Logistics and Transportation Technology M&A Transactions and Valuations

Between Q1 2020 and Q3 2024, the logistics and transportation technology sector experienced substantial growth, driven by the widespread adoption of digital transformation efforts throughout the industry. Companies increasingly automated their processes and used advanced analytics to enhance scalability and operational efficiencies, which led to increased demand for innovative logistics solutions. The need for robust, scalable logistics infrastructure prompted more investments in transportation technologies, making modernization a crucial component of business strategies.

This report examines transaction trends, valuation metrics, and regional dynamics, providing a detailed analysis of the strategic factors that drive M&A activities within the logistics and transportation technology sector. Valuation indicators such as EV/revenue and EV/EBITDA reveal investor priorities and the market conditions that shape valuations. Significant transactions, such as Uber Freight’s acquisition of Transplace, The Jordan Company’s buyout of Echo Global Logistics, and e2open’s acquisition of BluJay Solutions, demonstrate the industry’s focus on technological progress, scaling operations, and consolidating market leadership. These examples show how strategic mergers and acquisitions influence the competitive landscape and offer insights for investors, advisors, and stakeholders in this evolving market.

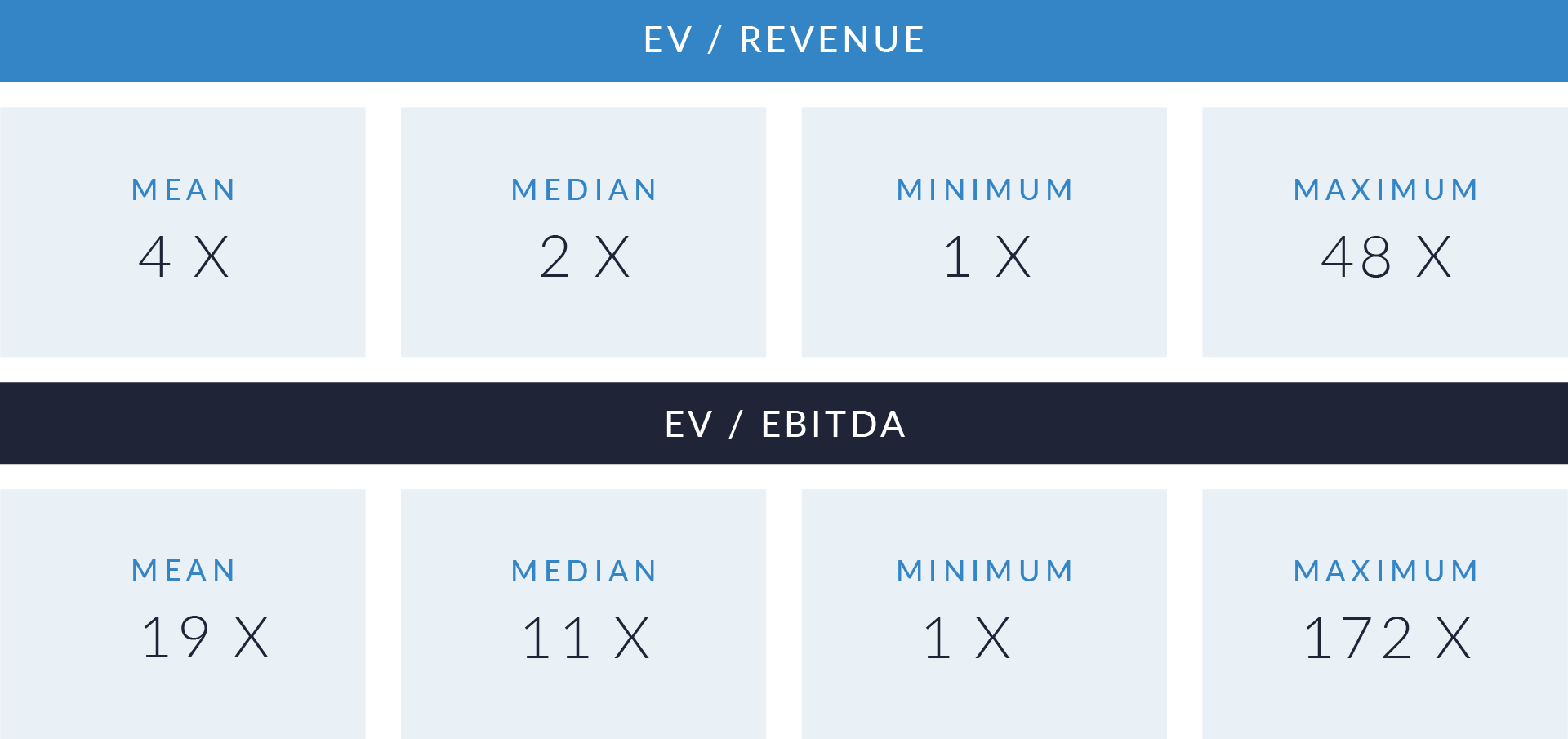

- Valuation multiples are based on a sample set of private and public M&A transactions in the logistics and transportation technology sector, using data collected on December 12, 2024.

