Private equity firms and strategic buyers targeted high-growth app publishers, ad-tech platforms, and gaming studios to scale operations, enhance monetization, and maximize long-term value. The substantial capital investment underscores confidence in the sector’s growth potential.

- Companies executed 1,894 mergers and acquisitions worth $221 billion, making it the most prevalent deal type. Industry leaders aggressively expanded market share, integrated new technologies, and strengthened competitive positions through acquisitions. Many leveraged M&A to diversify revenue, boost user engagement, and optimize app distribution, accelerating market consolidation.

- Mobile app firms secured $16 billion through 52 reverse mergers, leveraging SPACs and backdoor listings for quicker public market entry than traditional IPOs. This method provided faster access to capital while preserving operational flexibility. The lower deal volume suggests that companies pursued reverse mergers selectively as a niche but strategic funding strategy.

M&A Transactions Case Studies

Three major acquisitions in the global mobile application publishing sector demonstrate a strategic shift toward AI-driven advertising, real-time data optimization, and automated user acquisition solutions. These deals expanded app monetization capabilities, enhanced predictive analytics, and strengthened cross-platform marketing strategies across various industries. Each acquisition highlights how investors prioritize scalable marketing technologies, machine learning–driven engagement tools, and integrated monetization platforms to maximize app growth and revenue potential.

Case Study 01

MPARTICLE

MParticle is a US-based customer data platform (CDP) that enables businesses to collect, unify, and activate customer data across mobile apps, websites, and third-party services. Its platform supports real-time customer profiles, audience segmentation, identity resolution, and data governance, enhancing personalization, marketing strategies, and regulatory compliance.

Transaction Structure

Rokt, an e-commerce technology company specializing in real-time relevance and optimization, acquired mParticle for $300 million. The payment structure has not been publicly disclosed.

Market and Customer Segments Combination

Rokt and mParticle serve enterprise-level clients, including leading retailers and brands. Both companies focus on large-scale enterprises seeking advanced data management and personalized customer engagement. By integrating mParticle’s real-time customer data platform with Rokt’s e-commerce marketing technologies, the combined entity enhances services for mutual clients, optimizing customer interactions and driving better business outcomes.

Acquisition Strategic Rationale

Rokt’s acquisition of mParticle enhanced its ability to deliver real-time relevance in e-commerce transactions. By leveraging mParticle’s expertise in customer data management, Rokt sought to provide businesses with more precise targeting and personalization, leading to stronger performance outcomes. This strategic move positioned Rokt to offer a more comprehensive solution, enabling brands to activate their data in real time while maintaining full control over customer data assets.

Case Study 02

IRONSOURCE

IronSource is a software company based in Israel that helps app developers monetize, distribute, and grow their applications through a suite of advanced tools. Its offerings include ad monetization solutions to generate revenue from in-app ads, user acquisition services to drive installs and engagement, and analytics tools for performance optimization. Additionally, ironSource provides app distribution platforms that help businesses scale their mobile applications efficiently and maximize profitability.

Transaction Structure

IronSource was acquired by Unity in an all-stock transaction valued at more than $4 billion. The deal provided a 74% premium over ironSource’s 30-day average exchange ratio.

Market and Customer Segments Combination

Unity’s acquisition of ironSource brought together two major players in the mobile gaming and app ecosystem. IronSource serves mobile app developers, publishers, and advertisers seeking monetization, user acquisition, and analytics solutions. Unity supports game developers, enterprises, and creators using its game engine and development tools. The merger integrated Unity’s development and gaming services with ironSource’s monetization and distribution capabilities, which created a seamless end-to-end solution for developers to build, grow, and monetize their applications.

Acquisition Strategic Rationale

The acquisition created a comprehensive platform that unified game development, monetization, and user acquisition. By combining Unity’s game engine and development tools with ironSource’s ad monetization, mediation, and distribution expertise, the merger enhanced developers’ ability to scale and monetize apps more effectively. This strengthened Unity’s competitive position against major players by offering a more integrated ecosystem for mobile game developers. Additionally, the acquisition unlocked new revenue opportunities by leveraging ironSource’s data-driven monetization expertise, improving operational efficiencies and long-term growth potential for both companies.

Case Study 03

LIFTOFF MOBILE

Liftoff is a mobile app marketing and monetization platform based in the US that helps businesses acquire, engage, and retain high-quality users at scale. Using machine learning, it provides solutions for user acquisition, re-engagement, creative optimization, and monetization, enabling app developers and marketers to boost performance and maximize revenue.

Transaction Structure

Blackstone and BoxGroup acquired Liftoff through a $400 million leveraged buyout on December 22, 2020.

Market and Customer Segments Combination

Liftoff serves mobile app developers, advertisers, and marketers seeking to acquire and engage high-value users. Its platform is widely used across industries such as gaming, e-commerce, finance, and entertainment. Blackstone, a global investment firm, provides extensive resources and strategic expertise, while BoxGroup specializes in supporting innovative technology companies. The acquisition enabled Liftoff to expand its reach, leveraging Blackstone’s capital and BoxGroup’s network to accelerate growth in the sector.

Acquisition Strategic Rationale

The acquisition of Liftoff aligned with Blackstone’s strategy to invest in high-growth, technology-driven businesses with strong market potential. By acquiring Liftoff, Blackstone and BoxGroup sought to capitalize on the rising demand for mobile app marketing solutions, fueled by increasing app usage and growing competition in the digital space. The investment enabled Liftoff to scale its machine-learning capabilities, expand global operations, and enhance product offerings, positioning the company for long-term growth and market leadership in mobile advertising.

The global mobile application publishing sector continues to evolve, driven by AI-driven growth strategies, programmatic advertising, and data-driven decision-making. M&A activity reflects increasing consolidation, investment in monetization technologies, and expansion into high-growth markets. As valuation trends shift, businesses must adapt to scalability demands and competitive pressures. Investors and industry leaders should leverage emerging opportunities to optimize growth, enhance profitability, and strengthen market positioning.

Source: mParticle, PR Newswire, TechCrunch, Unity, Yahoo Finance, Pitchbook Data.