B2B Sales Solutions Transactions and Valuations

B2B Sales Solutions Transactions and Valuations

Between Q1 2020 and Q2 2024, over $40 billion was deployed across 872 M&A transactions in the B2B sales solutions sector, with an average deal size of $50 million.

B2B sales solutions are strategic tools and methodologies aimed at optimizing the business-to-business sales process. These solutions typically involve software platforms that help sales teams create compelling business cases, quantify the financial impact of their offerings, and effectively communicate value propositions to potential clients. By leveraging data-driven insights, these solutions enable businesses to improve customer engagement, streamline decision-making, and close deals more efficiently, ultimately driving better sales outcomes.

The B2B sales solutions industry has experienced substantial growth, fueled by advancements in AI and machine learning that enhance sales processes through predictive analytics and automation. The shift towards hybrid and remote selling has further improved efficiency, enabling companies to utilize diverse talent and adaptable strategies. From Q1 2020 to Q2 2024 the sector maintained strong investment activity, particularly in the US and Europe, which dominated transactions and capital allocation. Consistent deal activity, despite market fluctuations, highlights the sector’s resilience and strategic importance. The industry is set to continue evolving, driven by ongoing technological innovation and strategic mergers and acquisitions.

- The valuation multiples are based on a sample set of private M&A transactions and publicly listed healthcare therapy companies in the sector. The data was collected on September 4, 2024.

- The sample set typically trades at an enterprise value to revenue multiple range between 2x and 5x, increasing as the enterprise value of the business increases.

- Enterprise value to EBITDA multiples varied significantly, typically ranging between 6x and 11x. This valuation stays consistent as the enterprise value of the business increases.

- Between Q1 2020 and Q2 2024, over $40 billion was deployed across 872 M&A transactions in the B2B sales solutions sector by global firms, with an average deal size of $50 million.

- Q3 2021 reflects the period with the most significant capital deployment ($19.6 billion) and the highest deal count (68 deals).

- The capital invested fluctuates significantly throughout the period while the deal count remains stable around the mean of 48 deals per quarter. This indicates a consistent demand for M&A transactions in B2B sales solutions even through market conditions, which may suppress valuations.

- The largest completed transaction was the full acquisition of Personify Health through a leveraged buyout by HealthComp, via its financial sponsors Blackstone, Eir Partners, and New Mountain Capital. Personify Health was acquired for $3 billion in November 2023.