- Larger companies typically achieve lower valuation multiples as their enterprise value increases, with EV/revenue and EV/EBITDA multiples clustering in the lower range 1x to 42x. This reflects their stable performance, predictable cash flows, and established market positions, which reduce investor risk and limit the premium paid for growth potential.

- Smaller companies exhibit greater variability in valuation, particularly in the lower EV range below $100 million, where multiples often disperse widely and extend upward of 10x to 172x. This reflects investor willingness to pay premiums for the higher growth potential and increased uncertainty associated with smaller, high-growth companies.

- Profitability plays a key role in driving valuation differences, as EV/EBITDA multiples consistently exceed EV/revenue multiples. This underscores the significance of profitability in valuation assessments, with EBITDA-based metrics providing a clearer measure of operational efficiency and cash flow, especially for companies with higher enterprise values.

Capital Markets Activities

The data highlights transaction trends, valuation metrics, and regional dynamics in the logistics and transportation technology sector. The adoption of digital freight platforms, cloud-based supply chain solutions, and real-time analytics has fueled M&A activity and shaped valuations. Investors are leveraging diverse deal structures and geographic strategies to meet the growing demand for scalable, efficient logistics technologies, reshaping M&A dynamics, fostering innovation, and redefining the competitive landscape.

- Investors committed $718 billion to the logistics and transportation technology sector between Q1 2020 and Q3 2024, completing 1,951 deals with an average deal size of $368 million.

- Capital investment peaked at $87 billion in Q4 2021, with 161 deals, the highest on record, reflecting strong investor confidence and strategic interest in the sector. During this period, companies capitalized on growth opportunities, scaling and innovating rapidly.

- After this peak, both capital investment and deal count moderated, with deal activity declining to 56 deals by Q3 2024. This shift signals a maturing market as investors focus on fewer, higher-quality transactions that prioritize efficiency, innovation, and long-term value creation.

- Although capital investment dipped to $15 billion in Q3 2024, recent trends demonstrate a steady adjustment to evolving economic and market conditions. This stabilization underscores a commitment to sustainable growth and strategic consolidation, directing resources toward impactful technologies and transformative companies.

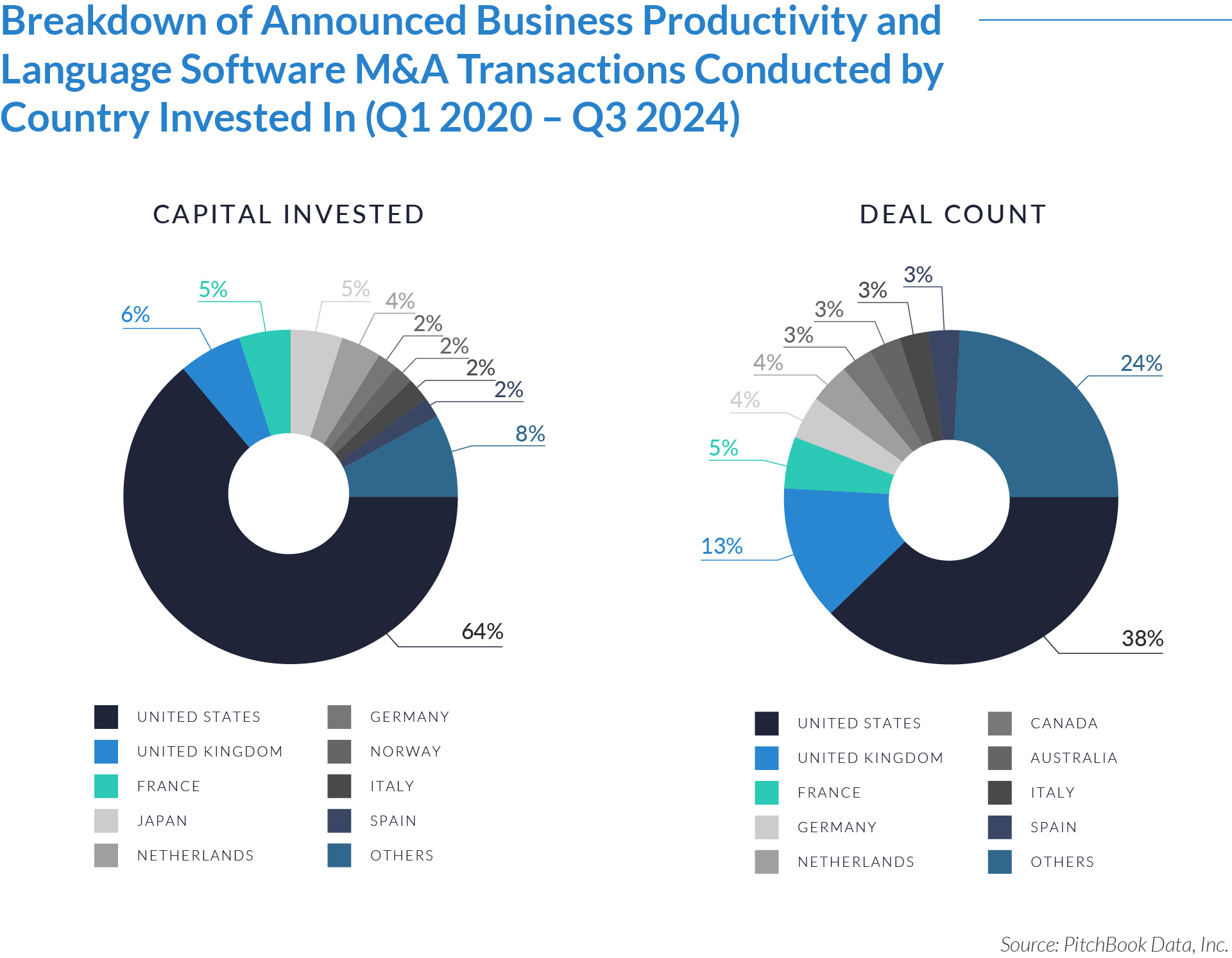

The graphs below present the geographic distribution of transactions, providing additional detail on regional trends and investment dynamics.

- The United States leads the market, capturing 30% of the total deal count and 50% of capital invested. This dominance underscores the region’s strong focus on large-scale, high-value transactions and its position as a global hub for logistics and transportation technology investments.

- Germany (6% deal count, 5% capital) and the United Kingdom (8% deal count, 4% capital) exhibit moderate deal activity with smaller transaction sizes, reflecting limited capital flows in these regions. This highlights their focus on mid-market opportunities and regional investments, contributing to the sector’s overall diversity in transaction dynamics. Despite their smaller scale, these markets remain essential contributors to innovation and localized growth in the logistics and transportation technology sector.

- Regional markets outside the US accounted for 49% of the deal count and 34% of capital invested, highlighting extensive activity across smaller markets with lower transaction values. This reveals emerging opportunities in diverse regions, even as major markets like the US maintain their dominance in attracting most capital flows.

The deal-type dynamics below set the stage for understanding how capital flows and strategic priorities shape the logistics and transportation technology sector’s growth and landscape.

- Mergers and acquisitions lead the market, accounting for $460 billion in capital across 1,432 deals. This dominance shows that M&A activity drives most capital flows and deal volume, reflecting ongoing consolidation trends and strategic acquisitions across industries. Businesses use these large, transformative deals to fuel growth, expand markets, and achieve operational synergies.

- Buyouts contribute $228 billion in capital across 436 deals, demonstrating that private equity and institutional investors prioritize acquiring control stakes in companies. The higher capital per deal reflects a preference for larger transactions that maximize long-term returns. Investors confidently leverage buyouts to improve operations and unlock significant value in target companies.

- Public-to-private deals represent the smallest share, with $30 billion in capital and 83 deals. While less frequent, these transactions highlight investor interest in taking undervalued public companies private. Factors such as valuation challenges, financing costs, and market conditions likely limit their volume, but they remain a strategic option for acquiring valuable assets with the potential for private transformation.

M&A Transactions Case Studies

Three notable M&A transactions in the logistics and transportation technology sector highlight strategic growth through enhanced market leadership, advanced technological integration, and expanded operational capabilities. These deals emphasized global expansion, operational synergies, and technological innovation, redefining the competitive landscape. Investors leveraged targeted strategies to drive scalability, foster sustainable growth, and create long-term value in this rapidly evolving industry.

Case Study 01

BLUJAY SOLUTIONS

BluJay Solutions, based in the United Kingdom, is a global leader in cloud-based supply chain and logistics management software. The company offers comprehensive solutions, including freight forwarding, transportation management, and global trade compliance, enabling businesses to optimize their logistics operations and enhance supply chain efficiency.