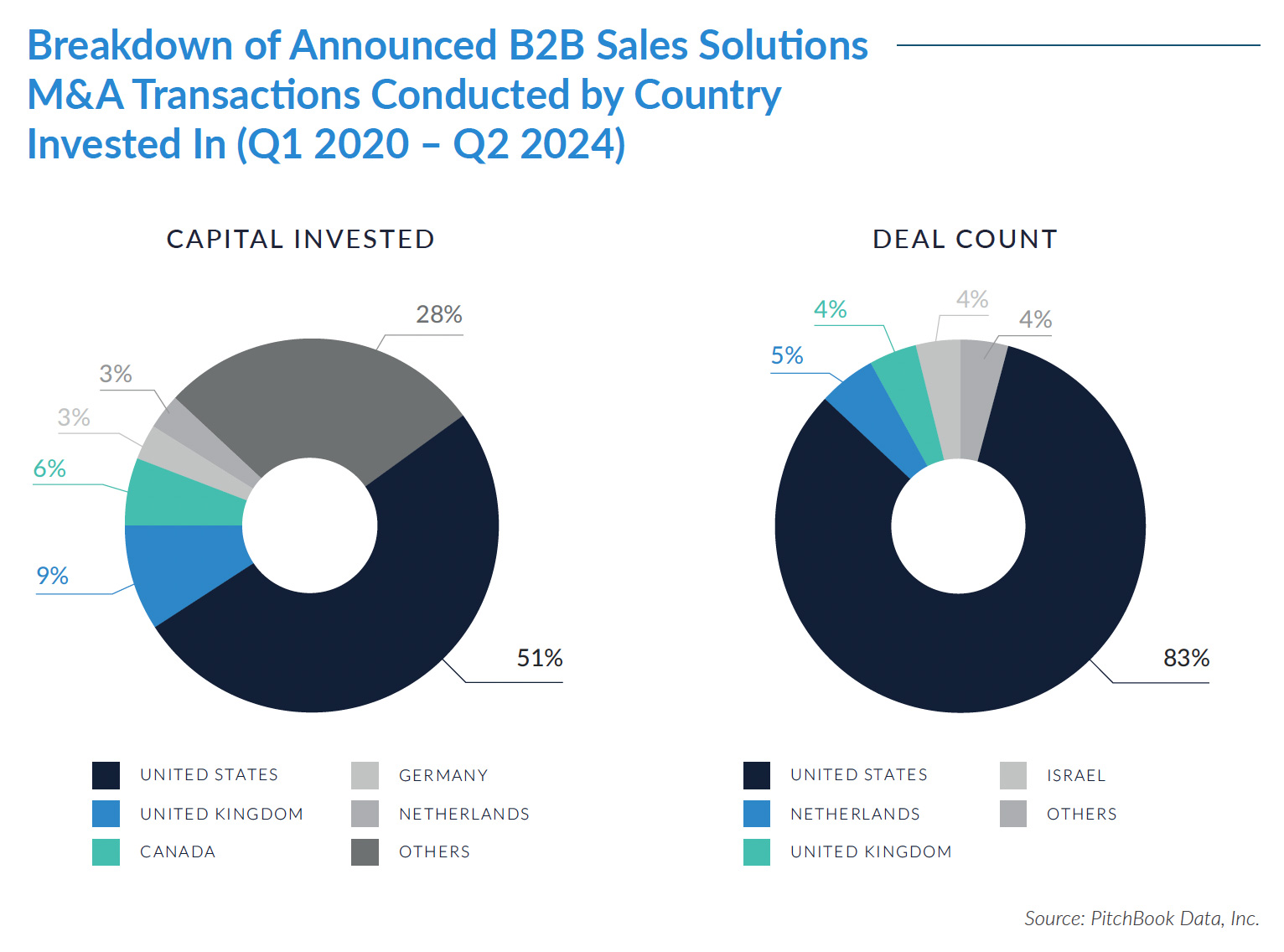

- The United States accounts for the majority of the deal count and the capital invested, with 450 transactions representing 51% of the total deal count and $37 billion capital invested representing 83% of the total. This indicates a significant focus on the US market in B2B sales solutions M&A activity during this period.

- The United Kingdom is the second-largest region by deal count, with 80 transactions, accounting for 9% of the total. This suggests a strong presence in the B2B sales solutions market.

- The capital invested is highly concentrated in a few countries, with the US (83%), the Netherlands (5%), the UK (4%), and Israel (4%) together representing the majority of the capital invested. These countries collectively account for significant global investments in the B2B sales solutions sector.

- Mergers and acquisitions (M&A) were the most prevalent deal type, with 573 deals and a significant $35 million in capital invested. This highlights the strong preference for M&A as a strategy in the B2B sales solutions sector, accounting for the largest deal count and capital share.

- Corporate divestitures, accounting for only 73 deals, have the second-highest capital investment of $13 million. This suggests that these deals, although fewer, involve substantial asset transfers or corporate restructuring, resulting in high capital requirements.

- Buyouts/leveraged buyouts (LBOs) were also a significant deal type, with 296 deals totaling $8 million in capital invested. This indicates that private equity and other investors actively pursue LBOs in this sector, often restructuring or refinancing businesses.

Deal Spotlight:

ANALYTIC EDGE

The Company

Singapore-based Analytic Edge offers a sales and marketing analytics platform that enhances budget optimization and measures the effectiveness of digital sales and marketing efforts. The platform captures both direct and indirect contributions, provides insights into pricing strategy, sales forecasting, determining ROI on marketing strategies, and assortment optimization, while identifying key customer segments. It helps businesses streamline their sales process, drive consumer demand, acquire new customers, and protect revenues while improving workforce management and overall operational efficiency.

Course5 Intelligence acquired 100% of Analytic Edge for $35 million to enhance its AI-powered sales and marketing analytics solutions. This strategic integration strengthens Course5’s value proposition.

The acquisition was made at an enterprise value of $35 million, reflecting a 3.5x enterprise value to revenue multiple, based on Analytic Edge’s $10 million in revenue.

The B2B sales solutions sector has experienced substantial growth from Q1 2020 to Q2 2024, with over $40 billion deployed across 872 transactions, resulting in an average deal size of $50 million. Valuation multiples remained competitive, with enterprise value to revenue multiples ranging from 2x to 5x, and enterprise value to EBITDA multiples ranging from 6x to 11x. The US dominated the market, accounting for 51% of the deals and 83% of total capital invested. The sector’s resilience is highlighted by the consistency in deal count, even amid fluctuating capital investments.

The industry’s growth is propelled by technological advancements, such as AI and machine learning, which enhance sales processes and drive efficiency. The focus on M&A as the dominant strategy underscores the sector’s dynamic nature, with significant activity concentrated in the US and supported by strategic divestitures and buyouts.

Sources: Uplead, Draup, Mc Kinsey & Company (1), (2), Simon-Kucher, Vainu, The Future of Commerce, Pitchbook M&A Research.