Transaction Structure

E2open acquired BluJay Solutions in a $2 billion transaction that included 72 million shares of e2open’s Class A common stock and $760 million in cash. The cash component covered debt repayment and adjustments under the purchase agreement, with financing provided by Credit Suisse and Goldman Sachs.

Market and Customer Segments Combination

The acquisition combined BluJay’s expertise in global trade and transportation management with e2open’s end-to-end SaaS supply chain platform, creating a comprehensive solution that catered to a wide range of industries including retail, manufacturing, and logistics service providers. This integration strengthened their ability to address complex supply chain needs for global customers and enhanced cross-industry collaboration by offering a unified platform for managing supply chain, logistics, and compliance workflows.

Acquisition Strategic Rationale

The deal accelerated e2open’s growth by expanding its SaaS platform capabilities, enhancing global trade and logistics offerings, and positioning the company as a leader in supply chain management. Additionally, the acquisition drove operational synergies, increased market share, and gave BluJay’s customers access to e2open’s broader portfolio of supply chain solutions. This combination enabled the company to scale its operations globally and deliver greater value through a more comprehensive suite of services.

Case Study 02

TRANSPLACE

Transplace, a US-based logistics technology and transportation management company, delivers comprehensive supply chain solutions. Its offerings include managed transportation, freight brokerage, and advanced logistics technology, all designed to optimize freight operations and enhance efficiency for shippers.

Transaction Structure

Uber Freight acquired Transplace for more than $2 billion, with $750 million paid in Uber stock and more than $1 billion in cash, financed through a combination of internal resources and external funding.

Market and Customer Segments Combination

The acquisition combined Uber Freight’s extensive network of digitally enabled carriers with Transplace’s shipper-focused technology and operational solutions, creating a comprehensive platform to serve both small businesses and large enterprises. By uniting these complementary networks, the deal bridged the gap between supply and demand in the logistics market, ensuring better service coverage and efficiency.

Acquisition Strategic Rationale

The deal enhanced Uber Freight’s ability to provide integrated logistics solutions, optimized its supply chain efficiencies, and strengthened its position as a leader in the freight technology market. Additionally, it accelerated Uber Freight’s growth strategy by expanding its footprint in managed transportation and enhancing its value proposition for enterprise shippers.

Case Study 03

ECHO GLOBAL LOGISTICS

Echo, a technology-driven transportation and logistics company based in the US, specializes in freight management and brokerage services. The company connects shippers with carriers, delivering optimized shipping solutions that enhance efficiency and streamline supply chain operations.

Transaction Structure

Echo Global Logistics was acquired for more than $1 billion in a public-to-private leveraged buyout led by The Jordan Company, with participation from Finback Investment Partners, Barings BDC, and Barings. Valued at more than $48 per share in cash, the transaction was supported by $810 million in debt financing, ensuring the necessary capital to complete the acquisition.

Market and Customer Segments Combination

The acquisition enhanced Echo’s ability to serve diverse customer segments, from small-to-medium-sized businesses to enterprise-level shippers, by providing tailored freight and logistics solutions. This alignment broadened market access and strengthened its position in the competitive logistics sector. Additionally, it created opportunities for deeper integration of Echo’s technology platform, delivering greater efficiency and cost savings for customers.

Acquisition Strategic Rationale

The transaction provided Echo with resources and operational flexibility to accelerate growth, invest in technology innovation, and expand its service offerings under private ownership. This approach drove long-term value creation and competitive differentiation, while private ownership enabled Echo to pursue strategic initiatives without the short-term pressures of public markets.

The logistics and transportation technology sector is undergoing rapid transformation, with M&A activity fueled by the drive to scale advanced digital solutions, enhance operational capabilities, and consolidate market leadership in an increasingly dynamic environment. Transactions have focused on technologies that boost supply chain efficiency, optimize freight management, and meet the growing need for resilient and agile logistics systems. As companies adapt to economic and technological changes, M&A remains a pivotal strategy for unlocking synergies, fostering innovation, and seizing emerging opportunities in global markets. The sector’s sustained investment in transformative technologies reinforces its critical role as the backbone of modern supply chains, presenting significant opportunities for long-term growth and value creation. Looking ahead, investors and stakeholders are well-positioned to harness strategic M&A to address shifting industry demands and secure competitive advantages in both mature and developing markets.

Source: Uber Investor, TechCrunch, PR Newswire, E2open, Pitchbook Data.